Table of Contents >> Show >> Hide

- Why 300,000 Valuations in 30 Days Is a Big Deal

- The Venture Market Is Strong, Selective, and Weird All at Once

- What Makes SaaStr’s Calculator Useful

- Why the AI Premium Changes Everything

- What the Milestone Says About SaaStr

- What Founders Should Do With a Valuation Estimate

- The Bigger Lesson: Transparency Wins

- Founder Experiences: What This Kind of Tool Feels Like in the Real World

- Conclusion

- SEO Tags

Some startup products solve a problem. Others expose one that was already sitting in the room, wearing a blazer, pretending to be fine. SaaStr’s new AI-powered startup valuation calculator appears to be the second kind. Crossing 300,000 valuations in just 30 days is not merely a nice growth chart for a product dashboard. It is a flare shot into the sky over the venture market, signaling that founders are still wildly unsure what their companies are actually worth.

And honestly, who can blame them? The old valuation playbook has become about as reliable as weather predictions made by a raccoon. Traditional SaaS is still judged heavily on recurring revenue, growth rate, retention, and capital efficiency. But AI has scrambled the neat little boxes. Some companies with modest revenue are commanding premium valuations because investors believe they have unusual speed, defensibility, or category-creating upside. Others with solid but unglamorous metrics are discovering that the market is selective, slower, and harder to impress than it looked during the boom years.

That is what makes this SaaStr milestone so interesting. The calculator is not just a useful founder toy. It is a response to a market that has become more data-rich, more AI-obsessed, more stage-sensitive, and a whole lot more emotionally exhausting. If you are a founder trying to walk into a funding conversation armed with something better than vibes and caffeine, a tool like this suddenly feels less like a gimmick and more like survival gear.

Why 300,000 Valuations in 30 Days Is a Big Deal

The raw number is flashy, sure, but the real story is what it implies. When a valuation tool racks up this kind of usage so quickly, it tells us there is pent-up demand for pricing transparency in private markets. Founders do not want to hear “it depends” for the hundredth time. They want a starting point. They want a range. They want to know whether the number in their head is reasonable, ambitious, or “please do not say that out loud in front of investors.”

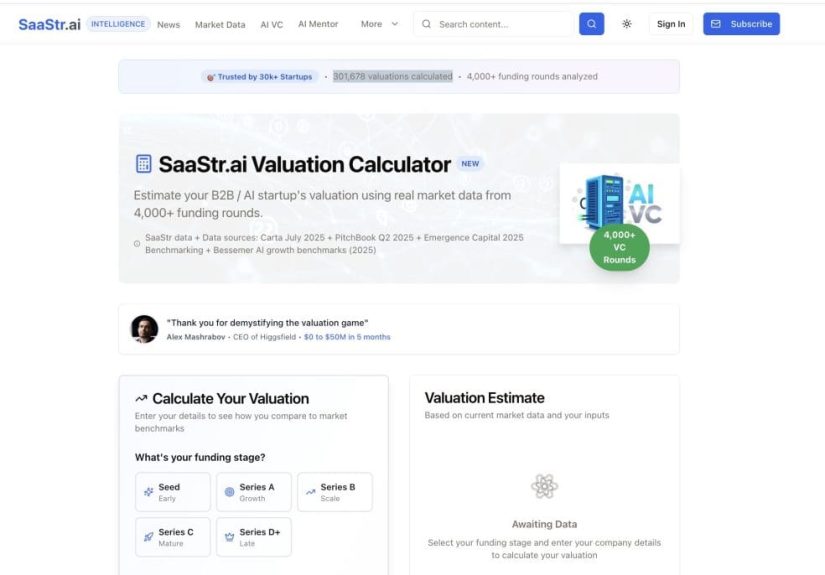

SaaStr has positioned the tool as a practical valuation assistant for B2B and AI founders. The idea is simple: pull together recent private market data, stage context, AI-versus-traditional SaaS comparisons, and current revenue multiple thinking, then turn all of that into a faster estimate of what a startup might command in the current environment. That is not the same as magically predicting a term sheet, of course. But it is a lot better than relying on a friend-of-a-friend’s stale 2021 fundraising story.

What makes the milestone even more notable is that SaaStr did not stop there. Early follow-up posts around the launch showed the calculator passing 200,000 valuations in roughly two weeks, then moving beyond 300,000 in 30 days, then later continuing upward. That kind of repeated traction suggests the product was not just curiosity-click bait. Founders kept showing up because the question stayed urgent: What is my company actually worth right now?

The Venture Market Is Strong, Selective, and Weird All at Once

To understand why the calculator hit a nerve, you have to understand the backdrop. Private startup markets are not dead. They are just choosier, sharper-edged, and heavily tilted toward the winners. In other words, the party is still happening, but the bouncer now has a spreadsheet.

On one side, valuations have held up surprisingly well in several parts of the market. Carta’s 2025 data showed median seed and Series A valuations rising even as deal volume cooled. That means strong startups can still command attractive prices. At the same time, the number of rounds has fallen, the time between rounds has lengthened, and investors are acting more selective. Translation: there is money, but not for everyone, and certainly not for every deck with the word “agentic” sprinkled across it like parmesan.

Then there is the AI factor. AI is not just another product feature anymore; in many cases, it is a valuation modifier. Bessemer’s 2025 benchmark work showed AI companies earning stronger revenue multiples than non-AI peers, while Carta’s 2025 market review showed a clear AI valuation premium across later stages. Reuters and Crunchbase both highlighted how heavily AI dominated venture dollars in 2025. That concentration matters because it changes founder expectations. If you are building an AI-native or AI-enhanced company, you are probably hearing about premium multiples everywhere. If you are building traditional SaaS, you are probably wondering whether investors still love you or just tolerate you politely.

This tension is exactly why a valuation calculator becomes appealing. It gives founders a way to benchmark themselves against the new reality instead of the mythology of the old one.

What Makes SaaStr’s Calculator Useful

At its best, a startup valuation tool should not act like a slot machine that spits out one shiny number. It should act more like a structured conversation starter. SaaStr’s version gained attention because it framed valuation through several lenses that actually matter in venture-backed software:

- Stage: A seed company and a Series C company with the same revenue are not valued the same way, and pretending otherwise is how founders accidentally embarrass themselves on Zoom.

- Company type: Traditional SaaS, AI-enhanced SaaS, and AI-native businesses are increasingly judged through different market expectations.

- Growth: Growth still does the heavy lifting. A fast-growing “boring” software company can absolutely outrun a slower AI company in valuation logic.

- Market comps: Recent funding rounds, private market benchmarks, and public-market thinking all influence the valuation envelope.

That last point matters a lot. Founders often hear “you’re worth X times ARR” as if ARR multiples are engraved on stone tablets somewhere in Silicon Valley. They are not. Multiples are shorthand, not truth. Brex, Carta, and a16z all make some version of the same point: recurring revenue is central to how many software companies are priced, but valuation is still deeply tied to growth quality, market position, capital efficiency, and long-term outcome potential.

That is why a data-driven calculator is useful even if it is imperfect. It forces the conversation away from fantasy math and toward defensible ranges.

Why the AI Premium Changes Everything

One of the most important reasons this tool took off is that founders know the market is rewarding AI exposure, but most do not know how much, when, or why. And that gap between “I think there’s an AI premium” and “I can defend this premium in a real fundraising conversation” is where confusion breeds.

The AI premium is real, but it is not automatic. Investors are not simply slapping a giant valuation sticker on every startup that can spell “LLM.” They are looking for signs that AI is truly embedded in the product, improves the economics, accelerates adoption, or changes the market ceiling. Bessemer’s research on AI leaders showed stronger multiples and much faster scaling among standout companies, but it also made clear that the best businesses are pairing speed with meaningful operational efficiency. Carta’s more recent data likewise points to AI companies winning larger rounds and higher valuations, especially once they prove they are more than a wrapper with a press release.

That nuance is important. A founder might plug numbers into a calculator and love the result, but the number only becomes believable if the story behind it holds up. Is the AI actually driving revenue expansion? Is customer demand durable? Are margins likely to improve? Is usage growth translating into contracted revenue? If the answer is no, then the tool is not lying to you so much as reminding you that markets pay for potential differently when the evidence is thin.

In other words, the calculator is useful not because it makes everyone look richer, but because it helps clarify why some companies deserve a premium and others do not.

What the Milestone Says About SaaStr

SaaStr has always done well when it turns founder anxiety into something concrete. Advice is helpful. Events are helpful. Podcasts are helpful. But tools are different. Tools take an abstract question and turn it into an action. That is probably why this product spread so quickly.

There is also a brand advantage here. SaaStr sits at the intersection of SaaS operators, AI builders, investors, and go-to-market leaders. When it ships a valuation tool, it is not entering the conversation as a random calculator website in a dark corner of the internet. It is leveraging years of audience trust, operator credibility, and distribution. In startup terms, that is a pretty unfair advantage.

The success of the calculator also hints at something larger: founder software is becoming its own category. SaaStr’s valuation calculator, pitch analysis tooling, and broader AI founder utilities point to a market where entrepreneurs increasingly want software that helps them prepare for fundraising, sharpen positioning, and sanity-check their assumptions. Not just content. Not just community. Actual working software.

That is a meaningful shift. It suggests founders no longer want to passively consume advice about fundraising. They want systems that help them act on it.

What Founders Should Do With a Valuation Estimate

Here is the part where we resist the urge to tattoo a calculator output on our forearm.

A valuation estimate is a tool, not a verdict. Smart founders use it in at least four practical ways:

1. Build a Range, Not a Fantasy Number

If the calculator suggests your company might fall between two valuation bands, work with the range. Do not cling to the highest number like it is your destiny. Founders who negotiate best usually know their floor, their stretch case, and the evidence required to justify either one.

2. Pressure-Test Your Story

If your implied valuation depends on a premium multiple, ask what exactly earns that premium. Faster growth? Better retention? AI leverage? Capital efficiency? A bigger market? If you cannot explain it clearly, investors will explain it for you, and you probably will not like their version.

3. Separate Fundraising Value From 409A Reality

This is crucial. A fundraising valuation estimate is not the same thing as a 409A valuation for employee stock option pricing. Carta, Kruze, and Y Combinator’s documentation all underscore how different these frameworks can be. One helps you think about what investors may pay in a financing context. The other helps establish fair market value for common stock and compliance purposes. Mixing them up is a terrific way to confuse your team and your finance lead at the same time.

4. Use It Before the Meeting, Not During the Meltdown

The best time to benchmark valuation is before you are emotionally attached to a term sheet. Once numbers are on the table, objectivity starts packing its bags. Founders who run scenarios early can walk into conversations more prepared, more grounded, and less likely to negotiate against themselves.

The Bigger Lesson: Transparency Wins

The real takeaway from 300,000 valuations in 30 days is not that one calculator had a good month. It is that founders are tired of opacity. They want better tools, faster benchmarks, and clearer frameworks for understanding how venture markets actually work now.

That is a healthy development. Startup valuation will never become perfectly objective. There will always be judgment, narrative, market timing, and a dash of venture capitalist mysticism. But the more founders can benchmark themselves against real data, the less likely they are to walk into fundraising conversations blind.

And that may be the most valuable part of this entire story. Not the number on the dashboard. Not the milestone headline. Not even the AI branding. The most valuable part is the behavioral change: more founders are trying to understand the rules before they step onto the field.

Frankly, that is overdue.

Founder Experiences: What This Kind of Tool Feels Like in the Real World

For many founders, using a valuation calculator like SaaStr’s is not a dramatic “Eureka!” moment. It is more like finally turning on the lights in a room where you have been tripping over furniture for six months. The first reaction is usually relief. The second is often panic. The third is a flurry of spreadsheet edits.

Imagine the typical early-stage founder in 2025 or 2026. Revenue is growing, but not evenly. Customers love the product, but churn still needs work. The company has some AI functionality, though the founder is not entirely sure whether investors will view it as “AI-enhanced,” “AI-native,” or “please stop saying agentic in every sentence.” That founder has heard stories from other teams: one company raised at a lofty multiple, another got pushed down hard, and a third spent months fundraising only to accept a round far below what everyone expected.

That is the emotional environment in which a valuation tool lands. It offers structure in the middle of noise. It gives a founder a way to ask practical questions: What happens if we grow faster for two more quarters? How much does our category positioning matter? Does a stronger gross margin profile move the range? Are we pricing ourselves like a durable software company or like a short-term AI experiment?

Even when the result is not flattering, there is value in that. In fact, some of the best founder experiences with valuation tools probably come from disappointment. A number that lands below expectation can force sharper thinking. Maybe the business is solid, but the growth story is not elite enough for a premium round. Maybe the team has a strong product but weak packaging. Maybe the AI narrative is exciting, but the economics are not yet convincing. A useful tool does not just flatter the founder; it helps expose the gap between internal optimism and external pricing logic.

There is also a negotiation benefit. Founders often walk into investor conversations either too timid or too aggressive. The timid ones under-ask because they do not want to look foolish. The aggressive ones anchor to a heroic valuation pulled from one hot company on social media. Neither approach is great. A calculator grounded in current market inputs can help founders land in the more productive middle: informed, flexible, and ready to explain the logic behind their ask.

Perhaps the biggest experiential benefit, though, is psychological. Fundraising is exhausting partly because it feels opaque. Every meeting can seem like a test where the grading rubric is hidden. Tools like this do not eliminate uncertainty, but they reduce the number of mysteries. And for founders, reducing mystery is not a small thing. It lowers stress, sharpens planning, and makes the next conversation a little less improvisational.

So yes, the headline is about 300,000 valuations in 30 days. But the human story underneath it is simpler: founders are desperate for clearer signals, and when someone offers a better map, they click.

Conclusion

SaaStr’s AI-powered startup valuation calculator crossing 300,000 valuations in 30 days is not just a fun milestone for a fast-growing tool. It is a snapshot of what modern founders need most: speed, context, and sanity in a market that rewards precision. The timing makes sense. Startup funding is still active, but selective. AI premiums are real, but uneven. Growth matters more than ever, yet it is no longer enough to quote a generic revenue multiple and call it strategy.

That is why this launch resonated. It gave founders a way to benchmark themselves against the market they are actually in, not the one they remember from screenshots in a Slack channel. Used correctly, a valuation calculator will not replace investor judgment, board input, or proper finance work. But it can give founders something much more useful than blind confidence: informed confidence.

And in venture, that is worth a lot.