Table of Contents >> Show >> Hide

- Why This Question Is Bigger Than It Sounds

- Where U.S. Households Stand Right Now

- Stocks: Your Growth Engine (But Only If You Respect Volatility)

- Housing: Stability, Leverage, and Lifestyle in One Asset

- Social Security: The Most Underestimated Retirement Asset

- So… What Matters Most?

- A Practical Framework by Life Stage

- Three Mini Case Studies

- Common Mistakes That Quietly Cost a Fortune

- The Bottom Line

- Experience Notes (Extended 500+ Words): Real-World Patterns Behind Stocks, Housing & Social Security

- Conclusion

Ask ten people what matters most for long-term financial security and you’ll get eleven answers.

One friend will say, “The stock market, obviously.” Another says, “Buy a house and chill.” A third

says, “Social Security is the real safety net.” The truth is less dramatic and much more useful:

all three matter, but they matter differently depending on your age, income, debt, health,

location, and risk tolerance.

Think of your financial life as a three-engine system:

stocks drive long-term growth,

housing provides stability plus forced equity building,

and Social Security anchors lifetime income in retirement.

If one engine sputters, the other two can keep you moving. If all three are tuned well, you get what most people

actually want: flexibility, options, and fewer 3 a.m. money panic sessions.

This article synthesizes data and guidance from major U.S. sources across household wealth,

housing affordability, mortgage trends, retirement-income policy, and investment behavior.

No hype, no doom-scroll economics, and no “just skip coffee and you’ll be a millionaire” takes.

Let’s break down what truly matters mostand when.

Why This Question Is Bigger Than It Sounds

“What matters most?” sounds like a ranking question. In real life, it’s a timing question.

The same strategy can be brilliant at 30 and risky at 62. For example, if you’re early in your career,

your biggest advantage is timeso stock exposure often matters more than squeezing every dollar of home equity.

But if you’re close to retirement, predictable cash flow and claiming strategy can matter more than chasing

one extra point of portfolio return.

Another key point: money decisions are rarely independent. Mortgage rates affect how much you can invest.

Housing costs affect how much you can save. Social Security claiming age changes how much you must withdraw

from investments in your 60s. Everything is connected, like one giant family group chat where no one mutes notifications.

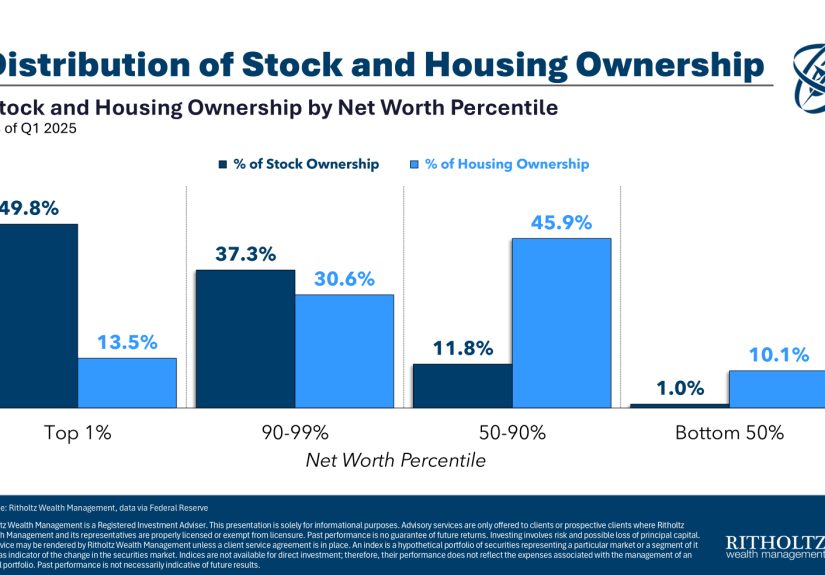

Where U.S. Households Stand Right Now

1) Wealth is concentrated in stocks and housing

At the national level, household balance sheets are still dominated by corporate equity and real estate.

That tells us one thing clearly: debates about “stocks vs. housing” miss the bigger realitymost wealth is built

through a combination of both.

2) Homeownership exists, but affordability pressure is real

U.S. homeownership remains around two-thirds of households, yet many buyers still face affordability friction:

higher monthly payments, persistent inventory constraints, and rate-sensitive budgets.

Translation: owning can still be a powerful wealth-building tool, but the entry cost has become more demanding.

3) Emergency resilience is improving, but uneven

A meaningful share of households report they can cover several months of expenses, but a large segment still

cannot. That matters because emergency fragility forces bad timing decisionslike selling investments in downturns

or taking on expensive debt.

4) Social Security remains essential, not optional

Social Security is not a side note in retirement planning. It is one of the only inflation-adjusted,

lifelong income streams most Americans can count on. But claiming age, work history, and policy timelines all

influence outcomes, so strategy matters.

Stocks: Your Growth Engine (But Only If You Respect Volatility)

Stocks historically do the heavy lifting for long-run wealth growth because businesses innovate, earnings grow,

and markets price that growth over time. But stocks also come with volatility, and volatility is fine until

it becomes emotional. The biggest portfolio risk for many households is not “the market”it’s panic behavior.

What stocks do best

- Compounding over decades: Time in the market beats trying to time the market.

- Inflation defense: Productive assets tend to adjust better than idle cash over long horizons.

- Liquidity: Unlike home equity, investments can be reallocated more easily.

Where people go wrong

- Over-concentrating in a few “story” stocks.

- Taking equity risk without an emergency fund.

- Ignoring taxes, fees, and behavior drag.

- Confusing a hot 12-month streak with a durable plan.

If your portfolio plan requires perfect nerves and perfect timing, it is not a plan. It is fan fiction.

A practical approach is boring on purpose: broad diversification, consistent contributions,

automatic investing, and periodic rebalancing. Boring is beautiful when your objective is financial freedom.

Housing: Stability, Leverage, and Lifestyle in One Asset

Housing is a financial asset and a life asset at the same time. That dual role makes it powerfuland tricky.

Your home can build equity, offer payment stability (with fixed-rate financing), and protect against rent inflation.

But it can also consume cash through maintenance, taxes, insurance, and transaction costs.

What housing does best

- Forced savings: Monthly principal payments can quietly build equity over years.

- Leverage: Small down payments can control larger assets (with risk).

- Behavioral stickiness: People are less likely to “trade” their home the way they trade stocks.

- Lifestyle utility: You live in itthis matters more than spreadsheet purists admit.

Where housing can hurt

- Buying at the edge of affordability with no cash buffer.

- Underestimating true carrying costs.

- Treating a primary home as a guaranteed high-return investment.

- Becoming “house rich, cash poor.”

Housing works best when it supports your life and your cash flow. The best home decision is not always

“buy bigger” or “buy now.” Sometimes the best move is to rent strategically while aggressively investing the difference.

Sometimes it’s buying modestly and keeping flexibility high. Wealth is less about winning one purchase and more about

surviving all the years after it.

Social Security: The Most Underestimated Retirement Asset

Many people obsess over portfolio size while underestimating guaranteed income. But in retirement planning,

predictability is priceless. Social Security can reduce sequence-of-returns risk by covering core expenses,

which means you may withdraw less from investments during bad markets.

Why it matters so much

- Lifetime income: You can’t outlive it.

- Inflation adjustments: Benefits are indexed through COLA mechanisms.

- Progressive design: Lower lifetime earners generally receive higher replacement rates.

- Spousal and survivor dimensions: Claiming choices affect household outcomes, not just individuals.

The claiming-age multiplier

Claiming early can permanently reduce monthly benefits; delaying can materially increase them.

This is one of the highest-impact retirement decisions many households ever make. A good claiming strategy

often beats endless tinkering with tiny investment allocations.

Policy realism without panic

Yes, long-term funding pressure exists and should be taken seriously. No, panic is not a strategy.

The practical response is to build flexibility: save consistently, control debt, keep working options open,

and model retirement with conservative assumptions. Hope is not a planbut neither is doom.

So… What Matters Most?

Here’s the honest answer:

what matters most is the weak link in your system.

- If you have no emergency buffer, cash resilience matters most.

- If you’re underinvested for your age, stock exposure and contribution rate matter most.

- If housing costs are crushing your budget, housing efficiency matters most.

- If retirement is near, Social Security claiming strategy and withdrawal planning matter most.

In other words, stop asking, “Which asset class wins?” and ask, “Which risk can hurt my household most in the next

3–10 years?” Fix that first.

A Practical Framework by Life Stage

In Your 20s–30s: Build the base

- Target consistent retirement contributions, ideally automated.

- Build a real emergency fund before maxing risk.

- Buy a home only if it improves, not destroys, monthly flexibility.

In Your 40s–50s: Optimize the middle game

- Increase savings rate with every raise.

- Reduce high-interest debt and prevent lifestyle creep.

- Run retirement projections with multiple market scenarios.

- Review insurance, estate basics, and tax efficiency.

In Your 60s+: Design income, not just returns

- Coordinate claiming strategy with spouse/survivor planning.

- Segment assets by time horizon (near-term cash vs long-term growth).

- Protect against sequence risk in the first retirement decade.

- Revisit housing fit: payment, maintenance burden, and location support.

Three Mini Case Studies

Case 1: “High salary, low net worth”

Jordan earns well, rents in a high-cost city, and invests inconsistently. The priority is not home buying pressure.

It’s automating 401(k) and brokerage contributions while building a six-month emergency reserve.

For Jordan, stocks + savings behavior matter most right now.

Case 2: “House rich, cash poor”

Priya owns a beautiful home but has minimal liquid reserves and frequent card balances.

One large repair could trigger expensive debt. Her priority is liquidity and cash-flow repair,

not chasing additional home upgrades. For Priya, resilience matters more than appreciation headlines.

Case 3: “Retiring soon, claiming uncertain”

Marcus is 63, has moderate investments, and wants to claim benefits immediately.

A delay analysis shows higher guaranteed monthly income if he waits, reducing later withdrawal stress.

For Marcus, Social Security strategy matters mostmore than trying to out-trade market volatility.

Common Mistakes That Quietly Cost a Fortune

- Ranking assets instead of building a system.

- Ignoring inflation and assuming flat living costs in retirement.

- Using home equity as a “plan” without a liquidity strategy.

- Letting short-term market fear break long-term investing discipline.

- Treating Social Security as an afterthought instead of a core income pillar.

The Bottom Line

Stocks, housing, and Social Security are not competitorsthey are teammates.

The strongest financial plans do not worship one pillar. They coordinate all three.

Stocks grow your future, housing stabilizes your present, and Social Security protects your longevity risk.

What matters most is not a universal ranking. It is the next strategic move that reduces your biggest vulnerability.

If you remember one thing, remember this: financial security is usually built through thousands of ordinary,

repeatable decisions, not one perfect call. Automatic investing. Sensible housing costs. Thoughtful claiming.

A buffer for bad surprises. Do that long enough and “What matters most?” becomes easier to answer:

your system works because all three pillars are doing their jobs.

Experience Notes (Extended 500+ Words): Real-World Patterns Behind Stocks, Housing & Social Security

The most useful way to understand this topic is to watch how real households behave during good years,

bad years, and “everything costs more than expected” years. Across hundreds of common money situations

(from young professionals to near-retirees), one pattern shows up again and again: people who win financially

rarely have perfect timing, but they usually have clear priorities.

In up markets, confidence rises fast. People start asking if they should go all-in on stocks because recent returns

look great. The households that stay grounded usually do three boring things: they keep an emergency cushion,

continue automatic contributions, and avoid concentration bets. They still enjoy market growth, but they don’t

build a fragile plan that collapses when volatility returns. Their mindset is, “I want to participate, not gamble.”

That one sentence often saves years of recovery.

In expensive housing markets, I’ve seen two opposite mistakes. First, some buyers rush in with razor-thin cash buffers

because they fear being priced out forever. Second, some renters delay all investing while waiting for a “perfect”

buying moment that never arrives. The more durable approach is balance: keep investing regardless of housing status,

and buy only when the monthly payment, reserve requirements, and life stability align. A home can be a wealth tool,

but only if it doesn’t suffocate the rest of the plan.

Mid-career households often face the “squeeze decade”: childcare, aging parents, career pivots, and rising insurance

costs all at once. This is where the three-pillar framework becomes practical. Stocks remain the growth engine,

housing remains the stability anchor, and Social Security becomes a planning variable rather than a mystery box.

Households that do best in this phase review contributions annually, refinance or adjust housing costs when possible,

and run retirement projections with conservative assumptions. They don’t need perfect certaintyjust regular calibration.

Near retirement, behavior changes quickly. People become less interested in maximum returns and more interested in

sleeping well. This is exactly where Social Security strategy becomes powerful. When households model claiming ages

side-by-side, the decision often feels less emotional and more mathematical. Delaying benefits can act like buying

more inflation-aware lifetime income, which reduces pressure on portfolio withdrawals. Not everyone should delay,

but everyone should model the tradeoffs in detail.

Another recurring experience: couples frequently discover they had different “money definitions” of safety.

One partner views paid-off housing as security. The other views liquid investments as security. Both are reasonable.

The best conversations acknowledge both needs and design a blended plan: manageable housing costs, diversified

investment exposure, and a clear Social Security claiming map. The argument fades when the system serves both values.

During periods of high inflation, the strongest households usually avoid extreme moves. They don’t abandon markets.

They don’t over-leverage into housing. They tighten spending where possible, keep contributions going, and protect

emergency liquidity. They understand that resilience is a return strategy, too. If you can avoid forced selling,

forced borrowing, and forced panic, compounding has a chance to do its job.

The most encouraging pattern of all is this: progress tends to arrive quietly, then suddenly. A household that felt

“behind” for years can look dramatically stronger after 24–36 months of steady behaviorautomated investing, controlled

housing costs, and smarter retirement-income decisions. There is no viral shortcut here. But there is a reliable path.

And for most people, that path is enough.

Conclusion

If you want a one-line verdict: the winner is integration. Stocks build growth, housing builds

stability, and Social Security builds durability. The question is not which pillar to worship; it is which pillar

needs reinforcement in your household right now. Fix that, then keep going. Money success is rarely flashy.

It is repeatable.