Table of Contents >> Show >> Hide

- From Treats to “Non-Negotiables”: How Lifestyle Creep Works

- The Psychology Behind It: Hedonic Adaptation and Social Comparison

- When Luxuries Crowd Out Your Future Wealth

- Signs Your Luxuries Have Quietly Become “Needs”

- A Wealth-of-Common-Sense Way to Reclaim Control

- Spending Less Without Feeling Deprived

- Real-Life Snapshots: When Luxuries Quietly Took Over

- Bringing It All Together

- SEO Metadata

Have you noticed how your “must-have” list keeps getting longer? One day you’re thrilled to have Wi-Fi at home. A few years later, you’re paying for gigabit internet, five streaming services, cloud storage, smart lights, and a fridge that sends you passive-aggressive notifications about milk.

That quiet creep from “nice extra” to “basic requirement” is more than just modern convenience. It’s a financial force with a real name: lifestyle creep. When luxuries become necessities, your budget gets squeezed, your savings rate shrinks, and your future options narrow. The worst part? It usually feels completely normal while it’s happening.

In the spirit of A Wealth of Common Sense, let’s look at how this shift happens, why our brains are wired for it, and how to keep your spending aligned with your actual values instead of whatever your social feed is selling this week.

From Treats to “Non-Negotiables”: How Lifestyle Creep Works

Lifestyle creep (or lifestyle inflation) is what happens when your spending rises alongside your income, and yesterday’s luxuries turn into today’s baseline. A fancier apartment, better car, premium phone, business-class flights, gourmet coffee, and higher-end vacations all feel justified because, technically, you can afford them.

The problem isn’t enjoying your money. The problem is when almost every upgrade becomes permanent. Instead of extra cash going to savings, investing, or debt payoff, it quietly disappears into subscriptions, upgrades, and conveniences that barely feel special anymore.

Modern Examples of Luxuries Turned “Essentials”

- Connectivity: High-speed internet, smartphones, and data plans are now treated like oxygen. Cutting back feels unthinkable, even if the plan is far more than you need.

- Streaming: What used to be “maybe Netflix” has turned into a small cable bundle made of apps. Most people now juggle multiple platforms as if they were utilities.

- Transportation: Instead of a reliable, modest car, bigger and more luxurious vehicles are increasingly common, even as family sizes shrink and commutes get shorter.

- Food & coffee: Takeout, delivery apps, and daily specialty coffees quietly replace home-cooked meals and drip coffee, often justified as “time-saving.”

- Home comforts: Designer furniture, smart devices, and constant décor upgrades can turn a perfectly functional home into an ongoing project.

None of these are bad on their own. The issue is scale. When every category gets upgraded at once, your “normal” lifestyle can easily outgrow your income growth.

The Psychology Behind It: Hedonic Adaptation and Social Comparison

The reason luxuries quickly stop feeling luxurious comes down to psychology. Two big forces are at work: hedonic adaptation and comparison.

Hedonic Adaptation: The “New Normal” Problem

Hedonic adaptation is the tendency to quickly get used to positive changes. A new phone, car, or kitchen remodel makes you happy for a while, but soon that new standard becomes your baseline. The thrill fades; the bill does not.

That’s why “just one upgrade” rarely stays as one. You move to a nicer apartment; suddenly, your furniture looks cheap. You buy a luxury car; now the old vacations feel basic. Your brain keeps raising the bar, telling you that the new level is “normal” and anything less would be a sacrifice.

Social Comparison: Keeping Up, Not Just Catching Up

Humans are social creatures. We constantly compare our lifestyles to friends, coworkers, neighbors, and influencers we’ve never met. Thanks to social media, you now see everyone’s best upgrades, not their trade-offs.

When your peers normalize frequent travel, premium gadgets, or expensive kids’ activities, you start to see those things as “standard” instead of “fancy.” That subtle pressure can push your spending higher without you ever consciously deciding, “I want to spend more and save less.”

When Luxuries Crowd Out Your Future Wealth

In a perfect world, higher income would mean higher savings and a slightly nicer lifestyle. In reality, for many people, income goes up and the savings rate barely moves. The gap between what you could be saving and what you’re actually saving gets swallowed by subscriptions, upgrades, and conveniences.

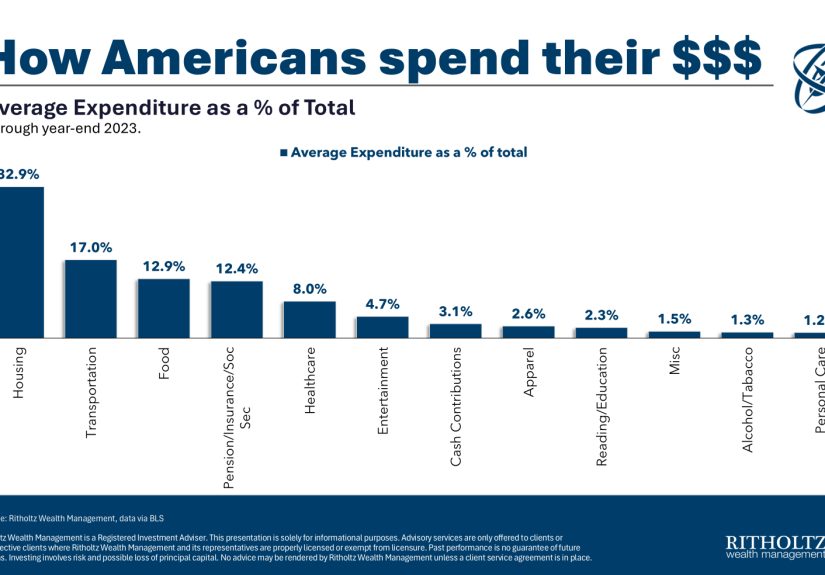

Think about a typical monthly budget:

- Rent or mortgage

- Car payment or two

- Childcare or kids’ activities

- Groceries and dining out

- Internet, phone, and streaming bundles

- Gym, apps, cloud storage, gaming, and other memberships

Each category can be defended. “We need good internet for work.” “The SUV is safer.” “The kids love these classes.” “Streaming is cheaper than going out.” All true individually. But put them together and they can crowd out retirement contributions, emergency savings, college funds, and debt payoff.

This is where a “wealth of common sense” approach comes in: your big money decisions matter far more than small hacks. If housing, cars, and lifestyle extras all operate at “max comfort,” it’s very hard to build long-term wealth no matter how many coupons you clip.

Signs Your Luxuries Have Quietly Become “Needs”

How do you know when you’ve crossed the line from enjoying your money to letting lifestyle creep run the show? A few red flags:

- You feel “broke” at a higher income. You earn more than ever, yet there’s still “nothing left” at the end of the month.

- Cutting anything feels impossible. You mentally label dozens of optional expenses as “non-negotiable.”

- You upgrade automatically. New phone hits the market? New trim level on a car? You barely question it.

- You finance wants like needs. Payment plans and “buy now, pay later” cover everyday indulgences that used to be treats.

- Your savings rate is flat or falling. Raises show up in your lifestyle, not in your investment accounts.

If any of that feels familiar, you’re not failing at money; you’re just human. But human behavior is exactly what you can work with.

A Wealth-of-Common-Sense Way to Reclaim Control

You don’t have to move into a van, live on rice and beans, or swear off fun forever. A common-sense financial approach is about intentional trade-offs. You can absolutely enjoy luxuries just not all of them, all at once, all the time.

1. Start With the Big Three: Housing, Cars, and Lifestyle

Most budgets are dominated by three categories. If you get these roughly right, everything else gets easier:

- Housing: Bigger isn’t always better. A slightly smaller or less trendy place can free up hundreds of dollars a month without destroying your quality of life.

- Transportation: A reliable, reasonably priced car that you keep for many years often beats a fancy model with big depreciation and financing costs.

- Everyday lifestyle: Dining out, subscriptions, shopping, and hobbies add up quickly. Decide which ones truly make life better and trim the rest.

Think of these choices as the framework of your financial house. Once the structure is solid, you can decorate however you like.

2. Run the “Would I Take a Pay Cut for This?” Test

For any recurring expense, ask:

“If my employer offered me a small permanent pay cut in exchange for this service forever, would I say yes?”

If the answer is an easy no, that expense probably isn’t a true necessity it’s just something you’ve gotten used to.

3. Separate Your Spending Into Three Buckets

- Essentials: Housing, basic transportation, food at home, insurance, utilities, minimum connectivity for work and life.

- Joyful Add-Ons: Things that genuinely make your life better and that you would miss: a streaming service you actually use, a hobby you love, trips to see family, a gym you attend regularly.

- Status Fluff: Purchases mostly driven by impressing others or keeping up appearances: name-brand upgrades you barely notice after a week, extra subscriptions you forget about, high-end items that live in a closet.

The goal isn’t to eliminate all Joyful Add-Ons. It’s to ruthlessly cut the Status Fluff and keep your Essentials from quietly inflating.

4. Use Automation For Saving, Not Just Spending

Many luxuries stay in our lives because they’re on auto-pay. Use that same power in your favor:

- Set up automatic transfers to savings and investment accounts right after each paycheck.

- Increase contributions whenever you get a raise, before your lifestyle catches up.

- Only then decide how much is left for upgrades or extras.

This “pay yourself first” method quietly turns savings into its own kind of non-negotiable “necessity.”

Spending Less Without Feeling Deprived

Here’s the twist: research suggests that spending less and spending more intentionally can actually make you happier. When you eliminate mindless consumption, you give yourself space to savor what you keep.

A few practical strategies:

- Rotate luxuries. Instead of stacking six streaming services, keep one or two at a time and rotate monthly. Each platform will feel fresh again.

- Upgrade slowly. When income rises, let your savings rate improve first. Add only one meaningful upgrade instead of several automatic ones.

- Focus on experiences over status. Time with people you love, learning new skills, or exploring nature often bring more lasting satisfaction than status purchases.

- Practice “temporary downgrades.” Try a cheaper phone plan, fewer restaurant meals, or a smaller car for a year. See if your happiness actually drops as much as you imagine.

You’re not trying to win some frugality contest. You’re trying to design a lifestyle where your current self is happy and your future self isn’t furious with you.

Real-Life Snapshots: When Luxuries Quietly Took Over

To really feel how this plays out, it’s helpful to look at a few stories the kind you might recognize in yourself or people you know.

The Young Professional With the “Harmless” Upgrades

Jenna starts her career earning $50,000. She lives with roommates, drives a paid-off used car, and cooks at home most nights. She’s not living large, but she’s saving consistently.

Five years later, Jenna earns $90,000. Along the way, she:

- Upgrades to a nicer one-bedroom apartment.

- Leases a new SUV “because the payment fits in the budget.”

- Adds a handful of subscriptions: three streaming platforms, a meal kit, a fitness app, and a monthly beauty box.

- Eats out or orders in multiple times per week due to “long days at work.”

There’s nothing outrageous here. But her savings rate barely improved even as her income almost doubled. She feels like she’s “doing okay,” but she can’t figure out why she’s not further ahead.

Once she sits down and runs the numbers, she realizes that small lifestyle upgrades all of which felt reasonable have absorbed almost every raise. Her solution isn’t to move into a tiny apartment and sell everything. Instead, she:

- Gives up the most expensive streaming and keeps one she truly uses.

- Cancels the beauty box and meal kit, shifting those dollars to a higher 401(k) contribution.

- Commits to making big spending decisions only once a year instead of reacting to every new temptation.

Suddenly, her savings rate jumps, and she doesn’t feel deprived she just feels less scattered.

The Family That Realized “Kid Expenses” Weren’t All Mandatory

A couple with two kids noticed that even with decent incomes, they felt like they were always one unexpected bill away from stress. When they listed their expenses, they were shocked by how many things felt like “for the kids” but were actually optional luxuries: multiple streaming services “for family movie night,” restaurant meals after practice, several expensive extracurriculars, and constant new gear.

They decided to:

- Keep one main streaming service and use the library for DVDs and books.

- Limit paid activities and focus more on free family time: parks, board games, bike rides.

- Set a clear monthly limit for “fun spending” and involve the kids in choosing what matters most.

The kids still felt loved and entertained. The parents felt less guilty and more in control. Their lifestyle was still comfortable just less padded with auto-pilot spending.

The Empty Nesters Who Wanted Freedom More Than Fancy

Another couple hit their late 50s with good incomes but not enough saved to retire on their timeline. Their lifestyle had grown steadily over the years: a big house, two leased vehicles, frequent travel, and an ongoing stream of upgrades.

When they finally sat down with a financial planner, they realized that if they kept things exactly as they were, they’d either have to work much longer or accept a steep drop in lifestyle later.

So, they made a decision: they’d rather tighten up now than feel trapped later. Over three years, they:

- Downsized their house, freeing up equity and reducing maintenance costs.

- Switched to one paid-off car and one older second vehicle.

- Shifted from first-class or premium travel to more modest trips or fewer, more meaningful ones.

Their friends thought they were “downshifting.” But the couple felt something else: relief. They weren’t giving up luxuries; they were exchanging constant upgrades for something better time.

Bringing It All Together

When luxuries become necessities, they stop feeling special and start quietly dictating your financial life. A wealth-of-common-sense approach doesn’t tell you to live like a monk. It simply asks:

“If I didn’t already have this, would I actively choose to buy it today at this price, with these trade-offs?”

Ask that question about your car, your home, your subscriptions, your gadgets, and your daily habits. Some things will easily survive the test. Others won’t.

The goal isn’t to squeeze every ounce of fun out of your budget. It’s to build a life where comfort, joy, and security coexist where your luxuries are chosen on purpose, not automatically promoted to “needs,” and where your future self can look back and say, “That was money well spent.”