Table of Contents >> Show >> Hide

- First: Know What “Taking Money Out” Really Means

- The Quick Decision Tree (Pick Your Adventure)

- Option 1: The “Cleanest” MoveDo a Direct Rollover (Not a Withdrawal)

- Option 2: Take a Regular Withdrawal (Distribution)

- Option 3: Use the Rule of 55 (Early Access Without the 10% Penalty)

- Option 4: Hardship Withdrawal (When Life Happens)

- Option 5: 401(k) Loan (Borrow From YourselfWith Strings Attached)

- Option 6: Substantially Equal Periodic Payments (SEPP / “72(t)”)

- Option 7: Required Minimum Distributions (RMDs)

- Traditional vs. Roth 401(k): Your Tax Result Depends on the Bucket

- How to Actually Take Money Out (Step-by-Step)

- Smart Alternatives Before You Tap the 401(k)

- Frequently Asked Questions

- Conclusion: Keep the Money Working (If You Can)

- Experiences & Real-World Scenarios (What People Commonly Run Into)

Needing cash is normal. Needing cash from your 401(k) is… also normal, but with extra paperwork and a side of tax seasoning. The good news: there are multiple ways to take money out of a 401(k) plan, and not all of them are “cash it out, cry later.” The bad news: the IRS has rules, your employer’s plan has rules, and your future self has opinions.

This guide walks you through the most common 401(k) withdrawal options (including rollovers, loans, hardship withdrawals, the Rule of 55, and required minimum distributions), how taxes and penalties generally work, and the smartest decision pathwithout drowning you in legalese. (We’ll keep it in plain American English with only a light mist of “consult a pro.”)

First: Know What “Taking Money Out” Really Means

People say “I want to cash out my 401(k)” when they might mean one of these very different moves:

- A withdrawal (distribution): Money leaves the retirement plan and goes to you.

- A rollover: Money leaves the plan but goes directly to another retirement account (like an IRA or a new employer’s plan).

- A 401(k) loan: Money leaves your investment lineup temporarily… and you repay it (to yourself) with interest.

- An in-service withdrawal: You’re still working there, but the plan allows a distribution (often after a certain age).

- Required minimum distributions (RMDs): The “the government would like its tax revenue now” withdrawals at older ages.

Your plan’s rules matter because the IRS sets the outer boundaries, but your employer decides what the plan actually allows. Translation: two coworkers can have the same problem and totally different 401(k) options.

The Quick Decision Tree (Pick Your Adventure)

- Are you leaving (or have you left) the job that sponsors the 401(k)?

If yes, you likely have the widest set of options: rollover, leave it, or withdraw. - Are you age 59½ or older?

If yes, you can usually withdraw without the early withdrawal penalty (taxes may still apply). - Did you separate from service in the year you turned 55 or later?

If yes, you may qualify for the Rule of 55 (penalty-free withdrawals from that employer’s plan). - Is this a true emergency and your plan offers hardship withdrawals?

If yes, you might be able to take a hardship distribution (usually taxable, sometimes penalized). - Could a loan solve the problem without triggering taxes/penalties?

If your plan allows loans, this may be the least tax-painful routeif you can repay it.

Option 1: The “Cleanest” MoveDo a Direct Rollover (Not a Withdrawal)

If you don’t absolutely need the cash in your checking account, a direct rollover is usually the best way to move money out of a 401(k) without turning it into a tax event. With a direct rollover, your plan sends the money straight to:

- an IRA (traditional or Roth, depending on what you’re rolling over), or

- a new employer’s retirement plan (if they accept rollovers).

Why direct rollovers are popular

- No current tax hit (for traditional-to-traditional rollovers).

- No mandatory 20% withholding that often applies when the check is made out to you.

- Keeps retirement money working (instead of shrinking via taxes, penalties, and impulse purchases labeled “just one small treat”).

Watch out for the “60-day rollover” trap

If the money is paid to you first (an indirect rollover), you generally have a limited window (often 60 days) to deposit it into another retirement account. Here’s the gotcha: many plans must withhold 20% for federal taxes when a taxable distribution is paid to you. To roll over the full amount, you may need to replace that withheld 20% out of pocketthen wait to recover it at tax time, if applicable.

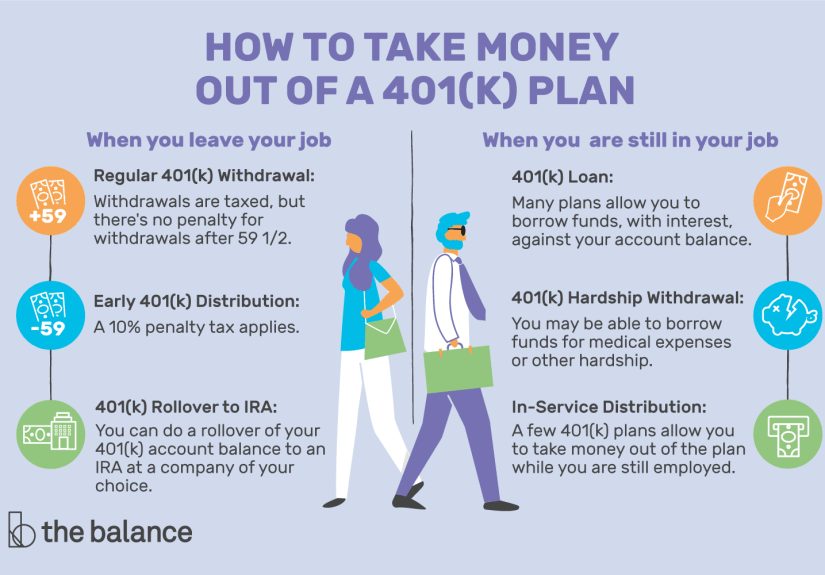

Option 2: Take a Regular Withdrawal (Distribution)

A regular 401(k) withdrawal puts money in your hands. This is straightforward mechanicallyand often expensive financially. In general, withdrawals from traditional 401(k) money are taxed as ordinary income. Withdrawals from Roth 401(k) money may be tax-free if they’re “qualified.”

When can you take a withdrawal?

Common situations include:

- After leaving your job: most plans allow distributions once you separate from service.

- After age 59½: withdrawals are generally no longer “early” for penalty purposes.

- In-service (while still employed): some plans allow it (often at 59½+), others don’t. Check your Summary Plan Description (SPD).

- At RMD age (later in life): you may have to start taking minimum distributions (more below).

Taxes and the 10% early withdrawal penalty (the part everyone forgets)

If you withdraw taxable money before age 59½, you may owe:

- Ordinary income tax on the taxable portion, plus

- an additional 10% penalty unless an exception applies.

Quick example: Suppose you withdraw $20,000 from a traditional 401(k) at age 45. If you’re in the 22% federal bracket and you owe the 10% penalty, that’s roughly 32% combined before any state taxes. You could lose about $6,400 to federal costs alone, leaving around $13,600. (Real life varies based on income, state taxes, and the specific distribution typebut you get the idea: the IRS keeps a tip jar.)

Option 3: Use the Rule of 55 (Early Access Without the 10% Penalty)

The Rule of 55 can be a lifesaver for early retireesor anyone who “retired” unexpectedly via layoff. If you separate from your employer during or after the calendar year you turn 55, withdrawals from that employer’s 401(k) may avoid the 10% early withdrawal penalty. You still generally owe ordinary income taxes on taxable amounts.

Important Rule of 55 fine print

- It usually applies only to the 401(k) of the employer you just left, not old 401(k)s and not IRAs.

- If you roll that account into an IRA, you may lose Rule-of-55 access.

- Plan rules still mattersome plans offer flexible partial distributions; others are more rigid.

Option 4: Hardship Withdrawal (When Life Happens)

If your plan allows it, a hardship distribution may be available for an “immediate and heavy financial need.” Hardship withdrawals are generally limited to the amount necessary to meet the need (sometimes including taxes/penalties triggered by the withdrawal).

Common hardship categories

Plans often use IRS safe-harbor categories such as certain medical expenses, costs to purchase a principal residence (not mortgage payments), tuition and education expenses, preventing eviction/foreclosure, funeral expenses, and certain disaster-related expenses. Your plan document (and your HR/recordkeeper portal) is the final referee.

Hardship withdrawal downsides

- Usually taxable (unless it’s Roth contributions being distributed).

- May also be penalized if you’re under 59½ and no exception applies.

- Typically cannot be rolled over to an IRA or another plan.

- Permanent account shrinkage: you’re removing money that can no longer compound inside the plan.

Option 5: 401(k) Loan (Borrow From YourselfWith Strings Attached)

If your plan permits loans, a 401(k) loan can provide cash without immediate income taxes or early withdrawal penalties, as long as the loan follows the rules and you repay it properly.

Typical loan limits and repayment rules

- You may be able to borrow up to 50% of your vested balance, capped at $50,000 (common IRS-based limits).

- Loans typically must be repaid within 5 years, unless used to purchase a principal residence.

- Repayments are usually made at least quarterly, in substantially level payments (principal + interest).

The big risk: job change + loan = surprise taxes

If you leave your employer (voluntarily or not) and can’t repay on schedule, an outstanding loan can become a taxable distribution. That could mean ordinary income taxes and possibly the 10% penalty. So a 401(k) loan is best for people who have stable repayment capacityand a backup plan if employment changes.

Option 6: Substantially Equal Periodic Payments (SEPP / “72(t)”)

Need early access before 59½ and the Rule of 55 doesn’t apply? A SEPP plan (often called a “72(t) distribution”) can allow penalty-free withdrawals if you follow strict IRS rules.

Why SEPP is both helpful and terrifying

- You must take substantially equal periodic payments calculated using IRS-approved methods.

- The schedule must generally continue for at least 5 years or until age 59½, whichever is longer.

- If you modify or stop payments incorrectly, the IRS can assess retroactive penalties (plus interest).

SEPP is not a casual “try it and see” strategy. It’s more like a long-term subscription plan you can’t cancel without a fee. If you’re considering it, it’s smart to work with a tax professional who has done SEPP calculations before.

Option 7: Required Minimum Distributions (RMDs)

At older ages, certain retirement accounts require annual minimum withdrawals. For many people, RMDs begin at age 73. Some workplace plans allow you to delay RMDs if you’re still working (with common exceptions for certain owners), but rules can vary.

Key RMD mechanics

- Your RMD is calculated from your prior year-end balance and IRS life expectancy tables.

- Missing an RMD can trigger a significant excise tax, although corrections may reduce the penalty in certain cases.

- Roth IRAs generally do not have lifetime RMDs for the original owner, and designated Roth accounts in some plans may also avoid lifetime RMDs for the account owner under current rulesconfirm with your plan.

Traditional vs. Roth 401(k): Your Tax Result Depends on the Bucket

Many people have both traditional (pre-tax) and Roth (after-tax) money in the same 401(k). The tax treatment differs:

Traditional 401(k)

- Contributions often reduced taxable income when you made them.

- Withdrawals are generally taxed as ordinary income.

Roth 401(k)

- Contributions were made with after-tax dollars.

- A “qualified distribution” of Roth 401(k) earnings can be tax-free if it meets the age/trigger requirement and the 5-year rule.

Practical tip: When you request a distribution, ask the recordkeeper how the withdrawal will be sourced (pro-rata across contributions/earnings or from specific sources) and how it will be reported on Form 1099-R. This prevents surprise taxes and prevents you from screaming into a pillow in April.

How to Actually Take Money Out (Step-by-Step)

- Find your plan’s Summary Plan Description (SPD).

Search your benefits portal for “SPD,” “distributions,” “loans,” and “hardship.” - Identify your eligible option.

Leaving job? Consider direct rollover first. Still employed? Check if in-service withdrawals are allowed. Emergency? Compare hardship vs. loan. - Estimate the tax impact before you click “Submit.”

Ask: Will there be mandatory withholding? Will this raise my tax bracket? Will I owe a 10% penalty? - Choose the payout method.

Many plans offer lump sums, partial withdrawals, or installments. Installments can help manage taxes by spreading income across tax years. - Complete the distribution/loan request.

Online portals are common. Hardship withdrawals may require documentation or certifications. - Track the paperwork for taxes.

You’ll generally receive Form 1099-R showing the distribution type and taxable amount. Keep it with your tax documents.

Smart Alternatives Before You Tap the 401(k)

Sometimes the “best” 401(k) withdrawal is… not doing it. Before taking money out, consider:

- Budget triage: pause nonessential expenses for 30–60 days to reduce the cash need.

- Emergency fund or short-term savings: if available, it’s usually less costly than retirement withdrawals.

- Low-interest personal loan or credit union loan: may be preferable to a penalty-heavy distribution.

- Roth IRA contributions (not earnings): if you have a Roth IRA, contributions can often be withdrawn tax- and penalty-free (different rules than Roth 401(k)).

Frequently Asked Questions

Can I withdraw from my 401(k) while still employed?

Sometimes. Many plans restrict in-service withdrawals, while others allow them (commonly after age 59½). Your plan’s SPD and recordkeeper portal will tell you what’s available.

Is the 20% withholding the same as the tax I owe?

Not necessarily. Withholding is a prepayment toward your tax bill. Your actual tax owed depends on your total income and deductions. You may owe more (or get some back) when you file.

Can I put money back after a hardship withdrawal?

Typically, hardship distributions can’t be repaid to the plan like a loan, and they generally can’t be rolled over. That’s why hardship should be a last resort when other resources won’t work.

What’s usually better: a 401(k) loan or a withdrawal?

A loan can avoid current taxes and the 10% early withdrawal penalty, but it carries repayment riskespecially if you leave your job. A withdrawal is simpler but can be much more expensive after taxes and penalties. “Better” depends on your timeline, job stability, and ability to repay.

Conclusion: Keep the Money Working (If You Can)

Taking money out of a 401(k) plan isn’t automatically a mistakebut it’s rarely “free money.” If you can avoid a taxable distribution, a direct rollover is usually the cleanest route. If you truly need funds, prioritize options that reduce penalties (like the Rule of 55, qualified exceptions, or a properly structured loan), and always run the tax math first.

Most importantly, your 401(k) is designed to fund Future You. If you borrow from it, make a plan to pay Future You back because Future You is already dealing with enough, like choosing between fiber supplements and exciting new knee technology.

Experiences & Real-World Scenarios (What People Commonly Run Into)

Let’s talk about what happens outside the tidy world of bullet pointsbecause real life doesn’t arrive in an IRS-approved format. Below are common “experiences” people report when trying to take money out of a 401(k), based on typical plan processes, rules, and the kind of practical hiccups that never show up in the marketing brochure.

1) The “I’ll just cash it out” moment (and the April surprise)

A classic scenario: someone leaves a job, sees a five-figure balance, and thinks, “This will fix everything.” They request a lump-sum withdrawal, money shows up in their bank account, and for a few glorious weeks it feels like adulthood is under control.

Then tax season arrives with a plot twist. The plan may have withheld federal taxes automatically, but the total tax bill can still be larger once income is calculated for the year. Add the 10% early withdrawal penalty (if under 59½ and no exception applies), plus state taxes, and suddenly that “fix everything” balance was more like “fix one thing, briefly.”

The practical lesson people learn (often the hard way): a 401(k) cash-out is not just spending retirement moneyit’s paying a premium to spend it early.

2) The indirect rollover scramble (aka the 60-day sprint)

Another common experience: someone intends to roll over their 401(k) but chooses “send me the check” because it feels faster or more controllable. That’s when the mandatory withholding can create a scramble. The check arrives for less than expected because a chunk was withheld for taxes, and now the person has a short window to deposit the full amount into an IRA to avoid taxation on the withheld part.

This is how perfectly responsible adults end up asking themselves questions like, “Can I temporarily borrow money from my savings so I can roll over money I already had… so I don’t get taxed on money I didn’t actually keep?” (Yes, it’s as fun as it sounds.)

People who want the least drama usually choose a direct rollover, where the money goes straight to the receiving institution. Fewer steps. Fewer deadlines. Fewer sweaty palms.

3) The 401(k) loan that turns into a job-change problem

401(k) loans are often described as “borrowing from yourself,” which is truebut incomplete. What people experience is that the loan feels easy at the beginning: quick approval, money arrives, repayments come out of paychecks. Then a job change happens. Or a layoff. Or a career pivot. Suddenly the repayment rules may accelerate, and the outstanding balance can become taxable.

The “experience takeaway” is that a 401(k) loan works best when you have a stable plan to repay, and a backup plan if employment changes. Many people now ask a simple question before borrowing: “If I left this job in six months, could I pay this off?” If the answer is “LOL,” a loan may be riskier than it looks.

4) The hardship withdrawal paperwork reality

Hardship withdrawals feel like they should be instantbecause the hardship is instant. In practice, people often experience documentation steps, plan-specific definitions, and a need to show that the amount requested matches the need. Some recordkeepers make it fairly smooth; others make it feel like you’re applying for a mortgage using only screenshots and hope.

Also, many people underestimate how “permanent” a hardship distribution feels later. It’s not like a loan that you repay. Once the money leaves, the account balance (and future compounding) is smaller. People often describe regret not because they took the money, but because they didn’t explore alternatives first or didn’t understand the full tax cost.

5) The “Rule of 55” lightbulb moment

One of the more positive experiences shows up for early retirees or people who left a job at 55+ and discover the Rule of 55. The reaction is usually something like, “Wait… I can access this without the 10% penalty?” It can be a genuine reliefespecially if someone needs bridge income before Social Security or before other assets are accessible.

The catch people learn: it’s very plan-specific and employer-specific. Rolling the account away too early can eliminate that advantage. The best “experience-based” move is often to slow down, confirm eligibility, and think through withdrawals over time to manage taxes.

Bottom line: the most common real-world win isn’t a clever loopholeit’s simply picking the least expensive option for your situation and understanding the rules before you click the final confirmation button.