Table of Contents >> Show >> Hide

- The “Swallowing” Effect: When One Market Becomes the Market

- Why the Money Keeps Flowing to the U.S.

- Stocks Aren’t GDP… But the Gap Still Turns Heads

- History Check: “Swallowing” Is Not a Straight Line

- The Hidden Risks of a U.S.-Heavy World

- So… Should You Fight It or Ride It?

- Conclusion: The U.S. Might Be Eating the Buffet, But The World Still Has Dessert

- Investor Experiences: What This U.S.-Dominance Era Feels Like

If global stock markets were a potluck dinner, the United States didn’t just bring a dish it showed up with a full catering truck,

a dessert bar, and a sign that says “please form an orderly line.” Over the past decade-plus, U.S. assets have pulled in an outsized

share of attention, capital, headlines, and (most painfully) comparison charts. For investors, it can feel like the rest of the world

is shrinking… even though it’s very much still there, still innovating, still growing, and still occasionally doing that thing where it

wildly outperforms when everyone least expects it.

So what’s going on? Why do U.S. markets loom so large in indexes, in portfolios, and in our collective financial imagination?

And more importantly: what should a real-life investor do about it, beyond refreshing their app and whispering “Magnificent Seven”

like it’s a spell?

The “Swallowing” Effect: When One Market Becomes the Market

Start with the simple math of scale. Global equity market capitalization is enormous well into the hundreds of trillions of dollars

and it has been growing. But within that big number, the U.S. has been taking up a historically large slice of the pie in major global

equity measures, approaching roughly two-thirds to around 70% by some index-based calculations at the end of 2024. That’s a “wow”

number, even for people who pretend they don’t say “wow” at numbers.

At the same time, broad U.S. benchmarks still describe only one country’s listed corporations. The S&P 500, for instance, is designed

as a large-cap U.S. equity gauge and covers a substantial share of U.S. market value. Yet when global investors buy “the market”

through cap-weighted global indexes, they often end up buying “a lot of America” almost by default.

It’s not just the U.S. it’s a handful of giants inside the U.S.

The modern dominance story has a twist: concentration. A small set of mega-cap companies has grown so large that they don’t just move

the U.S. market; they tug on the whole world’s market-cap gravity. By the end of 2024, fewer than 40 mega-cap names (including the

widely discussed “Magnificent 7”) accounted for more than 30% of global equity capitalization in one major breakdown. That’s not a typo

it’s a reminder that “diversified” can still mean “everyone owns the same behemoths.”

This shows up inside U.S. indexes too. By late 2025, the top 10 companies represented roughly 40% of the S&P 500’s market cap in a

widely-circulated institutional chart set. So even if you’re “only” buying the U.S., you may be buying a very specific version of the U.S.:

mega-cap, growth-tilted, tech- and communications-heavy, and closely tied to AI expectations.

Why the Money Keeps Flowing to the U.S.

The U.S. isn’t dominating global portfolios for one single reason. It’s more like a greatest-hits album of advantages

and the tracks keep getting radio play.

1) Deep markets, strong plumbing, and a culture of “sure, let’s fund that”

U.S. capital markets are huge, liquid, and (for all their chaos) built to finance risk. Investors can buy public equities with tight spreads,

access vast ETF lineups, trade options, and move in and out with relative ease. International investors also treat the U.S. as a kind of

financial “default setting” especially in periods of uncertainty.

This is visible in market activity and scale statistics: global equity market capitalization rose notably in 2024, and U.S. markets remain a

central hub for trading and capital formation. Whether you view that as “efficient” or “a little unhinged” depends on your caffeine intake.

2) Productivity and the post-pandemic business formation burst

The U.S. has also benefited from relatively strong economic momentum in recent years, including productivity improvements and a surge in

entrepreneurial activity. The Census Bureau’s Business Formation Statistics track new business applications at high frequency and the

level of business creation activity since the pandemic has remained a major talking point in economic and market commentary.

Productivity matters because, over the long run, it supports rising real incomes, corporate earnings power, and the ability to invest in new

technologies. The Bureau of Labor Statistics regularly reports productivity changes, and the post-2019 period has seen meaningful swings

that investors watch closely as a signal of sustainable growth.

3) The dollar’s starring role

Global investing isn’t only about stock selection it’s also about currency. When the U.S. dollar is strong, U.S.-based investors may see

foreign returns look weaker when translated back into dollars. When the dollar weakens, foreign returns can look better. Either way, the

dollar is a huge character in this story, and broad trade-weighted measures show it has been elevated in recent years, affecting relative

performance comparisons across regions.

4) AI, earnings narratives, and valuation “permission slips”

A big reason U.S. equities have outpaced international peers since the aftermath of the 2008 financial crisis is sector composition and

earnings leadership especially in technology and communication services. In 2024, U.S. equities outperformed the rest of the world by

a wide margin in some major index comparisons, and much of the conversation centered on AI-adjacent businesses.

Here’s where it gets spicy: valuation. At the end of 2024, U.S. mega caps were described as trading at a substantial earnings multiple

premium relative to many international peers. Investors have been willing to pay up because they expect faster growth an “AI growth

premium” story and because the largest firms have global reach, massive cash flows, and (sometimes) the vibe of “too important to ignore.”

Stocks Aren’t GDP… But the Gap Still Turns Heads

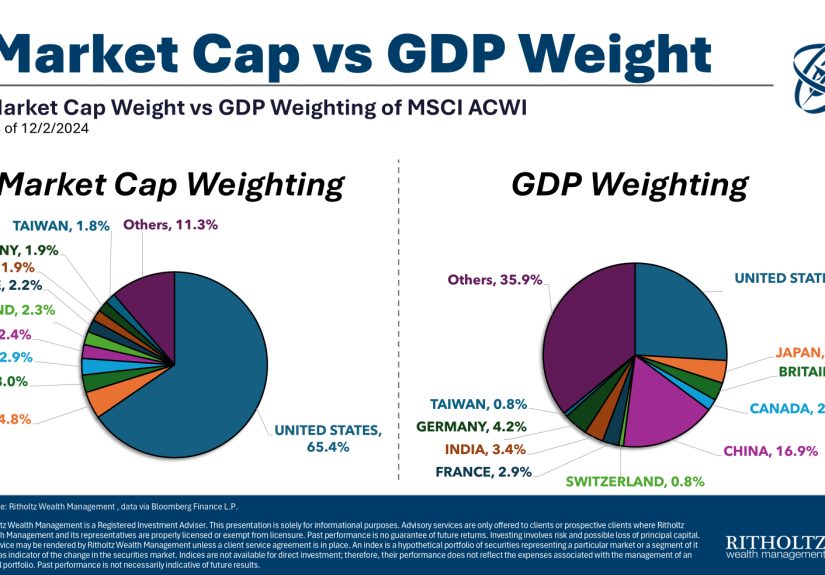

One of the most striking parts of the “U.S. swallowing the world” discussion is the comparison between the U.S. share of global economic

output and the U.S. share of global equity market capitalization in major indexes. They’re not the same thing not even close

because stock markets reflect listed corporate value, profitability, and investor access, not the full size of a nation’s economy.

Still, the contrast is memorable: the U.S. can represent around a quarter-ish of global nominal output by some measures while accounting for

a much larger slice of global equity value in major indexes. Meanwhile, other large economies may show the opposite pattern a big GDP share

but a comparatively smaller footprint in widely used global equity indexes due to differences in market structure, listings, state ownership,

capital controls, sector mix, and investor access.

Why some countries “under-show” in global indexes

- Fewer public mega-caps: Some economies have large private firms or state-owned enterprises that don’t trade like U.S. public companies.

- Bank-heavy markets: Many non-U.S. markets lean more toward financials and industrials, with fewer platform-style tech giants.

- Corporate profitability differences: Higher margins and stronger shareholder orientation can translate into higher valuations over time.

- Investor accessibility: Index weights reflect what global investors can realistically own and trade, not just what exists.

- Currency and capital flow dynamics: In stress periods, money often runs toward dollar assets and U.S. liquidity.

History Check: “Swallowing” Is Not a Straight Line

The most useful antidote to “this time is different” is… time. Global market leadership rotates, sometimes for years, sometimes for decades.

The U.S. has had periods of even higher relative market share in the past, and there have been eras when other regions surged:

Japan’s late-1980s boom, emerging markets’ mid-2000s strength, and the U.S. “lost decade” style slump in the 2000s are classic examples

investors love to cite right after they stop crying into their diversification spreadsheets.

Major index analysis has noted that U.S. outperformance became especially consistent after the 2008 crisis, with U.S. equities beating

international counterparts across rolling multi-year periods through the 2010s and into the 2020s. That’s a long run long enough to make

a generation of investors believe international diversification is a “nice idea” in the same way flossing is a “nice idea.”

But cycles don’t mail you a calendar invite before they turn. The bigger the performance gap gets, the louder the debate becomes:

“Is the U.S. genuinely exceptional?” versus “Are we just paying a premium for yesterday’s winners?”

The Hidden Risks of a U.S.-Heavy World

Dominance feels great on the way up. It feels less great when everyone realizes they’re standing on the same crowded trade.

The risks aren’t theoretical; they’re practical and they show up in portfolios in a few common ways.

1) Concentration risk (a.k.a. “Seven stocks walk into your retirement account”)

If a small number of companies drive a large share of returns, investors become more sensitive to those companies’ earnings,

regulatory environment, competitive threats, and narrative shifts. When market breadth narrows, “the market” can look fine even as many

stocks lag until the leaders stumble and the floor suddenly remembers it exists.

2) Valuation risk (paying up can work… until it doesn’t)

Higher valuations are not automatically bad they can reflect real quality and real growth. But they can also reduce the margin of safety.

If earnings growth disappoints, high-multiple segments can reprice quickly. International markets, by contrast, often trade at lower multiples,

which can offer different return drivers especially if leadership rotates.

3) Policy and geopolitical spillovers

When the U.S. sits at the center of global market narratives, U.S. policy reverberates everywhere from rates and regulation to trade and

tariffs. Major market research has pointed to how trade barriers and policy shifts can reshape corporate revenue exposures across regions,

particularly for export-oriented economies and supply-chain-linked markets.

4) Currency whiplash

Currency can turn “good international returns” into “meh returns” (or vice versa) depending on the dollar’s direction. Investors often ignore

currency until it’s the whole story. Broad dollar indexes exist for a reason: the exchange-rate effect is real, persistent, and emotionally rude.

So… Should You Fight It or Ride It?

Here’s the tricky truth: you don’t need to “bet against America” to acknowledge concentration and valuation risk. You also don’t need to

pretend the U.S. is doomed just to justify owning international stocks. The goal isn’t to win a debate it’s to build a portfolio that can

survive multiple futures, including ones where the U.S. remains dominant and ones where it cools off.

Practical approaches investors actually use

- Use a global core: A broad global fund can keep you diversified while naturally holding a large U.S. weight (because that’s how cap-weighting works).

- Set a policy allocation and rebalance: Decide your U.S./international split ahead of time and rebalance on a schedule not based on vibes.

- Pair cap-weighted with “anti-concentration” tilts: Some investors add equal-weight, value, or small-cap exposure to reduce mega-cap dependence.

- Remember what international diversification is for: It’s risk management and opportunity access, not a yearly performance contest.

- Think in decades, not quarters: The cycles that change leadership often unfold slowly, then suddenly.

Vanguard’s investor education on international investing highlights diversification benefits, exposure to different economic cycles, and

currency effects as reasons investors may choose global diversification. Morningstar commentary has also emphasized that a concentrated U.S.

market can make non-U.S. and smaller-company exposures look more attractive on valuation and diversification grounds even if they’ve been

unpopular lately.

Conclusion: The U.S. Might Be Eating the Buffet, But The World Still Has Dessert

U.S. markets have become the gravitational center of global investing powered by scale, liquidity, entrepreneurship, sector leadership,

and a small group of mega-cap firms that have effectively become global “equity infrastructure.” In index terms, that dominance has reached

historically high levels. And yes, it can feel like the U.S. is “swallowing” everything else.

But market leadership is cyclical, concentration is a double-edged sword, and the rest of the world is not a rounding error it’s a diverse

set of markets with different sectors, valuations, currencies, and catalysts. The most “wealth of common sense” takeaway is simple:

don’t build a portfolio that only works if the last decade repeats forever. Build one that can handle a world where the U.S. stays strong…

and a world where it shares the spotlight.

Investor Experiences: What This U.S.-Dominance Era Feels Like

The weirdest part about “U.S. markets swallowing the rest of the world” isn’t the chart itself it’s how it changes investor behavior in real life.

Numbers may be rational, but portfolios are run by humans, and humans are basically emotions with spreadsheets.

One common experience is the slow drift from “diversified plan” to “accidental America-only.” It often starts innocently: someone chooses a global

fund, or a target-date fund, or a sensible mix of U.S. and international. Then the U.S. outperforms for another year. And another. Over time, without

rebalancing, the U.S. allocation grows like a houseplant that suddenly discovered sunlight. The investor didn’t make an active decision to bet bigger

on the U.S. the market made it for them. When they check allocations later, they’re surprised by how much concentration snuck in while they were busy

living their life.

Another very real experience is “diversification regret.” Picture an investor who diligently held international stocks through the 2010s and early 2020s.

They read the right books, nodded at the right principles, and did the right grown-up things. But every time they compared returns with a friend who held

only U.S. stocks, it felt like showing up to a marathon with a backpack full of rocks. Even if they still believed in diversification, the emotional tax

was constant: “Am I being prudent… or just stubborn?” This is where many people quietly capitulate, selling international after a long stretch of

underperformance which, unfortunately, is exactly how performance chasing tends to work.

There’s also the “Magnificent Seven lifestyle,” which is a fancy way of saying: people start thinking they’re diversified because they own an index,

while the index is increasingly dominated by a few leaders. The experience here is confusing. The investor sees the S&P 500 up, hears headlines about

record highs, and assumes “stocks” are doing great. But their friend who owns a more diversified U.S. portfolio might complain that “most of my stocks

are flat.” Both can be true in a concentrated market. The index can look strong while broad participation is weaker and that disconnect can make

investors second-guess everything.

Advisors and long-term investors often describe another experience: “rebalancing pain” the good kind. Rebalancing forces you to trim what has done

well and add to what has lagged. In a U.S.-dominant era, that can mean regularly selling some U.S. winners to buy international or smaller companies.

Emotionally, it feels like trading a hot new show everyone’s watching for a critically acclaimed foreign film your friends insist you’ll love. But the

whole point is to keep your portfolio from turning into a one-theme playlist.

Finally, many investors experience “headline whiplash.” One week, the story is unstoppable U.S. innovation, AI capex, and soaring productivity.

The next week, it’s valuations, concentration risk, regulation, and geopolitical shocks. The healthiest investors learn to treat narratives like weather:

worth checking, not worth obeying. They set an allocation that reflects reality including the U.S.’s massive global footprint while still protecting

themselves from the possibility that leadership rotates. In practice, that means staying diversified, rebalancing with discipline, and remembering that

the goal is not to perfectly predict which country wins next year. The goal is to stay in the game long enough to benefit from whatever wins next.