Table of Contents >> Show >> Hide

- The Classic Story: Risk and Reward (Mostly) Travel Together

- Why Some Risks Pay Youand Others Don’t

- A Wealth of Common Sense Example: Two Stocks, Two Very Different Outcomes

- Four Common Ways Investors Take Risk Without Getting Paid

- So What Actually Works? A Checklist for Smarter Risk

- When Risk Isn’t Rewarded, What Should You Do Next?

- Conclusion: The Goal Isn’t Less RiskIt’s Better Risk

- Real-World Experiences: What It Feels Like When Risk Doesn’t Pay (Plus What Helps)

Risk is supposed to come with a punchline: reward. That’s the deal we’re sold in money talk, finance class,

and every inspirational poster that says “no pain, no gain” (usually next to a guy flipping tractor tires).

But investing has a brutal sense of humor: sometimes you take the pain, and the “gain” ghosts you.

This ideawhen risk is not rewardedis a core “wealth of common sense” lesson because it separates

smart, intentional risk from the kind that just makes your stomach hurt. The goal isn’t to become allergic to risk.

The goal is to learn which risks have a history of paying investors over time, and which risks are basically

“extra spicy” with no extra flavor.

The Classic Story: Risk and Reward (Mostly) Travel Together

In the big-picture version of investing, the risk-and-reward relationship is real. Stocks usually bounce around more

than bonds. Cash is steadier than both. And over long stretches of history, investors have generally demanded a higher

return to own the thing that can drop 30% when the world gets nervous.

That “extra return” is often described as the equity risk premiumthe idea that stocks are expected

to beat a safer baseline (like Treasury bills or bonds) because stocks are riskier. The key word is

expected. It’s not a guarantee, it’s a reason people are willing to hold stocks in the first place.

Here’s the important part: even if the long-run story holds up, the short-run story can be a mess.

Stocks can lag bonds for years. Entire decades can be disappointing. Some markets go through long

“nothing burgers” where risk feels like it’s charging rent and not paying utilities.

Why Some Risks Pay Youand Others Don’t

A practical way to think about investing risk is to split it into two buckets:

compensated risk and uncompensated risk.

Compensated risk: the risk that tends to come with a payoff

This is the risk you can’t completely diversify away because it’s tied to the market or broad economic conditions.

Think: owning a diversified basket of stocks and living through recessions, bear markets, inflation scares, and the

occasional “is the financial system okay?” headline.

Over long horizons, investors have historically been compensated for bearing broad market riskthough not smoothly,

not consistently, and definitely not on the timeline of “I need this to work by summer.”

Uncompensated risk: the risk that usually doesn’t increase your expected return

This is the risk you take that can often be reduced without giving up expected return. In plain English:

it’s the risk you’re taking for freeand “free” is not a compliment here.

Uncompensated risk shows up when a portfolio is too concentrated, too dependent on one theme, one employer, one sector,

one country, one high-fee product, or one “this time is different” story. It’s the risk of putting your financial

future in a single narrative and hoping the market agrees.

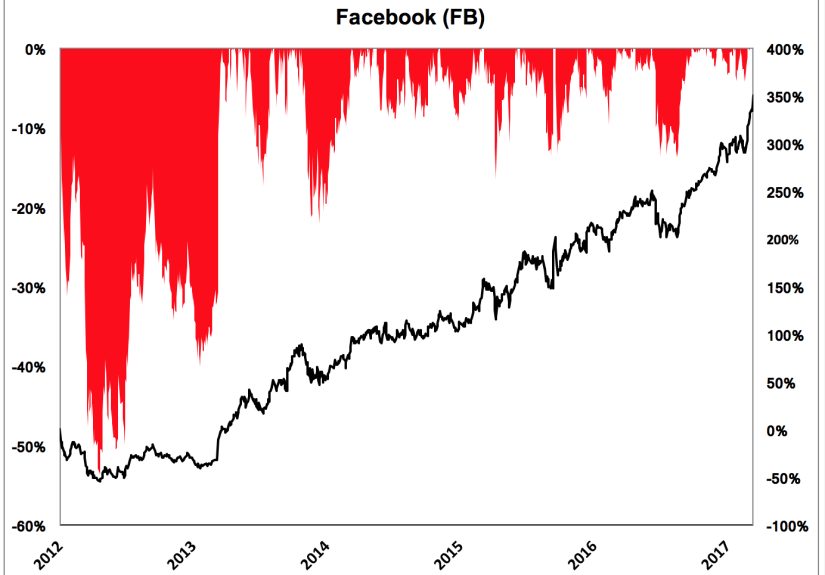

A Wealth of Common Sense Example: Two Stocks, Two Very Different Outcomes

One reason this topic resonates is that individual stocks are where the risk/reward relationship gets weird.

A classic pattern looks like this:

-

Company A is volatile, has brutal drawdowns, and later becomes a historic winner. The pain looks

justified in hindsight because the eventual payoff is enormous. -

Company B is also volatile, also has gut-check drawdowns, but never delivers the upside that would

make the rollercoaster worth it.

The uncomfortable truth is that both companies can feel similar while you’re living through it.

Volatility doesn’t come with a label that says “congratulations, this will be worth it later.”

This is why talking about past winners can be misleading. It’s fun to say, “If you invested $10,000 in the right stock

at the perfect moment…” but that game is basically the financial version of planning how you’ll spend your lottery

winnings. It skips over the part where you had to pick the right winner without the benefit of hindsight,

then hold through terrifying drops, then ignore a thousand reasons to sell, then not get replaced by panic along the way.

Winners are loud. Losers are plentiful. And markets are perfectly capable of punishing risk that looks brave on paper.

Four Common Ways Investors Take Risk Without Getting Paid

1) Overconcentration: “I know this company. I work there.”

Concentration is seductive because it feels like conviction. If a stock has treated you well, it’s easy to believe

you’ve found “your” thing. But concentration can quietly turn your portfolio into a one-act play.

One of the most common versions is holding too much employer stock. It’s not just an investment riskit’s a life risk.

If your employer hits trouble, you could face a double hit: job uncertainty and a portfolio drawdown at the same time.

Diversification is boring, but boring is often the point. The goal isn’t to avoid upside; it’s to avoid betting your

financial security on a single outcome.

2) “Lottery stocks”: exciting volatility, disappointing returns

Some stocks behave like scratch-off tickets: low price, wild swings, and the faint hope of a moonshot.

Humans naturally like the idea of a small chance at a huge payoff. Markets know this. And when enough people pay extra

for “maybe this explodes,” expected returns can get worse, not better.

Research has found that stocks with very high idiosyncratic volatility (company-specific whiplash) can have

lower future returns on average. That’s a fancy way of saying: “being extra chaotic doesn’t automatically mean being extra profitable.”

This isn’t a moral judgment. It’s a pricing reality: if investors overpay for the thrill, the thrill becomes the product,

not the return.

3) Reaching for yield: when “more income” is actually more risk

Whenever safer yields look unattractive, people start stretching. They move into riskier bonds, questionable dividend

plays, or products that promise “income” like it’s a free refill.

The problem is that yield is not a cheat code. Sometimes higher yield is fair compensation for real risks

(credit risk, default risk, liquidity risk). Other times it’s a warning label written in smaller font.

If the market is offering unusually high yield, ask what it’s trying to pay you to endure.

A classic mistake is treating higher yield as “safer” because it pays you monthly. But cash flow doesn’t cancel price risk.

A steady coupon can be a comfort blanketuntil it isn’t.

4) Complexity and illiquidity: paying more to understand less

Complexity often masquerades as sophistication. Some products are genuinely useful in the right portfolio and the right

context. But complexity also creates two sneaky risks:

- Fee drag: higher costs that quietly reduce returns year after year.

- Decision risk: the investor abandons the strategy at the worst possible time because it’s confusing or opaque.

Illiquidity can be compensated sometimes (you might earn a premium for locking money up), but it can also be

uncompensated if the lock-up mainly benefits the structure, not the investor. If you can’t explain the product in plain

language, the product may be explaining you.

So What Actually Works? A Checklist for Smarter Risk

If “risk isn’t always rewarded,” the practical response is not fearit’s process.

Here are common-sense moves that raise the odds that the risk you take is the kind that can pay you back.

Build your portfolio around diversified exposures

A diversified portfolio doesn’t eliminate risk. It trades concentrated risk for broad risk.

That’s a good swap. Broad risk is the kind that has historically been compensated over time.

Decide your asset allocation before the market decides for you

Asset allocation is the “how much in stocks vs bonds vs cash” decision, and it’s one of the biggest drivers of how an

investing experience feels. Too aggressive and you’ll panic-sell. Too conservative and you’ll sabotage long-term growth.

The right mix is the one you can live with.

Rebalance like a grown-up

Rebalancing is the simple, occasionally annoying practice of trimming what’s grown and adding to what’s laggingbased

on your plan, not your mood. It’s a disciplined way to avoid drifting into unintended concentration during long bull runs.

Keep costs low (because fees are guaranteed, returns are not)

You can’t control the market, but you can control what you pay to access it. High fees are one of the few risks

investors take that reliably reduce returns. That’s the most “not rewarded” risk of all.

Make peace with uncertaintyand stop demanding instant validation

Markets don’t hand out gold stars for being early or right “eventually.” They only price what they price. A good plan

requires patience, because the payoff for compensated risk often arrives late, messy, and unannounced.

When Risk Isn’t Rewarded, What Should You Do Next?

This is where common sense beats adrenaline. When something risky doesn’t pay off, you have two choices:

-

Improve the process: Was the risk intentional? Diversified? Reasonable? Connected to a long-term plan?

Or was it a concentrated bet disguised as confidence? - Chase a “make it back” trade: the emotional sequel nobody asked for, and the one that often makes things worse.

The market is full of opportunities to accept outsized risk without receiving outsized returns.

The win is learning to recognize those situations before they recognize you.

Conclusion: The Goal Isn’t Less RiskIt’s Better Risk

“When risk is not rewarded” isn’t a reason to give up on investing. It’s a reminder to stop confusing

volatility with opportunity, and complexity with edge.

The smartest investors are not fearless. They’re selective.

They take risks that have a history of being compensated (like diversified market exposure over time),

and they avoid risks that can be reduced for free (like concentration, unnecessary complexity, and

thrill-seeking in disguise). That’s the wealth-of-common-sense approach: not predicting the future,

but building a plan that doesn’t require perfect predictions to work.

Real-World Experiences: What It Feels Like When Risk Doesn’t Pay (Plus What Helps)

The hardest part about uncompensated risk is that it rarely announces itself. It usually shows up as a story you can

tell yourself with a straight face. Below are realistic “investor experiences” built from common patternsbecause you

don’t need a dramatic headline to learn this lesson; you just need a portfolio and a little time.

Experience #1: The “I Did the Brave Thing” Stock Pick That Never Pays Off

Someone buys a single stock because it feels like a high-conviction move: a hot brand, a compelling product, a charismatic

CEO, or a strong narrative about “the future.” The stock is volatile, which gets interpreted as proof of upside.

Then reality hits: earnings disappoint, competition shows up, or the business model looks less magical under higher

interest rates. The investor holds through drawdowns because selling would “lock in” the loss, and the mind starts

bargaining: “If it just gets back to my cost basis, I’ll sell.”

Months turn into years. The stock may bounce, but it never regains the highs. Meanwhile, the broader market moves on.

The emotional cost becomes bigger than the financial costchecking prices too often, arguing with friends about the company,

and feeling personally judged by a ticker symbol. What helps isn’t a heroic comeback trade. What helps is zooming out:

recognizing that single-stock risk is often uncompensated, and that a diversified approach can keep the investor exposed

to growth without depending on one company’s fairy tale ending.

Experience #2: The “Safe Income” Investment That Wasn’t Actually Safe

Another common experience starts with a reasonable desire: “I want more income.” The investor moves into a higher-yield

productmaybe a riskier bond fund, a high-dividend strategy, or something marketed as stable because it pays regularly.

The payments feel reassuring. Then spreads widen, defaults rise, or rates change, and the price drops more than expected.

The investor realizes they didn’t just buy income; they bought a bundle of risks, including credit risk and liquidity risk.

The lesson isn’t “never seek yield.” It’s “understand what yield is paying you for.” If the yield is higher, something

is riskiersometimes in ways that don’t show up until stress hits the system. What helps here is re-framing the goal:

income is not the same as safety. A better plan is matching the investment to the time horizon, diversifying across

quality, and avoiding the temptation to treat cash flow as a substitute for risk management.

Experience #3: The Portfolio That Looked DiversifiedUntil It Needed to Be

This one is sneaky. On paper, the portfolio has many holdings: multiple funds, multiple accounts, maybe even a mix of

stocks and ETFs. But a closer look shows overlap: the same large companies repeated across different products, heavy

concentration in a single sector, or a strong home-country bias that turns “diversified” into “mostly one bet.”

In calm times, it feels fine. In a downturn, correlations rise and everything seems to fall togetherright when the

investor expected diversification to be the superhero.

The “aha” moment is realizing that diversification isn’t a count of how many tickers you own; it’s a measure of how

different your exposures truly are. What helps is simplifying: using broad, low-cost building blocks, checking overlap,

and making sure the portfolio isn’t accidentally built around one theme. The goal is not perfection; it’s resilience.

When risk isn’t rewarded, resilience is the reward you notice firstbecause it keeps you in the game long enough for

compensated risk to do its job.