Table of Contents >> Show >> Hide

- What Is the Russell 2000, Exactly?

- Why Investors Watch the Russell 2000 So Closely

- What Makes Small-Cap Stocks Different?

- Now for the Underrated Middle Child: Mid Cap Stocks

- Why Mid Cap Stocks Deserve More Appreciation

- The Russell 2000 and Mid Caps: Related, But Not the Same Story

- How Market Cycles Shape the Russell 2000 and Mid Caps

- Specific Examples of Why Mid Caps Are Easy to Overlook

- The Real Takeaway: The Russell 2000 Matters, but It Should Not Hog the Whole Conversation

- Investor Experiences and Practical Lessons From Following the Russell 2000 and Mid Caps

- Conclusion

- SEO Tags

Wall Street loves a headliner. One year it is the mega-cap tech giants hogging the spotlight like they own the red carpet. Another year it is tiny small-cap stocks bursting out of nowhere like the indie band that suddenly headlines a stadium tour. Caught between those two attention hogs is a group of companies that often gets less fanfare than it deserves: mid cap stocks.

If you have ever heard investors talk about the Russell 2000, they are usually talking about the mood ring of small-cap America. It is the index people check when they want to know how smaller U.S. companies are doing. But once you look closely at the Russell 2000, you also start to notice something else: the investment conversation often skips too quickly past mid caps, even though they can offer an appealing blend of growth potential, business maturity, and diversification.

So let’s do two things at once. First, we will take a smart, practical look at what the Russell 2000 actually is and why it matters. Second, we will give mid cap stocks the standing ovation they rarely ask for but often earn.

What Is the Russell 2000, Exactly?

The Russell 2000 is one of the best-known small-cap stock indexes in the United States. In simple terms, it tracks roughly 2,000 smaller publicly traded U.S. companies. It sits inside the broader Russell index family, which is built to represent the investable U.S. stock market.

Think of the Russell universe like a giant class photo. The Russell 3000 is the full group shot, covering about 3,000 U.S. stocks. The Russell 1000 contains the larger companies. The Russell 2000 captures the smaller companies that remain after the biggest names are pulled out. That structure is one reason the Russell 2000 matters so much: it is not just a random basket of small stocks. It is a rules-based slice of a bigger, widely followed system.

Investors, fund managers, financial journalists, and ETF providers use the Russell 2000 as a benchmark for the small-cap segment. When the index is rallying, people often say investors are warming up to risk, domestic growth, and companies with more room to expand. When it struggles, that can reflect tighter financial conditions, slower growth expectations, or a market that prefers the balance-sheet strength of larger firms.

In other words, the Russell 2000 is part thermometer, part scoreboard, and part personality test for the market.

Why Investors Watch the Russell 2000 So Closely

It offers a read on smaller U.S. businesses

Many companies in the Russell 2000 are more domestically focused than giant multinational corporations. That makes the index useful when investors want exposure to the U.S. economy beyond the handful of giant names that dominate headlines. If you want to know how smaller industrial firms, regional service businesses, niche healthcare players, and up-and-coming software companies are doing, the Russell 2000 gives you a better clue than a large-cap benchmark alone.

It behaves differently from large-cap indexes

The S&P 500 and other large-cap indexes can sometimes look like a parade led by a few enormous companies. The Russell 2000, by contrast, tends to be broader and less top-heavy. That can make it more volatile, but it also means performance may be driven by a wider mix of businesses rather than a tiny club of giants.

It reflects the opportunities and headaches of small caps

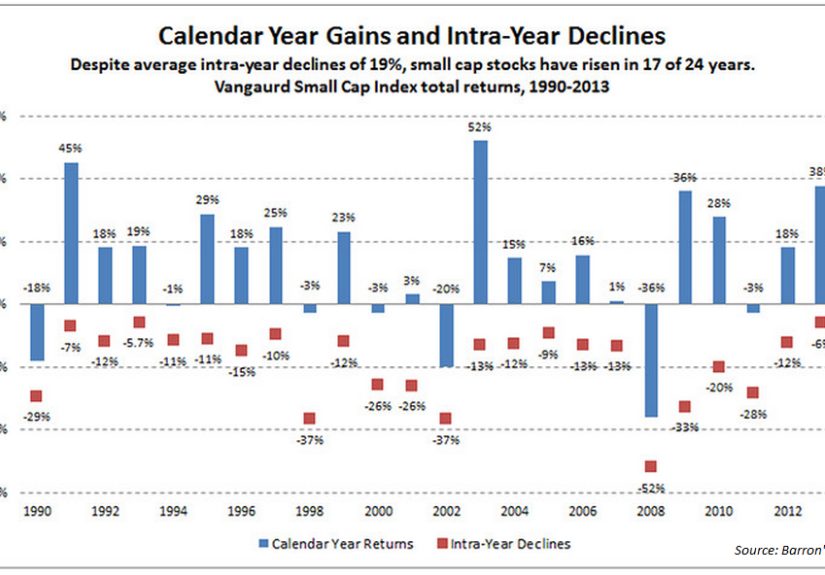

Small-cap companies can grow faster than mature blue chips, but they can also be more sensitive to borrowing costs, economic slowdowns, and investor nerves. That is why the Russell 2000 is often treated as a test of economic confidence. When investors believe the future looks brighter, they may be more willing to buy smaller companies. When fear shows up with a clipboard and a frown, small caps often feel it first.

What Makes Small-Cap Stocks Different?

Before we praise mid caps, it helps to understand why small-cap stocks attract so much attention in the first place.

Small caps are often seen as the market’s “maybe this company becomes a big deal later” category. They may operate in niche industries, serve narrow markets, or still be proving that their business model can scale. Because of that, investors like them for their potential upside. A company that goes from “promising” to “profitable and dominant” can generate enormous shareholder excitement.

But small caps are not magic beans. They usually come with higher business risk, thinner margins, less diversified revenue, and fewer financial cushions than large corporations. A big company may shrug off a rough quarter. A small company may need a very strong coffee and a very understanding lender.

That is the Russell 2000 in a nutshell: exciting, useful, important, and occasionally dramatic.

Now for the Underrated Middle Child: Mid Cap Stocks

Mid cap stocks sit between small caps and large caps. Depending on the definition, that usually means companies with a market value somewhere in the middle of the pack. Some educational sources use a rough market-cap range of about $2 billion to $10 billion, while index providers may define mid caps relative to the broader market rather than a fixed dollar cutoff.

Either way, the big idea is the same. Mid caps are often companies that have moved beyond the scrappy startup phase but still have meaningful room to grow. They may already have recognizable products, expanding national footprints, improving profitability, and more seasoned management teams, yet they are not so huge that growth becomes a slow, lumbering affair.

If small caps are the ambitious younger sibling and large caps are the well-established older one with a mortgage and a Costco membership, mid caps are the capable middle child finally getting things together and quietly becoming the family success story.

Why Mid Cap Stocks Deserve More Appreciation

They can offer a balance of growth and stability

One of the strongest arguments for mid cap investing is that mid caps may capture some of the upside investors like in small caps while avoiding part of the fragility that can come with very small companies. Many mid-cap businesses are already past the most hazardous early-growth stage. They may have steadier revenue, better access to capital, and more operational experience.

That does not make them safe in the absolute sense. Stocks are stocks, and mid caps can still swing around. But they often occupy a sweet spot: established enough to feel real, young enough to keep growing.

They may be less crowded than mega-caps

Large-cap names get endless analyst coverage, nonstop media attention, and enough public commentary to fill a small library. Mid caps often live with less spotlight. For investors, that can be a feature rather than a flaw. A less crowded segment may offer more opportunities for discovery, especially for people who want exposure beyond the same famous companies appearing in every portfolio discussion.

They improve diversification

A portfolio made only of mega-cap stocks can become more concentrated than it first appears. Mid caps help spread exposure across different business sizes, industries, and growth stages. That diversification matters because market leadership changes. The stocks that dominate one cycle may not lead the next.

They can reflect business momentum in action

Mid caps are often where you find companies transitioning from “promising” to “proven.” They may be expanding regionally into national markets, increasing margins, or moving from founder-led hustle into more scalable corporate structure. That phase can be attractive because growth is still present, but the business may already have more substance behind it.

The Russell 2000 and Mid Caps: Related, But Not the Same Story

Here is where the conversation gets more interesting. The Russell 2000 focuses on small caps, but it naturally points investors toward a question: what happens when these smaller companies mature?

Some of them never do. Some stall out. Some disappear. But some graduate into the mid-cap tier, and that journey matters. Mid caps can be the proving ground where a business shows it is more than a hopeful idea in a well-designed investor deck.

Russell’s broader index family includes benchmarks for this part of the market too, such as the Russell Midcap Index and the Russell 2500, which covers the small-to-mid, or “smid-cap,” segment. That is a reminder that the Russell 2000 is only one chapter in the market-cap story. If you focus on it alone, you may understand where smaller companies are today, but miss where some of the best businesses are going tomorrow.

That is why an appreciation for mid caps is so useful. It completes the picture. The Russell 2000 shows the energy of smaller companies. Mid caps show what happens when some of that energy turns into staying power.

How Market Cycles Shape the Russell 2000 and Mid Caps

Small caps and mid caps do not perform the same way in every environment. Interest rates, credit conditions, inflation expectations, and investor risk appetite all matter.

When economic growth looks strong and financing is available, the Russell 2000 can shine because smaller companies may benefit disproportionately from improving sales and rising optimism. But when money gets expensive or the economy looks shaky, small caps can struggle more than larger firms because they often have fewer resources and less flexibility.

Mid caps can sometimes hold up better in those moments. They are not immune to market stress, but many are more mature than typical small-cap firms. They may have stronger balance sheets, broader customer bases, and better access to funding. That can make them more resilient than the average small cap, while still offering more growth potential than a slow-moving giant.

Recent market research has also reinforced an old truth: leadership rotates. Large caps can dominate for years, then smaller or mid-sized companies can come back into favor. That is another reason not to dismiss mid caps just because they are not currently winning the loudest popularity contest on financial television.

Specific Examples of Why Mid Caps Are Easy to Overlook

Imagine three companies. One is a mega-cap household name everyone knows. One is a tiny speculative firm with a catchy story and dramatic price swings. The third is a profitable, expanding business quietly gaining market share in industrial technology, specialty healthcare, or business software.

Guess which one gets the fewest headlines? Usually the third one.

That third company often lives in mid-cap territory. It may not be flashy enough to dominate social media chatter, and it may not be small enough to feel like a lottery ticket. But it can still be a serious business with real growth, improving economics, and room to scale.

That is the core of the mid-cap stock appreciation argument. Mid caps are frequently boring in the best way. They are not always trying to change the world by Tuesday. They are often just building better businesses quarter after quarter, which, inconveniently for drama lovers, can be a very effective long-term strategy.

The Real Takeaway: The Russell 2000 Matters, but It Should Not Hog the Whole Conversation

The Russell 2000 deserves its status as one of the most important small-cap benchmarks in the market. It helps investors track a huge swath of smaller U.S. companies, understand market sentiment, and measure how the small-cap segment is behaving.

But the admiration people have for the Russell 2000 should not come at the expense of ignoring mid caps. In fact, a close look at the Russell 2000 almost naturally leads to a greater respect for them. Small caps tell the story of possibility. Mid caps tell the story of progress.

For investors thinking about diversification, business maturity, and long-term opportunity, mid caps deserve more than a passing glance. They deserve a proper seat at the table, not the folding chair near the kitchen.

And that may be the best way to frame the whole discussion. The Russell 2000 is exciting because it represents the early, energetic side of corporate growth. Mid caps are compelling because they show what can happen when that growth begins to harden into quality, durability, and scale. Put together, they offer a richer view of the American equity market than a large-cap-only lens ever could.

Investor Experiences and Practical Lessons From Following the Russell 2000 and Mid Caps

Anyone who spends time watching the Russell 2000 and comparing it with mid cap stocks usually learns a few lessons the hard way. The first is that smaller-company investing rarely moves in a straight line. On paper, it is easy to say that small caps offer higher growth potential. In real life, that can mean sharp rallies, messy pullbacks, and long stretches where investors wonder whether the market has forgotten an entire segment exists.

A common experience is excitement during the first phase of a small-cap rebound. When investors start rotating out of crowded mega-cap trades, the Russell 2000 can suddenly look like the most interesting room in the market. Financial media starts using words like “broadening,” “reflation,” and “domestic growth story,” and everything feels fresh again. That early phase can be thrilling because the moves are often quick and broad-based.

Then reality arrives wearing work boots. Some small-cap companies keep executing, but others run into ordinary business problems: rising costs, soft demand, financing pressure, or weak margins. That is often the moment investors begin to appreciate mid caps more. Mid-cap companies may not move with quite the same wild energy, but they often feel sturdier. They still participate in economic growth, yet they tend to come with more developed operations and more evidence that management knows what it is doing.

Another practical lesson is that headlines can distort perception. When the market is obsessed with giant technology stocks, investors can forget there are hundreds of mid-sized companies steadily expanding in sectors like specialty manufacturing, logistics, software, medical devices, and consumer services. These businesses may not dominate dinner-table conversation, but they can quietly build impressive records over time.

There is also a psychological lesson here. Many investors are naturally drawn either to the safety of giant companies or the excitement of tiny ones. Mid caps can feel less glamorous because they sit in the middle. But middle ground is not the same thing as mediocrity. In investing, the middle can be exactly where discipline, growth, and resilience meet.

People who study these segments long enough often come away with a more balanced view. The Russell 2000 is valuable because it captures entrepreneurial energy and economic sensitivity. Mid caps are valuable because they often represent businesses that have survived early uncertainty and are learning how to scale. The experience of watching both over time teaches patience, diversification, and humility. It reminds investors that not every great opportunity arrives wrapped in hype. Sometimes the most attractive part of the market is the one quietly doing the hard work while everyone else is staring somewhere else.

Conclusion

A closer look at the Russell 2000 reveals far more than just a list of smaller U.S. stocks. It opens a window into economic optimism, business risk, and the early stages of corporate growth. But it also highlights an important truth: some of the most interesting companies in the market may sit just beyond the small-cap label.

That is where mid cap stocks earn their applause. They can offer scale without stagnation, growth without quite as much fragility, and diversification without the concentration risk that can build in large-cap-heavy portfolios. The Russell 2000 may be the famous benchmark, but mid caps are often the underrated professionals quietly putting up strong numbers while the crowd looks elsewhere.

If you want a fuller understanding of the U.S. stock market, the smartest move is not choosing between small caps and mid caps as if only one deserves attention. It is recognizing that both matter, and that the story of American business growth often begins in the Russell 2000 and becomes more durable in the mid-cap space.