Table of Contents >> Show >> Hide

- Why This Episode Still Matters

- Who Is Jeremy Schwartz and Why People Listen

- Core Theme 1: The Future of ETFs Is About Structure, Not Just Scale

- Core Theme 2: Tax-Deferred Accounts Changed the Investing Landscape

- Core Theme 3: International Investing, Currency Hedging, and PPP

- Core Theme 4: Improving the Classic 60/40 Portfolio

- What the Episode Gets Right About Investor Behavior

- How Advisors and DIY Investors Can Apply the Takeaways

- 500-Word Practical Experience Section: What Investors Often Experience With These Ideas

- Conclusion

If you’ve ever listened to a smart investing conversation and thought, “Okay, I understand the words, but I still need the human version,” this article is for you. The Talk Your Book episode featuring Jeremy Schwartz of WisdomTree is the kind of finance conversation that rewards a second pass. It touches on ETFs, tax-deferred accounts, international investing, currency hedging, portfolio construction, and the never-ending “stocks vs. bonds” debatebasically, the greatest hits album of modern portfolio anxiety.

Jeremy Schwartz brings a research-heavy perspective, but the appeal is that the ideas can still be translated into practical portfolio thinking. In this article, we’ll break down what makes the episode important, why WisdomTree’s framework still matters, and how everyday investors (and advisors) can think more clearly about diversification, risk efficiency, and taxes without turning their brokerage app into a casino.

Why This Episode Still Matters

The Talk Your Book appearance is memorable because it focused on themes that have only become more relevant over time: the growth of ETFs, the rise of tax-advantaged investing, and the search for better portfolio design than a plain-vanilla “set it and forget it” allocation. Even if the episode originally aired years ago, the questions it raised are still current:

- How much of your return is coming from smart structure versus plain market exposure?

- Does currency exposure help or hurt when you invest internationally?

- Can a portfolio be made more efficient without simply piling on risk?

- What does tax location do to long-term compounding?

That last point is sneaky-important. Investors love talking about what to buy, but long-term wealth is often shaped just as much by where assets are held (taxable accounts vs. tax-deferred accounts) and how exposure is packaged (for example, ETFs versus other structures).

Who Is Jeremy Schwartz and Why People Listen

Jeremy Schwartz, CFA, is one of the key investment voices at WisdomTree and has long been associated with the firm’s research-led approach to ETFs, index design, and portfolio strategy. He is known for connecting academic finance ideas with real-world fund constructionespecially around dividends, factor tilts, international equities, and capital-efficient portfolio tools.

In plain English: he’s not just talking about markets from a whiteboard. He’s talking about how ideas get turned into actual investable products. That makes his commentary useful for both advisors and individual investors trying to understand why certain ETFs exist, not just what ticker symbols are trending this week.

Core Theme 1: The Future of ETFs Is About Structure, Not Just Scale

One of the strongest takeaways from the episode is that ETF innovation is not only about launching more funds. It’s about improving portfolio implementation. For many investors, “ETF” still sounds like a synonym for “cheap index tracker,” but that’s only part of the story.

ETF wrappers can be used for:

- Broad market exposure (the basic use case)

- Dividend and quality screens

- International and currency-hedged strategies

- Multi-asset and capital-efficient portfolio overlays

- Tax-aware portfolio management in certain account types

In other words, the ETF market matured from “here’s an index fund you can trade intraday” into “here’s a toolkit for precision portfolio construction.” That shift is exactly the kind of thing Jeremy Schwartz tends to emphasize: investment outcomes improve when the design improves.

Why This Matters for Everyday Investors

Many people think the only decision is “active vs. passive.” But that’s too narrow. A better question is: What exposure am I trying to own, and what structure gives me the cleanest, most efficient way to own it? Sometimes the answer is a plain market ETF. Sometimes it’s a dividend strategy. Sometimes it’s a currency-hedged fund. And sometimes it’s a combination.

The joke version: choosing investments without thinking about structure is like buying a couch based only on color. Looks nice. Might not fit through the door.

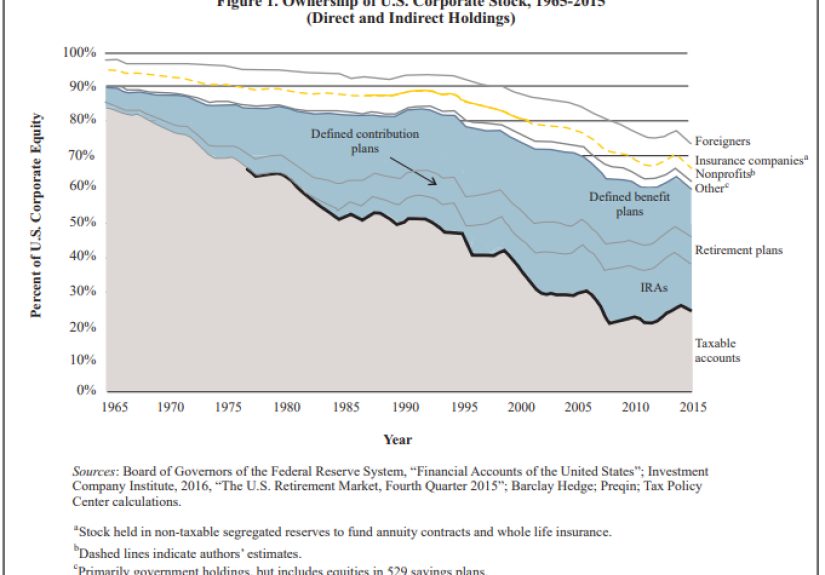

Core Theme 2: Tax-Deferred Accounts Changed the Investing Landscape

A standout discussion point tied to Jeremy Schwartz’s research background is the growing share of assets held in tax-advantaged or tax-deferred vehiclessuch as traditional IRAs, 401(k)s, and other retirement accounts. This matters because when more assets move into tax-advantaged wrappers, market behavior, investor preferences, and portfolio design can shift in subtle ways.

For investors, the practical lesson is simple: account type is part of portfolio strategy. Taxes are not an afterthought. They are part of your expected return.

Practical Implications of Tax Location

- Taxable accounts may favor more tax-efficient strategies and lower turnover.

- Tax-deferred accounts can be better places for certain income-heavy or rebalancing-intensive strategies.

- Asset location decisions can improve after-tax outcomes even when the portfolio holdings stay the same.

This is one of those “boring but powerful” topics. It doesn’t sound exciting at dinner parties, but it can make a meaningful difference over decades of compounding. (Though if your dinner party enjoys discussing asset location strategy, please invite me to the next one.)

Core Theme 3: International Investing, Currency Hedging, and PPP

Another major idea in the episode is international investing and the role of currency. Investors often say they want global diversificationuntil currency volatility shows up and starts throwing elbows.

When you buy international equities, you’re usually taking on two sources of return (and risk):

- The return of the underlying foreign stocks

- The movement of the foreign currency relative to the U.S. dollar

That second piece can help or hurt. If the dollar weakens, U.S.-based investors may see a boost from unhedged foreign exposure. If the dollar strengthens, returns can be reduced. This is where currency-hedged ETFs enter the conversation.

So What Does “PPP” Have to Do with It?

Purchasing power parity (PPP) is often discussed as a long-term framework for thinking about exchange rates. It is not a short-term trading crystal ball. It’s more like a valuation lens: currencies may drift away from “fair value” for long periods, but PPP gives investors a way to think about relative pricing over time.

In practice, Schwartz-style portfolio thinking treats currency not as a random footnote, but as a portfolio decision. If your investment thesis is “I want exposure to Japanese or European equities,” you can ask whether you also want the currency exposureor whether you’d rather isolate the equity return with a hedge.

Neither choice is universally correct. The “right” answer depends on your horizon, risk tolerance, and portfolio role. But asking the question at all is already a sign of a more advanced investor process.

Core Theme 4: Improving the Classic 60/40 Portfolio

The traditional 60/40 portfolio (roughly 60% stocks, 40% bonds) remains one of the most widely used allocation frameworks in investing. Jeremy Schwartz and WisdomTree have spent years exploring how to improve its risk efficiency rather than simply abandoning it.

This is where conversations about capital efficiency and “90/60” style thinking become especially interesting. The idea is not “magic returns.” The idea is to use portfolio construction toolssuch as futures overlaysto seek a more efficient exposure mix for the same dollar of capital, while recognizing that leverage and derivatives introduce real risks and complexity.

What “Capital Efficiency” Means (Without the Jargon Tax)

Capital efficiency is basically this: can you get the exposure you want using less capital tied up in a single sleeve, leaving room for diversification or other strategic uses of cash?

WisdomTree’s “Efficient Core” concept is one example of this thinking. It aims to combine equity exposure with a bond futures overlay so investors can potentially maintain a core equity role while adding fixed income diversification in a capital-efficient format.

This is not a beginner “set it and never learn anything again” product category. It requires understanding:

- How futures overlays work

- How leverage affects returns and drawdowns

- Why correlation and volatility matter as much as expected return

- Why implementation risks are real (liquidity, financing, tracking, behavior)

But as a concept, it reflects a valuable principle for all investors: portfolio construction matters. Risk-adjusted thinking can be more useful than return-chasing.

What the Episode Gets Right About Investor Behavior

One reason this conversation lands well is that it doesn’t treat investors as spreadsheets. Real people have habits, fears, preferences, and blind spots. They overreact to headlines. They anchor on recent returns. They hate complexity until complexity is attached to a hot ticker.

Schwartz’s approachat least as it comes through in these types of interviewstends to focus on durable frameworks:

- Build portfolios intentionally

- Use diversification as a tool, not a slogan

- Think about taxes and account structure

- Be clear on what risk you are taking (equity, duration, currency, factor, leverage)

- Match strategy design to long-term objectives, not short-term excitement

That’s useful advice because it ages well. Markets change. The need for process does not.

How Advisors and DIY Investors Can Apply the Takeaways

For Financial Advisors

- Use the episode’s themes to explain portfolio design in plain language to clients.

- Show how tax location and account type can affect after-tax outcomes.

- Discuss when currency hedging is a strategic choice rather than a market-timing call.

- Evaluate whether capital-efficient strategies fit client sophistication and risk tolerance.

For DIY Investors

- Audit your portfolio by exposure type, not just ticker count.

- Separate “I like this fund” from “I understand what risks this fund adds.”

- Avoid using advanced products before understanding their mechanics and downside behavior.

- Think in decades, not dopamine cycles.

A practical next step is to list each holding and label it by role: core U.S. equity, international equity, duration, income, inflation hedge, tactical sleeve, or “I bought this at 11:47 p.m. after reading one thread” (we’ve all seen portfolios like this).

500-Word Practical Experience Section: What Investors Often Experience With These Ideas

Let’s talk about the real-world side of a conversation like Talk Your Book: Jeremy Schwartz of WisdomTree. Not the elegant chart version. The actual version, where people are balancing careers, families, cash flow, headlines, and a brokerage account that somehow contains three excellent funds and one completely mysterious position.

A common experience is that investors begin with a simple goal“I want to invest for the long term”but quickly discover that the market offers 5,000 ways to turn that sentence into confusion. They start with a broad ETF, feel good, then hear about dividend ETFs, then international diversification, then currency hedging, then factor investing, then tax-loss harvesting, and suddenly they’re building a portfolio like they’re drafting a fantasy football team during a power outage.

This is where Jeremy Schwartz-style discussions can help. They encourage investors to pause and ask: what is the portfolio actually trying to do? In practice, that question can reduce a lot of unnecessary moves. For example, someone holding U.S. large caps, international equities, and bonds may realize they do not need a dozen overlapping funds. They may simply need clearer role definitions, better rebalancing discipline, and smarter placement across taxable and retirement accounts.

Another common experience is emotional whiplash around currency moves. Investors buy international funds for diversification, then get frustrated when strong local-market returns look weaker in U.S. dollars. That frustration often leads to reactive decisions: selling at the wrong time or switching strategies based only on recent currency moves. A more grounded processunderstanding unhedged versus hedged exposure before buyingcan prevent that cycle. The experience improves not because markets become easier, but because expectations become more realistic.

Advisors often see a similar pattern with the 60/40 debate. Clients read headlines declaring the death of balanced portfolios, then a year later read the opposite. The lived experience is not that one allocation is permanently “right.” It is that portfolio design should be matched to goals, spending needs, and behavior. Conversations about capital efficiency or enhanced core exposures can be useful, but only when the investor understands the trade-offs. In the real world, complexity without education tends to create panic at the worst possible moment.

The best experience investors report after applying these ideas is usually not “I found a secret fund.” It is something more durable: they finally understand what they own and why they own it. They can explain their portfolio in a few sentences. They stop chasing every new theme. They rebalance with less drama. They pay more attention to taxes. They judge results over a full cycle, not a noisy month. That may sound less exciting than a hot prediction, but it is exactly the kind of progress that compounds over time.

In short, the real-life lesson from this topic is that good investing feels less like constant action and more like better design. Not flashy. Not viral. Just effective.

Conclusion

Talk Your Book: Jeremy Schwartz of WisdomTree is more than a fund-manager interview. It’s a compact lesson in modern portfolio thinking: ETFs as implementation tools, taxes as part of strategy, currency exposure as a deliberate choice, and portfolio efficiency as an ongoing design challenge.

If you’re an investor, advisor, or finance-curious listener, the biggest takeaway is this: don’t just ask what a fund ownsask what job it performs in a portfolio. That question alone can help you make better decisions, avoid unnecessary overlap, and build a more resilient long-term investment plan.

And if that sounds slightly less thrilling than day-trading rumors on social media… congratulations. You may be doing this correctly.