Table of Contents >> Show >> Hide

- Distress Used to Be a Sale Sign. Now It Is Often Just a Warning Label.

- Why Prices Stay Stubbornly High Even When the Market Feels Troubled

- What This Does to Investors, Borrowers, and the Market’s Mood

- Where Opportunity Actually Shows Up When Nothing Looks Cheap

- The Risks of Mistaking “Not Cheap” for “Safe”

- So, What Happens Next?

- Experience Notes: What It Feels Like to Live Through a Market That Looks Distressed but Refuses to Go on Sale

- Conclusion

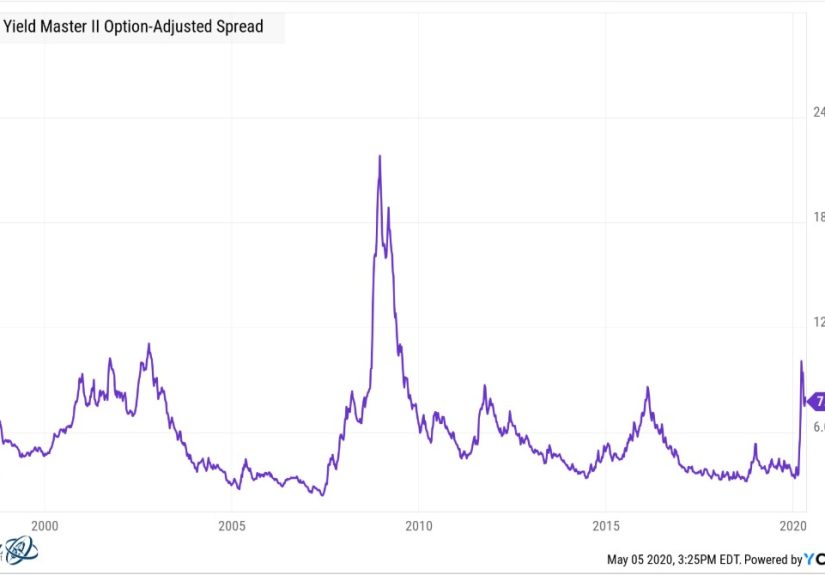

There is a special kind of frustration in finance that deserves its own support group: the moment when a market feels stressed, headlines sound gloomy, refinancing gets awkward, defaults start clearing their throats, and yet prices refuse to go on clearance. In theory, a distressed market should hand opportunistic buyers a shopping cart and say, “Go wild.” In practice, modern credit markets often smile politely and reply, “Best I can do is a tiny discount and a very long due-diligence memo.”

That gap between distress and distressed pricing is one of the defining quirks of today’s market. It matters in private credit, leveraged loans, commercial real estate, sponsor-backed middle-market deals, and even in public credit where spreads can tighten while the underlying business picture still looks like it missed a few nights of sleep. The result is a market that can feel sick without looking cheap.

So what happens when distressed markets do not give you distressed prices? A few things happen at once. Buyers get more selective. Sellers cling to old marks like family heirlooms. Refinancing becomes a bridge instead of a cure. Weak companies survive longer than expected. And the easy-money fantasy of buying dollar bills for sixty cents gets replaced by a much less glamorous sport: arguing over documentation, liquidity, covenants, and whether a “stable” valuation is genuinely stable or just emotionally attached to yesterday.

Distress Used to Be a Sale Sign. Now It Is Often Just a Warning Label.

In older market scripts, distress and cheap prices tended to arrive together. If financing dried up, risk premiums expanded, lenders pulled back, and forced sellers appeared, prices fell hard enough to lure in fresh capital. That was the rough but functional mechanism of market cleansing. Ugly, yes. Efficient, also yes.

Today the script is messier. Markets can be under real pressure without producing the broad, juicy markdowns that distressed investors fantasize about over coffee and spreadsheets. Why? Because there is still a remarkable amount of capital in the system. Private credit funds, interval funds, insurance capital, secondaries capital, large asset managers, and flexible lenders are all circling the same opportunity set. If too much money is chasing “special situations,” those situations start looking suspiciously unspecial.

That changes the meaning of distress. Instead of a fast, dramatic repricing, you often get a slow-motion struggle. A company misses growth targets. Margins compress. Interest expense bites. Sponsors inject support selectively. Lenders tweak documents. Maturities get pushed. Liability management exercises pop up. Everyone agrees the borrower is not exactly thriving, but nobody wants to be the first to crystallize a painful loss. So the asset keeps trading, refinancing, or being marked at levels that imply a calmer world than the operating business actually inhabits.

In plain English: the patient is coughing, but the hospital bill still looks premium.

Why Prices Stay Stubbornly High Even When the Market Feels Troubled

1. There is too much capital hunting the same “distress.”

When institutions keep allocating to private markets, distressed pricing becomes harder to find in broad daylight. Capital that once might have waited for panic now steps in earlier. That support can be rational: investors still want income, floating-rate exposure, senior-secured positions, or access to private structures that offer negotiated protections. But the side effect is that higher-quality stressed assets get bid up before they ever become truly cheap.

This is why markets can feel uneasy while spreads remain tight for better credits. Buyers with scale and patience still want exposure. They may believe they are being prudent, but when many prudent people show up to the same auction, prices get rather impolite.

2. Private marks move more slowly than public prices.

Public markets are brutally honest, sometimes to the point of drama. Private markets, by contrast, are more like that one friend who says, “I’m fine,” while sitting in a room full of smoke. Valuations in private credit and private equity do not update tick by tick, which means deterioration can show up late. That does not automatically mean the marks are wrong, but it does mean public and private signals can diverge for longer than many investors expect.

That divergence creates two illusions at the same time. Public markets may look too pessimistic in the short term. Private markets may look too calm. Reality usually arrives later, wearing steel-toed boots.

3. Refinancing windows reopen before the pain fully clears.

One of the reasons distressed pricing does not always appear is that companies often get just enough access to new financing to avoid a hard reset. Even if borrowing costs remain high by pre-2022 standards, a partial easing in rates, improving market tone, or a receptive private-credit lender can buy time. Time is valuable. Time is also dangerous. It can help good businesses survive a rough patch, but it can also keep weak businesses shambling forward like corporate zombies in business-casual attire.

When refinancing is available, even selectively, assets do not always have to clear at ugly prices. That is good news for holders who hate losses. It is less exciting for buyers who were hoping the market would finally stop pretending everything was okay.

4. Documentation, structure, and sponsor behavior matter more than headline spreads.

When price is not doing the heavy lifting, structure becomes the whole show. A loan with better covenants, tighter collateral packages, stronger reporting, and a lender group willing to act can be far more attractive than a slightly cheaper loan with weak protections and a vague prayer where enforcement should be. In crowded markets, investors often stop competing only on price and start competing on flexibility. That is useful for borrowers, but it can reduce downside protection for lenders if discipline slips.

This is why “tight spreads” alone do not tell you enough. A market can be expensive not only because prices are high, but also because protections are thin. Paying up for risk is one problem. Paying up while giving away your leverage is a sequel nobody asked for.

What This Does to Investors, Borrowers, and the Market’s Mood

Buyers get pickier and more creative.

When broad distressed pricing never appears, serious investors shift from macro shopping to micro hunting. They stop waiting for the whole market to get cheap and start looking for pockets of forced complexity: misunderstood sectors, rescue financings, structured capital solutions, secondary LP sales, asset-based finance, hard-asset-backed loans, and credits where documentation can create value even when the headline yield looks ordinary.

In other words, the game moves from “buy the panic” to “underwrite the mess.” That requires more work, more sector expertise, and a stronger stomach for ambiguity. The easy trade disappears. The smart trade becomes annoyingly specific.

Borrowers survive longer, but not always better.

If distressed pricing does not show up quickly, weak borrowers can avoid a full reckoning. That sounds comforting, and sometimes it is. A company with a decent business but bad timing may only need maturity runway and breathing room. Yet extended survival is not the same as restored health. Businesses that should deleverage may merely refinance. Companies that need an operational fix may get a capital-structure bandage instead. This stretches the cycle out and can make future losses more uneven.

That is one reason modern credit cycles often feel less like a crash and more like a stubborn leak. The floor does not collapse everywhere. It just keeps getting damp.

Sellers hesitate, which reduces true price discovery.

Sellers do not love turning paper pain into real pain. Shocking, I know. When marks feel debatable, exits slow. Transaction volume can stall. Sponsors hold assets longer. Lenders negotiate. Fund managers defend valuations. Everybody waits for either fundamentals to improve or a more generous buyer to appear. The result is fewer clean transactions at market-clearing levels.

And when there is less price discovery, there is more storytelling. Some of that storytelling is thoughtful. Some of it deserves a violin soundtrack and a legal disclaimer.

Where Opportunity Actually Shows Up When Nothing Looks Cheap

1. In the spread between public fear and private patience

Sometimes public markets overreact first, while private markets hold marks steady. Other times private valuations lag and public prices are the better warning signal. Investors with access to both worlds can compare funding costs, liquidity, recoveries, and structure rather than treating public and private credit like rival religions. Relative value becomes more useful than broad market timing.

2. In sectors with real stress, not just fashionable stress

Not every troubled sector is mispriced, but some are more genuinely dislocated than others. Software, telecom, cable, lower-quality consumer exposures, and parts of commercial real estate have all had moments where the fundamental pain ran deeper than the headline market move. In those cases, opportunity is less about buying “the distressed market” and more about identifying which exact business has survivable leverage, durable cash flow, and collateral that still means something when the room gets quiet.

3. In rescue capital and special situations

When broad distress is elusive, bespoke rescue financing can become the grown-up version of bargain hunting. A lender may not buy a loan at a heroic discount, but it may negotiate tighter terms, fees, enhanced collateral, equity kickers, board rights, or priority positioning in a recapitalization. That is not as cinematic as scooping up a fallen angel at half price, but it can be more reliable.

4. In liquidity itself

Liquidity is not just a feature; it is sometimes the opportunity. When many investors are trapped in slow-moving vehicles or reluctant to transact, the party willing to provide flexible, fast capital can earn premium economics without needing a full-blown market collapse. In a world short on honest price cuts, speed and certainty can become the discount.

The Risks of Mistaking “Not Cheap” for “Safe”

This is where people get in trouble. A market that does not reprice dramatically can look healthier than it is. Tight spreads can be read as confidence when they may simply reflect competition. Stable marks can look like resilience when they may partly reflect lag. Low visible default rates can feel reassuring even if underlying stress is building through amendments, payment tweaks, sponsor support, covenant flexibility, or distressed exchanges.

That matters because recoveries are shaped long before a default is officially called. If underwriting weakens during the good mood, losses can surprise later even when the entry price seemed only mildly aggressive. In that sense, the absence of distressed pricing can plant the seeds for future disappointment. Investors do not lose money only by buying obvious garbage. They also lose money by paying polished prices for risks that have not finished revealing themselves.

The modern lesson is simple: when markets are stressed but prices stay rich, you cannot outsource your caution to market quotes. You have to build it yourself through underwriting, documentation, liquidity planning, and honesty about what a “good” yield really compensates you for.

So, What Happens Next?

Usually one of three things. First, fundamentals improve and today’s stubborn pricing eventually looks justified. Second, prices finally catch down to reality, just later and less gracefully than buyers hoped. Third, dispersion widens: stronger assets hold up, weaker ones crack, and the market stops pretending all credits deserve the same benefit of the doubt.

That third outcome is the most likely in many modern credit cycles. Not every corner of the market will implode. Not every stressed borrower will survive. The big broad sale may never arrive. Instead, the market becomes a sorting machine. Good businesses with sensible leverage get refinanced. Fragile companies with weak protections face harsher restructurings. Asset managers with scale, sourcing, and patience find opportunities. Tourists discover that “private” is not a synonym for “immune.”

So when distressed markets do not give you distressed prices, the answer is not “nothing happens.” Plenty happens. The pain gets delayed, redistributed, disguised, and negotiated. The bargains get narrower. The analysis gets harder. The winners are less likely to be the people waiting for fireworks and more likely to be the ones reading the footnotes while everybody else keeps refreshing the headline spread chart.

Welcome to modern distress: less apocalypse, more paperwork.

Experience Notes: What It Feels Like to Live Through a Market That Looks Distressed but Refuses to Go on Sale

If you spend enough time around stressed credit markets, you start to notice a strange emotional pattern. The first phase is excitement. People say things like, “This is it,” or, “Now we’ll finally get paid for taking risk.” They expect widening spreads, forced selling, ugly refinancing headlines, and the magical reappearance of genuine bargains. It feels like standing outside a store before a huge sale, except the store is the global credit market and everyone is dressed like they own at least one spreadsheet with color-coded tabs.

Then the doors open, and the sale never really happens.

Instead, you get half-signals. Borrowers are clearly under pressure, but lenders are still showing up. Management teams talk about discipline while quietly renegotiating terms. Investors complain that valuations are unrealistic, then pass on selling because the bid is “not reflective of intrinsic value,” which is finance-speak for, “I would rather wait and hope the universe becomes more cooperative.”

The experience can be maddening because the market feels wrong in two directions at once. Public prices may look jumpy and dramatic, while private marks look serene to the point of comedy. One side is shouting. The other is meditating. Somewhere in the middle is the truth, drinking lukewarm coffee.

What I find most memorable about these periods is how much the conversation changes. In a true panic, people talk about price. In a not-quite-panic, they talk about process. Suddenly every discussion is about structure, downside control, amendment rights, sponsor incentives, reporting quality, collateral leakage, and whether a refinancing actually solves anything or just moves the problem to a later calendar invite. The glamour drains out of the room fast. What is left is craft.

There is also a psychological tax. When markets refuse to clear, patience starts to feel indistinguishable from denial. Holders convince themselves that stability proves quality. Buyers convince themselves that waiting longer will produce better entry points. Sometimes both are wrong. Sometimes the market is not cheap because the best assets truly deserve a premium. Other times it is not cheap because nobody wants to blink first.

The most seasoned people in these markets are usually less theatrical about it. They do not chase every scary headline, and they do not assume a calm valuation means hidden strength. They ask less glamorous questions. Who controls the documents? Who really has liquidity? Which lenders can hold through turbulence, and which ones may become accidental sellers? Which companies have operational problems, not just capital-structure problems? That mindset tends to be more useful than waiting around for a giant neon sign flashing “DISTRESSNOW 40% OFF.”

The real experience of these markets is not one dramatic collapse. It is a long stretch of negotiated discomfort. Deals still happen. Capital still moves. Returns can still be made. But conviction has to be earned the hard way. You do not get rewarded simply for showing up when the mood darkens. You get rewarded for knowing exactly why an asset can survive, exactly where your protection comes from, and exactly how wrong a consensus view can stay before reality finally sends the bill.

That is the unromantic truth of distressed markets without distressed prices: the opportunity is still there, but it has stopped posing for pictures.

Conclusion

When distressed markets fail to produce distressed prices, the story is not that risk disappeared. The story is that risk changed costume. It moved from obvious markdowns to hidden fragilities, from broad panic to selective pressure, from marketwide bargains to deal-by-deal judgment. For investors, lenders, and operators, that means discipline matters more than drama. The opportunity is no longer in waiting for the whole market to get cheap. It is in recognizing which assets are merely expensive, which are deceptively calm, and which have the structure and staying power to justify their price. In markets like these, the loudest signal is often not the best one. The most important signal is whether the cash flow, the collateral, and the contract still work when sentiment stops doing the heavy lifting.