Table of Contents >> Show >> Hide

- What a Sole Proprietorship Really Is (and Why It’s So Popular)

- Is a Sole Proprietorship the Right Fit for You?

- Step-by-Step: How to Start a Sole Proprietorship

- Taxes: The Part Everyone Avoids Until It Becomes “Suddenly Important”

- Liability: The Big “Grown-Up” Issue (Even If You Feel 22 Forever)

- Licenses, Permits, and Sales Tax: The “Local Rules” Layer

- Brand Protection: DBA vs. Trademark (Not the Same Thing)

- Hiring Help: Contractors, Employees, and the “Uh-Oh, I Need Systems” Moment

- Common Mistakes (and How to Avoid Them)

- When to Consider Switching to an LLC (or Another Structure)

- A Quick Note on Beneficial Ownership Reporting (BOI) and Why Sole Proprietors Still Ask About It

- Real-World First-Year Experiences: What New Sole Proprietors Wish They Knew (500+ Words)

- Experience #1: “I made money… so why do I feel broke?”

- Experience #2: The invoice that ages like milk

- Experience #3: The receipt avalanche

- Experience #4: The awkward business name moment

- Experience #5: The “I’m doing everything” burnout spiral

- Experience #6: The “Do I need to become an LLC now?” question

- Conclusion

Starting a sole proprietorship is the business equivalent of showing up to a party wearing jeans: easy, comfortable, and you can leave whenever you want.

It’s also the most “default” way to run a business in the U.S.if you start selling cookies, coding websites, walking dogs, or offering consulting under your own name without forming an LLC or corporation, congratulations: you’re basically already a sole proprietor.

But “simple” doesn’t mean “no rules.” A sole proprietorship can be fast to launch, yet it still comes with legal, tax, and money-management choices that will

either keep your life tidyor turn your receipts into a confetti cannon come tax time.

This guide walks you through what matters most, what to do first, and what pitfalls to avoid, with practical examples you can actually use.

What a Sole Proprietorship Really Is (and Why It’s So Popular)

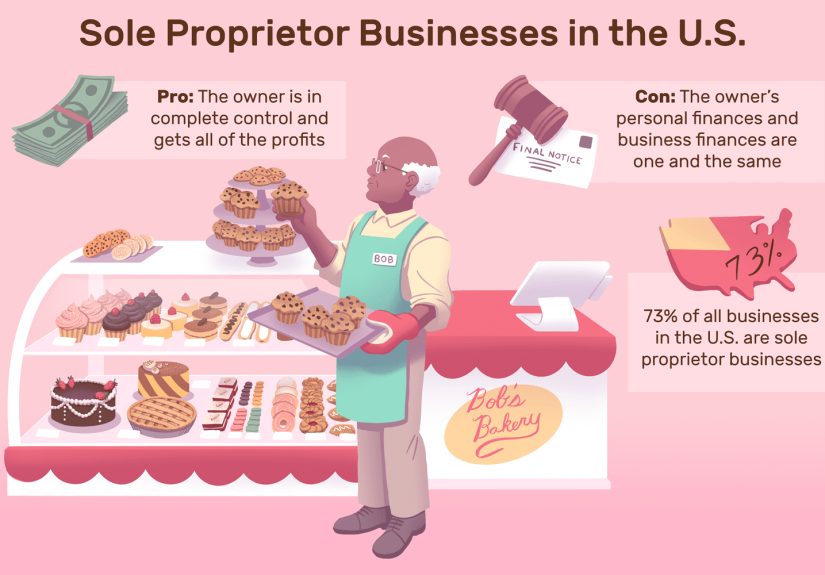

A sole proprietorship is a business owned and operated by one person, with no separate legal entity created. That’s the big headline:

you and the business are the same legal “person.” You get full control, you keep the profits, and you can start quickly.

The tradeoff is that your personal assets can be on the hook if the business gets sued or can’t pay its bills.

Quick reality check: “Separate business” is mostly a money habit here

Even though the law doesn’t separate you from your business, you should separate the money and records anyway.

Your future self will thank you. Your accountant will also thank you. Your accountant’s accountant might even send a thank-you card.

Is a Sole Proprietorship the Right Fit for You?

A sole proprietorship is often a great fit if you’re:

- Testing a business idea (low cost, fast start)

- Freelancing or doing gig work (design, writing, tutoring, delivery, consulting)

- Running a small service business (house cleaning, landscaping, photography)

- Keeping risk relatively low (no employees yet, limited contracts, not a high-liability industry)

It may be a poor fit if you’re:

- Working in a higher-liability field (construction, certain health/fitness services, products with safety risk)

- Signing big contracts or taking on business debt

- Hiring employees soon

- Trying to raise outside investment (sole props don’t sell stock)

A simple example

If you’re a freelance graphic designer doing project work for local businesses, a sole proprietorship can be plenty.

If you’re launching a children’s toy brand and shipping products nationwide, you’ll want to think harder about liability protection and whether an LLC makes more sense.

Step-by-Step: How to Start a Sole Proprietorship

1) Pick your business name (and decide if you need a DBA)

If you operate under your legal name (for example, “Jordan Lee”), you may not need to register a special name.

If you want to operate as “Brightside Bookkeeping” instead, you’ll likely need a DBA (Doing Business As), also called a trade name, assumed name, or fictitious name depending on your state/county.

Important: a DBA usually doesn’t create legal protection for the name by itselfit’s mainly about public notice and letting you do business under a brand name.

If you want stronger name protection, you’ll look at trademarks (more on that below).

2) Check local, state, and federal registration requirements

One of the most confusing parts is that “sole proprietorship” doesn’t require a universal federal registration, but your city, county, or state might still require:

- A general business license

- A home occupation permit (if you run it from home)

- Professional licensing (depending on what you do)

- A seller’s permit/sales tax registration (if you sell taxable goods)

Think of it like owning a car: the car can exist without paperwork, but you still need the right registration and license plates to drive legally where you live.

3) Decide whether to get an EIN (even if you can use your SSN)

Many sole proprietors can use their Social Security Number for tax purposes, but getting an EIN (Employer Identification Number) can still be helpful.

You may need an EIN if you hire employees or meet certain IRS conditions. Even when it’s optional, it can:

- Reduce how often you share your SSN on forms

- Make it easier to open a business bank account (some banks prefer it)

- Help with payroll setup, certain vendor forms, and business credit

Pro tip: applying for an EIN through the IRS is free. If a website tries to charge you for an EIN, it’s basically charging you for clicking buttons you can click yourself.

4) Open a separate business bank account (and a “tax bucket”)

Even though a sole proprietorship isn’t legally separate from you, mixing funds is how small business finances become a mystery novel.

A clean setup is:

- Business checking for business income and expenses

- Business savings (or a second checking account) as your “tax bucket”

Many new sole proprietors set aside a percentage of each payment into the tax bucket (the exact percent depends on income, deductions, and state taxes).

The point isn’t perfectionit’s avoiding the moment in April when you say, “Wait… I was supposed to pay how much?”

5) Set up basic bookkeeping from day one

You don’t need fancy software on day one, but you do need a system. Your bookkeeping should clearly track:

- Income (by date and source)

- Expenses (categorized)

- Receipts and invoices

- Mileage (if you use a vehicle for business)

If you’re allergic to spreadsheets, accounting apps can help. If you love spreadsheets, I won’t stop you. Just promise you’ll label your tabs.

Taxes: The Part Everyone Avoids Until It Becomes “Suddenly Important”

Sole proprietors generally report business income and expenses on Schedule C, and if you have enough net earnings from self-employment, you’ll calculate self-employment tax on Schedule SE.

In plain English: you’re not just paying income taxyou’re also covering Social Security and Medicare contributions that an employer would normally split with you.

Estimated quarterly taxes

If you’re self-employed, you generally need to pay estimated taxes during the year (often quarterly). This helps you avoid penalties and a giant year-end bill.

The IRS provides a worksheet system (Form 1040-ES) to help estimate what you owe.

What counts as a deductible business expense?

A deductible business expense is typically one that’s ordinary and necessary for your trade or business. Common categories include:

- Advertising and marketing

- Supplies and materials

- Software subscriptions

- Business insurance

- Professional fees (legal, accounting)

- Business travel and some meal expenses (rules apply)

- Home office (only if you meet the requirements)

Home office deduction: powerful, but picky

The home office deduction can be valuable, but it generally requires that you use the space regularly and exclusively for business.

“My laptop sometimes sits on the kitchen table” is not the vibe the rule is aiming for.

A practical tax example

Let’s say you’re a sole proprietor photographer. You earn $60,000 in revenue. You spend $12,000 on legitimate business expenses

(equipment depreciation, editing software, insurance, marketing, mileage, and a portion of phone/internet used for business).

Your Schedule C net profit would be about $48,000. That profit flows to your personal return, and you’ll likely owe income tax plus self-employment tax on that net profit.

Liability: The Big “Grown-Up” Issue (Even If You Feel 22 Forever)

Because there’s no separate legal entity, your personal assets can be exposed to business liabilities.

That doesn’t mean you should panic. It means you should be intentional.

Risk-reduction moves that actually help

- Use contracts that define scope, payment terms, and responsibilities

- Get the right insurance (general liability, professional liability, etc.)

- Keep clean records (it helps with taxes and disputes)

- Avoid personal guarantees where possible

Insurance basics for sole proprietors

Insurance isn’t glamorous, but it can be cheaper than one bad day. Common types include:

- General liability (injury or property damage claims)

- Professional liability (errors/omissions for service providers)

- Commercial auto (if you drive for business)

- Workers’ comp (if you hire employeesrules vary by state)

Licenses, Permits, and Sales Tax: The “Local Rules” Layer

Sole proprietorships often trip up here because requirements can be very local.

A few common scenarios:

- You sell physical products: you may need sales tax registration and to collect/remit sales tax where required.

- You operate from home: zoning or a home occupation permit may apply.

- You offer regulated services: a state license may be required.

Example: Etsy seller vs. local service provider

An Etsy candle seller might need sales tax compliance and product labeling awareness.

A mobile dog groomer might need a city business license and commercial auto coverage, plus clear service terms to reduce disputes.

Brand Protection: DBA vs. Trademark (Not the Same Thing)

A DBA lets you operate under a business name. A trademark helps protect a brand name or logo used in commerce.

If you’re building a brand you plan to grow, it’s worth understanding trademarks earlyespecially before you invest in a big website, packaging, or marketing campaign.

A simple brand protection checklist

- Search for similar business names in your state

- Check domain availability

- Do a basic trademark search before committing hard to a name

- Use consistent branding once you choose it

Hiring Help: Contractors, Employees, and the “Uh-Oh, I Need Systems” Moment

Many sole proprietors start solo, then add help as demand grows. The moment you pay someone else, you’ll want to be clear whether they are:

- An independent contractor (you hire them for a project or ongoing work, but they run their own business)

- An employee (you control how/when they work; payroll and labor law rules apply)

Misclassifying workers can create tax and legal issues, so it’s worth doing this part carefully, especially if you’re scaling.

Common Mistakes (and How to Avoid Them)

Mistake #1: Mixing personal and business expenses

Fix: separate accounts, separate cards, and a bookkeeping habit you can keep up.

Mistake #2: Ignoring estimated taxes

Fix: set aside money regularly and review your numbers quarterly. If your income jumps, your tax plan should jump with it.

Mistake #3: Getting “creative” with deductions

Fix: claim legitimate expenses you can support. Keep receipts and logs. Big, unusual deductions can draw extra scrutiny.

Mistake #4: No written agreements

Fix: use contractsespecially for custom work, deposits, deadlines, and scope changes. A good contract is like a seatbelt: it’s annoying until it saves you.

Mistake #5: Skipping insurance in higher-risk work

Fix: match your insurance to your real risk. If a mistake could cost thousands, insurance isn’t optionalit’s strategy.

When to Consider Switching to an LLC (or Another Structure)

Many businesses begin as sole proprietorships and later switch to an LLC when the stakes get higher.

You might consider changing your business structure if:

- Your revenue grows and you want stronger liability separation

- You’re signing larger contracts or taking on debt

- You’re hiring employees

- You want to bring on a co-owner (which may mean partnership or LLC)

- You want a structure that’s more attractive to lenders or investors

This isn’t about “graduating” from a sole proprietorship. It’s about choosing the right tool for the risk and growth stage you’re in.

A Quick Note on Beneficial Ownership Reporting (BOI) and Why Sole Proprietors Still Ask About It

If you’ve heard buzz about Beneficial Ownership Information (BOI) reporting under the Corporate Transparency Act, you’re not alone.

Here’s the practical takeaway: a plain-vanilla sole proprietorship isn’t a separate entity like an LLC or corporation.

Also, federal rules around BOI reporting have shifted in recent updates, including exemptions related to domestic entities.

If you form an LLC or corporation later, check the current BOI requirements at that time.

Real-World First-Year Experiences: What New Sole Proprietors Wish They Knew (500+ Words)

The first year of a sole proprietorship often feels like learning to ride a bike while carrying groceries and answering email.

The good news is that most “pain points” are predictableand once you expect them, they’re easier to handle.

Below are common real-world experiences new sole proprietors run into, plus the practical lesson each one teaches.

Experience #1: “I made money… so why do I feel broke?”

Many first-timers confuse revenue with spendable income. The money hits your account and feels like a win,

but then expenses, taxes, software subscriptions, supplies, and slow-paying clients quietly eat it.

The lesson: adopt a simple cash-flow routine. Every time you get paid, immediately move a portion into your tax bucket,

and keep a running list of monthly “must-pay” expenses. You don’t need a finance degreejust a consistent habit.

Experience #2: The invoice that ages like milk

At some point, a client will pay late. Or “forget.” Or disappear into the mystical land of “Accounts Payable is processing it.”

The lesson: use clear payment terms and a repeatable follow-up system. Include due dates on invoices,

spell out late fees if you plan to enforce them, and consider requesting deposits for custom work.

A surprising number of payment problems are solved by being politely consistent and having everything in writing.

Experience #3: The receipt avalanche

New sole proprietors often start with “I’ll remember this expense” and end with “Why do I have 83 photos of crumpled receipts?”

The lesson: decide on a receipt workflow early. It can be as simple as one folder in your email and one envelope in a drawer,

plus a monthly 30-minute “paperwork reset.” Recordkeeping doesn’t have to be fancy. It just has to exist.

Experience #4: The awkward business name moment

People commonly launch under a name without checking whether it’s already used locally or online.

Later, they discover a near-identical business name in the same industry, or a domain that costs more than their first month of profit.

The lesson: do basic name checks before printing 500 business cards. If you’re building a real brand, learn the difference between a DBA and a trademark early.

Even if you’re not ready to register a trademark, you’ll make smarter naming decisions if you understand how brand protection works.

Experience #5: The “I’m doing everything” burnout spiral

Sole proprietors often become the CEO, the service provider, the marketer, the bookkeeper, and the IT departmentsometimes all before lunch.

The lesson: create a weekly operating rhythm. For example:

one block for client work, one block for marketing, one block for bookkeeping, and one block for planning.

When you give every job a time slot, your brain stops trying to juggle everything at once.

It also becomes obvious which tasks you should eventually outsource (bookkeeping and admin are common early wins).

Experience #6: The “Do I need to become an LLC now?” question

This comes up when your first big contract landsor when someone asks, “Are you insured?”

The lesson: don’t switch structures out of fear or internet hype. Switch because your risk and growth justify it.

If you’re taking on debt, hiring, expanding into higher-liability work, or your income is rising fast,

it might be time to explore an LLC and get professional guidance on the tax and legal impacts.

But many successful businesses remain sole proprietorships for years because it fits their reality.

Bottom line: a sole proprietorship is simple to start, but it rewards structure.

If you build a few basic systems earlyseparate accounts, clean records, clear payment terms, and a tax routineyou’ll feel less stressed,

make better decisions, and free up your energy for the part that actually makes money: serving customers.

Conclusion

Starting a sole proprietorship is one of the fastest ways to turn a skill into a business.

You get flexibility, full control, and minimal startup frictionbut you also take on personal liability and the responsibility to manage taxes and records.

If you treat the business like a business (separate money, track everything, plan for taxes, use contracts, and manage risk),

you can keep the simplicity without the chaos.