Table of Contents >> Show >> Hide

- Wealth inequality vs. income inequality (and why wealth is the big boss)

- The uncomfortable truth: inequality is a team sport

- 1) We clap for “the economy” when we really mean “asset prices”

- 2) We support tax rules that favor wealthbecause “maybe someday”

- 3) We treat housing like an investment firstand a home second

- 4) We normalize “shareholder-first” business behavior

- 5) We shrug at bargaining powerand then act shocked at wage stagnation

- 6) We run the “meritocracy treadmill” that advantages people with cushions

- 7) We accept debt as the default bridge to the middle class

- 8) We treat inheritance as “private,” even though it shapes public outcomes

- “Okay, so what do I dosell my couch and start a revolution?”

- Conclusion: The point isn’t guiltit’s agency

- Experiences: How this shows up in real life (about )

- SEO tags (JSON)

Let’s start with a spicy truth: wealth inequality doesn’t worsen by accident. It worsens because millions of everyday decisionsby voters,

consumers, homeowners, investors, managers, and “not my problem” bystandersstack up like Jenga blocks. And yes, that means some of it

is “your fault.” Not in the cartoon-villain way. More like the “you kept clicking ‘Accept All Cookies’ and now the internet knows your soul” way.

Before you throw your phone into a decorative bowl labeled SELF-CARE, a quick comfort: this isn’t a shame parade.

People don’t create inequality singlehandedlysystems do. But systems are basically the sum of incentives we tolerate, policies we vote for (or skip),

and social norms we shrug at. If inequality is a machine, most of us aren’t the CEO… but plenty of us keep tossing quarters into it.

Wealth inequality vs. income inequality (and why wealth is the big boss)

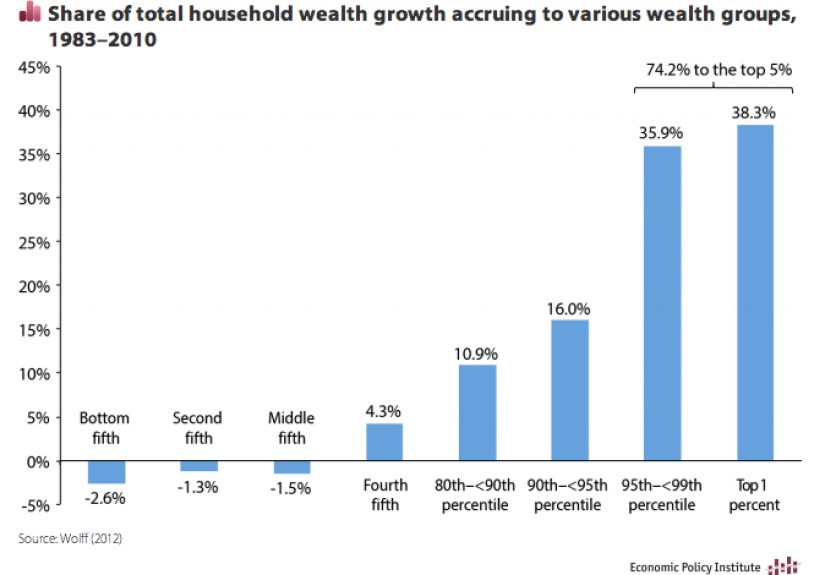

“Income inequality” is about paychecks. “Wealth inequality” is about what you already own: home equity, retirement accounts, businesses, stocks,

and inherited assetsminus debt. Income pays the bills. Wealth changes the rules.

Here’s why wealth matters more: wealth can grow while you sleep. It can compound, appreciate, and generate income. It can also absorb shocks.

If your car dies and you have savings or assets, it’s an annoyance. If you don’t, it’s a crisis with a side quest called “high-interest debt.”

Over time, that gap compounds into different lives: who can move for a better job, who can take an unpaid internship, who can start a business,

who can buy into a good school district, and who can survive a layoff without falling through the floor.

The uncomfortable truth: inequality is a team sport

Wealth inequality grows when society consistently does three things:

(1) rewards owning more than working,

(2) restricts access to the best “wealth-building” opportunities,

and (3) protects existing winners with rules that sound reasonable until you zoom out.

So where do everyday people fit in? In the habits and choices that quietly reinforce those three patterns.

Let’s talk about the most common ways we help inequality keep its gym membership.

1) We clap for “the economy” when we really mean “asset prices”

A lot of public conversation treats a rising stock market like a national mood ring. Green arrow? Everyone’s winning!

Except that stock ownership is heavily concentrated, and many households have little to no exposure to stocks beyond a modest retirement accountor none at all.

When policy and news obsess over asset growth, the winners tend to be people who already have assets.

On a personal level, this shows up when we accept “record corporate profits” as a success metric even if wages, job security, and affordability don’t improve.

We end up prioritizing the health of portfolios over the health of paychecks because portfolios have better publicists.

2) We support tax rules that favor wealthbecause “maybe someday”

Wealth grows fastest when the returns to owning assets are taxed gently or inconsistently compared with the returns to working.

Preferential treatment for long-term investment income can encourage investment, surebut it also magnifies the advantage of already owning investments.

Many middle-income people support these rules because they hope to be “future rich,” or they fear any change will punish their own retirement savings.

That fear isn’t irrational. But it can become a blanket veto: we oppose reforms that could reduce extreme concentration even when those reforms are designed

to target the very top and protect typical savers.

The result: a tax and policy environment that often treats wealth like a fragile houseplant (“be careful!”) and wages like a rented mule (“it can take it”).

We don’t have to demonize success to admit the playing field tilts when ownership gets the soft pillows.

3) We treat housing like an investment firstand a home second

Housing is the biggest wealth-building tool for many American families. That’s exactly why it becomes a political battleground.

When homeowners prioritize rising property values, they often oppose changes that could make housing more affordablelike new apartments,

smaller homes, accessory dwelling units, or mixed-use development.

The most common script is: “I’m not against housing, I’m just against that housing… right here… near my parking… and my view… and my vibes.”

Local rules that limit density can reduce supply, raise prices, and make it harder for new families to buy in.

If wealth grows through home equity, then restricting entry is like pulling the ladder up behind youpolitely, at a city council meeting, with donuts.

This isn’t only about individual homeowners. It’s about communities deciding that exclusivity is “character.”

But when “character” means “only people who already have money can live here,” the wealth gap doesn’t just persistit becomes geographic.

4) We normalize “shareholder-first” business behavior

Modern corporate culture often treats shareholder returns as the ultimate scoreboard. That can push companies toward strategies like aggressive

cost-cutting, automation without worker support, and distributing more cash to investors rather than reinvesting in workers, training, or long-term stability.

And guess what? Ordinary people participate, tooespecially if we own mutual funds or retirement accounts (which is common).

We cheer quarterly beats. We complain about high prices but celebrate record earnings. We want companies to be “responsible,”

as long as responsibility doesn’t reduce returns.

None of this means investing is bad. It means we should be honest: when corporate decision-making prioritizes capital over labor,

wealth tends to concentrate upward. If we don’t like the outcome, we can’t pretend we’re not part of the audience.

5) We shrug at bargaining powerand then act shocked at wage stagnation

When workers have less bargaining power, a smaller share of economic growth tends to show up in pay. One major factor is the long-run decline

of collective bargaining in many industries. Another is how hard it is to switch jobs safely when healthcare, childcare, or unpredictable scheduling

makes “just leave” sound like advice from someone with a trust fund and a Peloton.

As individuals, we contribute when we:

(a) treat wages as a “cost problem” rather than a distribution choice,

(b) judge labor organizing as inherently annoying or outdated,

(c) reward businesses only for low prices, not for fair practices,

or (d) accept workplaces where pay transparency is taboo.

If you’ve ever said, “Why don’t people just negotiate?” while ignoring that negotiation power depends on leverage,

congratulationsyou’ve met the invisible hand, and it’s doing jazz hands.

6) We run the “meritocracy treadmill” that advantages people with cushions

The American story loves a self-made hero. The problem is that the “self” often comes with hidden scaffolding:

family help, a paid-off car, a spare bedroom, a safety net, a relative who can spot rent, a school district that doesn’t have to fundraise for pencils.

Meanwhile, we’ve turned opportunity into a high-stakes tournament. Parents feel pressure to buy into “good” neighborhoods, pay for tutoring,

stack extracurriculars, and treat college admissions like a second job. Those who can afford the treadmill gain speed.

Those who can’t are told to “work harder” while running in place.

Even common career advice can widen gaps: “Take the internship for experience” assumes someone else pays your bills.

“Move to a high-opportunity city” assumes you can handle deposits, higher rent, and job-search downtime.

Merit matters. So does money. Pretending otherwise is one way inequality keeps its mask on.

7) We accept debt as the default bridge to the middle class

Debt can be a useful tooluntil it becomes the admission price for education, stability, and basic dignity.

When households must borrow heavily to access opportunity, the payoff depends on timing, interest rates, job markets,

and whether life behaves itself (spoiler: life is a chaotic gremlin).

We contribute when we normalize systems where people finance necessities at punishing rates while wealthier households can pay cash,

invest earlier, and avoid the “interest tax.” Debt burdens can delay homeownership, reduce savings, and make families more vulnerable to shocksexactly

the opposite of what’s needed to narrow the wealth gap.

8) We treat inheritance as “private,” even though it shapes public outcomes

Intergenerational transfersinheritances, family gifts, help with down payments, informal supportare a huge part of how wealth persists.

They aren’t immoral. They’re human. But when large transfers accumulate at the top, society starts to look less like a meritocracy and more like a relay race

where some people get handed a baton and others get handed a bill.

We contribute when we pretend family wealth has no social impact. Or when we talk about “self-made” success without acknowledging that some people start

closer to the finish line, with water stations and a personal fan club.

“Okay, so what do I dosell my couch and start a revolution?”

You don’t have to become a full-time policy nerd (unless that’s your hobbyno judgment).

But you can stop being an accidental donor to inequality. Here are practical ways to reduce the “my fault” factor without turning your life into a spreadsheet.

Change what you reward

- As a consumer: When possible, support businesses with fair scheduling, transparent pay, and decent benefits. Cheap is not the same as affordable if it comes with hidden social costs.

- As an employee or manager: Advocate for pay transparency, fair raises, and clear promotion paths. “We can’t afford it” is often a choice about priorities, not a law of physics.

- As an investor: If you invest, look at funds and policies that consider long-term value creation, not just short-term extraction.

Stop treating local politics like background noise

National debates get the spotlight, but local rules shape daily life: housing supply, school funding, transit access, and zoning. If you’ve ever complained

about rent, commute times, or “no one can buy a house anymore,” congratulationsyou have a local politics problem.

- Support practical housing solutions (a mix of housing types, smarter density, and faster permitting) that let more families access opportunity.

- Pay attention to who shows up at city meetingsbecause it’s usually not the people working two jobs.

Vote like you understand compounding

Wealth inequality compounds over decades. So do policy choices. If you want a smaller wealth gap, look for proposals that improve:

wages, access to asset-building, fair taxation of extreme wealth, affordable housing, healthcare stability, childcare access, and education pathways

that don’t require lifelong debt.

You don’t have to agree with every policy idea. But you should be allergic to slogans that promise “growth” while ignoring who captures it.

Have the awkward conversations

Inequality thrives in silence. Talk about pay with coworkers (where legal). Discuss how family support shapes outcomes.

Ask what “fair” means in your community when it comes to housing, schools, and opportunity.

Being polite is great. Being politely avoidant is how unfairness becomes tradition.

Conclusion: The point isn’t guiltit’s agency

If this article made you feel mildly called out, good. That’s the sound of awareness forming a little union in your brain.

Wealth inequality isn’t just a fate delivered by distant billionaires and abstract markets. It’s reinforced by ordinary incentives and ordinary choices:

what we praise, what we fear, what we vote for, what we block in our neighborhoods, and what we accept as “just how it works.”

You didn’t build the system alone. But you can stop helping it run on autopilot. The real opposite of inequality isn’t perfectionit’s participation.

Experiences: How this shows up in real life (about )

Picture a middle-class couple who finally buys a starter home after years of saving. They’re proud, relieved, and honestly a little traumatized by the

bidding war. A year later, a new housing proposal appears: a small apartment building and a handful of townhomes nearby. Their first reaction isn’t,

“Great, more people can afford to live here.” It’s, “Will this hurt our home value?” They attend a meeting, not because they hate newcomers,

but because this house is their biggest asset. They vote for “neighborhood character.” The project dies. Prices rise again. They feel like they protected

their futurewithout realizing they also protected the scarcity that keeps other families out.

Or think about a talented student who gets accepted into a great program, but the unpaid internship required to “break in” would mean months without income.

A classmate takes it easilybecause their parents cover rent. The student with bills takes a different job, gains less industry experience,

and gets told later they lack the “right background.” Nobody thinks they’re enforcing inequality. They’re just following norms. But norms can be brutal.

Now zoom into the workplace. A manager wants to give bigger raises to the team, but the budget is tight. Executives are also pressuring everyone to hit

aggressive profit targets. The manager compromises: small raises, a promise of “growth opportunities,” and maybe a pizza party (the unofficial currency of

corporate guilt). Meanwhile, the company announces a big cash return to investors because it “signals confidence.” Employees feel like the business values

themright up until it doesn’t. The manager isn’t a villain. The incentives are.

At a family gathering, someone mentions that their kid bought a house in their twenties. The room nods politely until the details slip out:

a “little help” with the down payment, a car gifted after graduation, and a temporary stay at home to save. Another cousin, equally hardworking,

can’t do any of that because their parents are struggling. One cousin gets to invest early; the other pays interest. Ten years later, the first cousin has

equity and options. The second has experience and exhaustion. Both have “worked hard,” but only one has compounding on their side.

Finally, there’s the news cycle experience: headlines celebrate a strong economy because markets are up. A friend asks, “Does that mean things are better?”

You look around at rent, groceries, childcare, and student loan balances and say, “Not for everyone.” That momentwhen national success indicators don’t match

lived realityis where many people either disengage (“it’s all rigged”) or get curious (“what would make growth show up in pay and stability?”).

The difference matters. Disengagement is oxygen for inequality. Curiosity is the start of change.