Table of Contents >> Show >> Hide

- What the Ramp data is really measuring

- Why OpenAI still holds the stronger headline position

- Why Anthropic’s velocity curve keeps getting harder to ignore

- The most important chart may be the overlap chart

- Penetration versus velocity: which metric matters more?

- Why this race is really about product shape, not just market share

- What enterprise buyers should watch next

- Experience from the field: what this rivalry looks like inside real organizations

- Conclusion

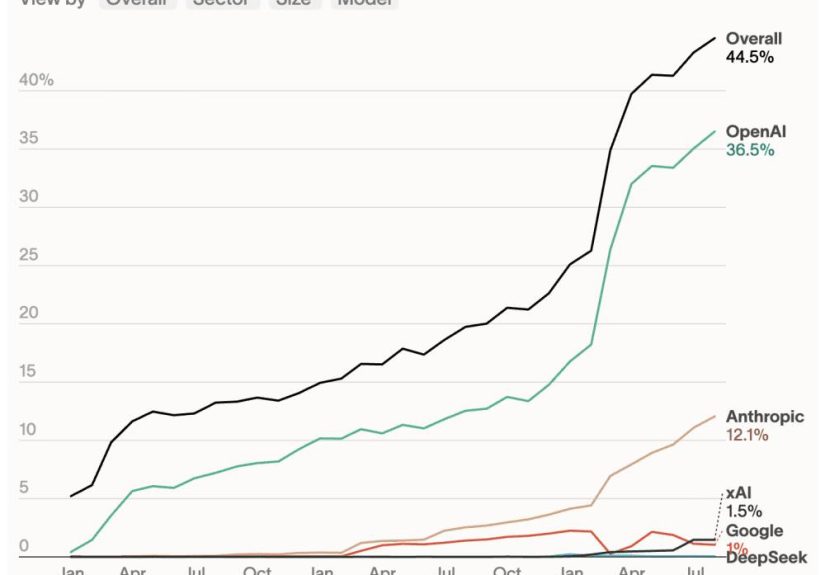

If you only glance at the scoreboard, this looks like a comfortable OpenAI win. A penetration snapshot around 36% for OpenAI versus roughly 12% for Anthropic makes the race look lopsided, like one team is already printing championship T-shirts. But AI markets are not baseball cards. Installed base matters, sure, yet the more revealing metric is often the slope of the line, not just the height of the bar.

That is why the OpenAI-versus-Anthropic debate has gotten a lot more interesting than the headline numbers suggest. OpenAI still looks like the category leader in direct business adoption, thanks to its massive ChatGPT footprint, earlier enterprise launch, and broad product reach. Anthropic, however, has been acting like the fastest kid on the moving walkway: smaller overall, but gaining speed in ways that can reshape the race.

And here is the real twist: the market is not yet zero-sum. Companies are not always replacing OpenAI with Anthropic or vice versa. Many are buying both, testing both, and routing different jobs to different models. So if you are trying to understand who is “winning,” the honest answer is a little annoying and a lot more useful: it depends on whether you care most about penetration, spending share, product fit, or momentum.

What the Ramp data is really measuring

Ramp’s AI Index is valuable because it is based on real business spending rather than vibes, wishful PowerPoint arrows, or that one coworker who says, “Everyone I know uses Claude now.” Its methodology tracks paid AI adoption using corporate card and bill-pay data across a large sample of American businesses. That gives us a solid window into how companies are actually spending money on AI tools.

But it is not a perfect map of the entire enterprise market. It captures visible, direct purchases: subscriptions, tool spend, and model usage that shows up in normal procurement channels. It does not cleanly capture every giant enterprise contract, every bundled cloud relationship, or every AI feature tucked inside broader software commitments. In other words, it shows the part of the iceberg floating above the waterline, not the whole frozen drama underneath.

That matters because a 36% versus 12% penetration snapshot can be directionally true for a moment in time while still missing bigger structural realities. The title number reflects an earlier market view. Later Ramp updates already showed Anthropic climbing sharply while OpenAI remained ahead, which is exactly why the velocity story deserves more attention than the static screenshot.

Why OpenAI still holds the stronger headline position

OpenAI’s advantage starts with distribution. ChatGPT became a mainstream habit before most enterprises had formal AI policies, which is both hilarious and extremely effective. Employees tried it at home, then at work, then in meetings, then probably during meetings that should have been emails. That consumer-to-work flywheel is hard to overstate.

Once a product becomes familiar at the individual level, enterprise rollout gets easier. Training is lighter. Internal champions are easier to find. Procurement friction drops because people already understand the use cases. OpenAI has benefited enormously from that pattern, and its own enterprise materials lean into it for good reason.

OpenAI also moved early with ChatGPT Enterprise, giving it a head start in security, privacy controls, admin tooling, and broader organizational deployment. Add in multimodal strength, mature APIs, agent tooling, strong brand recognition, and an ever-expanding business user base, and the case for OpenAI’s leading penetration becomes pretty straightforward. It is the familiar default, the broad platform, and the option many companies adopt first.

That first-vendor advantage matters because once OpenAI gets into the building, it often spreads across departments. Marketing uses it for campaign drafts. Support teams use it for knowledge retrieval. Finance leans on it for analysis. Product and engineering use it for prototyping. The result is wide organizational footprint, even when some teams later decide that another model is better for specific tasks.

OpenAI’s strategic edge is breadth

OpenAI looks strongest where enterprises want one vendor that can do many things reasonably well, and a few things exceptionally well. Its platform story is broad: chat, APIs, coding, reasoning, image generation, voice, enterprise controls, and increasingly agent-style workflow automation. For CIOs trying to reduce tool sprawl, that breadth is appealing.

It also helps that OpenAI is not acting like a company content to defend its lead. It is leaning harder into enterprise delivery, including partnerships designed to move customers from “cool pilot” to “actual production system.” That tells us OpenAI understands the next phase of this market is not just model quality. It is implementation, governance, reliability, and proving ROI in boring-but-important business workflows.

Why Anthropic’s velocity curve keeps getting harder to ignore

If OpenAI owns the bigger base, Anthropic owns more of the suspense. The reason is simple: its growth line has looked steeper in the business market, especially as coding, agentic workflows, and long-context document work have become more valuable.

Anthropic’s rise is not just a story about one good quarter or one flashy benchmark. It has been building a reputation around reliability, steerability, and strong performance in coding-heavy environments. That combination lands well with enterprises, especially the ones that are tired of prompt gymnastics and want outputs that feel stable enough to operationalize.

In developer circles, Claude has earned serious traction. That matters because software development is one of the earliest AI use cases with obvious, measurable value. If a model makes engineers faster, improves code review quality, and handles large codebases without turning into a caffeinated intern, enterprises notice fast. They may start with a few seats, then add API usage, then expand into adjacent functions. That is how velocity becomes share.

Anthropic’s strategic edge is trust plus coding strength

Anthropic has positioned itself as the model company for serious work: long documents, regulated settings, high-trust environments, and agentic coding tasks where consistency matters. Menlo Ventures’ enterprise work has reflected that shift, showing Anthropic outperforming OpenAI in enterprise LLM spending and widening its lead in coding-related usage.

That does not mean Anthropic has already beaten OpenAI in the broad enterprise market. It has not. But it does suggest Anthropic has found a wedge that matters: win technical teams first, prove reliability, and expand into departments that care more about predictability than consumer fame.

There is also a commercial signal here. Anthropic has reported a business-heavy revenue mix, and its enterprise customer count has expanded rapidly. That suggests the company is not simply winning admiration on social media or benchmark charts. It is turning model preference into paid adoption, which is the metric that makes CFOs, investors, and procurement teams stop pretending AI is just an innovation sandbox.

The most important chart may be the overlap chart

Here is where the story gets much smarter than “OpenAI good, Anthropic catching up.” Ramp’s data indicates that a large majority of Anthropic customers also pay OpenAI. That means Anthropic’s rise is not mostly coming from ripping OpenAI out of organizations. It is often entering as a second vendor.

That is a huge clue about how enterprise AI is being bought in real life. Companies are not choosing a single model provider and getting married under a lovely procurement arch. They are testing multiple vendors by use case. OpenAI may be the default general assistant. Anthropic may be the coding workhorse or the trusted analyst for long documents. Google may sit inside broader productivity or cloud arrangements. In short, enterprises are buying portfolios, not soulmates.

That overlap changes how we should interpret velocity curves. If Anthropic is gaining mostly through multivendor expansion, its slope is still impressive, but the next test is harder: can it become the primary vendor rather than the clever second one? Can it turn dual-vendor experimentation into consolidation in its favor?

OpenAI faces the mirror-image question. Can it keep the broad lead while preventing specialized erosion? It does not need to win every workload. But it does need to avoid becoming the generalist provider that everyone likes and fewer teams love.

Penetration versus velocity: which metric matters more?

Penetration tells you who got there first and who is currently inside more organizations. Velocity tells you where buyer energy is moving right now. In early markets, velocity can be more predictive than penetration because share can shift quickly once real use cases harden.

That said, it is dangerous to fall in love with momentum charts. A steep line looks sexy right up until it meets enterprise reality: governance reviews, security audits, integration headaches, budget cycles, and the ancient art of “let’s revisit this next quarter.” Plenty of fast-growing tools hit the wall when expansion gets harder than initial adoption.

So the right interpretation is not that Anthropic’s velocity makes OpenAI’s lead irrelevant. It is that the lead is less settled than the topline number suggests. OpenAI has scale and distribution. Anthropic has sharper recent momentum in some of the highest-value enterprise workloads. Both can be true at once, and annoyingly, they are.

Why this race is really about product shape, not just market share

OpenAI and Anthropic are not selling identical products with different logos. They are increasingly selling different operating philosophies for enterprise AI.

OpenAI’s pitch is broad platform power. It wants to be the general-purpose layer that individuals adopt quickly and organizations can standardize around. Anthropic’s pitch is focused performance and reliability, especially in coding, reasoning, and structured knowledge work. One says, “We can do nearly everything.” The other says, “We can be the model you trust for the jobs that matter most.”

That distinction explains why the race can produce mixed signals. OpenAI can lead penetration while Anthropic gains wallet share in certain enterprise segments. OpenAI can dominate top-of-funnel adoption while Anthropic wins technical evaluations. OpenAI can own mainstream familiarity while Anthropic owns the room when the conversation shifts to coding productivity and model steerability.

The market is large enough for both stories to coexist for now. But over time, that coexistence gets more expensive. Running two frontier vendors is not free, not simple, and not something procurement teams dream about for fun. Eventually, many organizations will consolidate more aggressively. When that happens, velocity curves turn into hard market-share consequences.

What enterprise buyers should watch next

The next chapter in this rivalry will not be decided by one benchmark or one month of subscription data. It will be decided by a handful of boring metrics that end up being wildly important.

1. Whether dual-vendor overlap starts shrinking

If companies keep paying both OpenAI and Anthropic, the market stays exploratory. If overlap begins to fall, consolidation has begun, and then the real competitive winner starts to emerge.

2. Whether Anthropic keeps expanding beyond coding

Claude’s reputation in software work is a major advantage. The next test is whether that credibility spreads into legal, finance, operations, research, and companywide workflow automation at scale.

3. Whether OpenAI turns familiarity into deeper system lock-in

Consumer popularity gets you in the door. Enterprise durability comes from integration, workflow depth, admin controls, and measurable business outcomes. OpenAI knows this, which is why its enterprise push now looks much more hands-on.

4. Whether procurement starts caring more about stability than novelty

In the early phase, the newest capability can win attention. In the production phase, stability wins budgets. Enterprises do not want their core workflows to feel like they are attached to a rocket skateboard.

Experience from the field: what this rivalry looks like inside real organizations

In practice, the OpenAI-versus-Anthropic battle rarely looks like a clean, top-down executive decision. It usually starts messier, and honestly, much more human. One team is already using ChatGPT because everyone knows what it is. Another team, usually engineering, quietly starts preferring Claude because it handles code review, refactoring, or large-context work with less babysitting. Before long, the company has two AI standards, three pilot programs, six opinions, and one procurement manager developing a stress twitch.

A common pattern is this: OpenAI wins the first wave because it is familiar, broad, and easy to justify. Employees already know the interface. Leaders have heard of the brand. The tool feels like the safe mainstream choice. Then the second wave begins. Developers compare outputs. Analysts compare reasoning quality. Legal and compliance teams compare tone, consistency, and how much prompt-engineering duct tape is required to get reliable results. That is often where Anthropic starts gaining ground.

Another recurring experience is that companies do not really want a philosophical AI debate. They want workflows that work. If OpenAI helps support agents answer faster, it stays. If Claude writes better internal tools, it stays too. The market’s messy overlap makes perfect sense when you see how organizations adopt technology: they optimize locally before they standardize globally.

There is also a very practical budget story underneath all of this. Teams will happily add a second model provider when the productivity gain feels obvious. But once finance starts asking why the company is paying for overlapping capabilities, the bar rises. That is when “Which model do people like?” turns into “Which vendor can support our most important workflows with the least operational friction?” This is where velocity curves meet the cold stare of procurement.

Experience also shows that model choice is becoming role-specific. Product managers may prefer OpenAI for broad ideation and multimodal tasks. Engineers may lean toward Anthropic for coding and agentic development. Finance teams may mix both depending on spreadsheet work, research depth, and auditability. The end state is rarely one magical model doing everything perfectly. It is usually an organization figuring out which model deserves to sit closest to the highest-value tasks.

That is why the Ramp numbers matter so much. They are not just a scorecard. They capture an in-between phase of the market, where broad leaders and fast gainers can both be right, and where second-vendor adoption can be the bridge to future consolidation. OpenAI still looks like the default giant. Anthropic looks like the fast-rising specialist with ambitions to become much more than that. The most realistic enterprise experience today is not choosing between them once. It is living with both long enough to discover which one earns the right to stay everywhere.

Conclusion

OpenAI still owns the cleaner headline. A higher penetration figure, a bigger installed base, and enormous user familiarity make it the most visible leader in enterprise AI. But visibility is not the same thing as inevitability.

Anthropic’s velocity curve, especially in coding-heavy and trust-sensitive workloads, suggests the market is still being shaped in real time. The more important takeaway from Ramp’s data is not that OpenAI is losing. It is that Anthropic is gaining in ways that traditional market-share snapshots can underestimate.

So yes, 36% versus 12% sounds decisive. But the smarter read is this: OpenAI has the lead, Anthropic has the momentum, and the real enterprise AI war will be decided when multivendor experimentation turns into single-vendor standardization. Until then, the bars tell one story, and the curves tell another.