Table of Contents >> Show >> Hide

- What Were “Covid Multiples” in SaaS?

- Why SaaS Valuations Exploded During Covid

- The Correction: When the Market Remembered Gravity

- Were Covid Multiples an Anomaly or a Preview?

- The New SaaS Valuation Playbook

- Public SaaS vs. Private SaaS: Why the Gap Matters

- Examples: What the Boom and Reset Taught Us

- So, What Is the “Normal” SaaS Multiple Now?

- What Founders Should Learn From Covid Multiples

- What Investors Should Learn From the SaaS Boom

- Final Verdict: An Anomaly, But Not a Mirage

- Experience Notes: What the SaaS Multiple Roller Coaster Felt Like in Practice

- Conclusion

- SEO Tags

Note: This article is for market analysis and educational publishing purposes only. It is not investment, legal, tax, or fundraising advice.

The short answer is yesbut with an asterisk large enough to need its own cloud storage plan. The Covid-era SaaS multiples were not simply “normal valuations with better snacks.” They were the product of emergency interest rates, forced digital adoption, abundant venture capital, public-market enthusiasm, and a belief that software growth could keep floating upward like a motivational poster in a boardroom. But calling them a total hallucination would also be too easy. The pandemic did accelerate real software adoption. It did pull years of cloud transformation into a few chaotic quarters. It did prove that many SaaS products were no longer “nice-to-have” but mission-critical.

So, were the Covid multiples in SaaS just an anomaly? Mostly, yes. But they were an anomaly built on real trends, inflated by temporary conditions, and corrected by a market that eventually remembered math exists.

What Were “Covid Multiples” in SaaS?

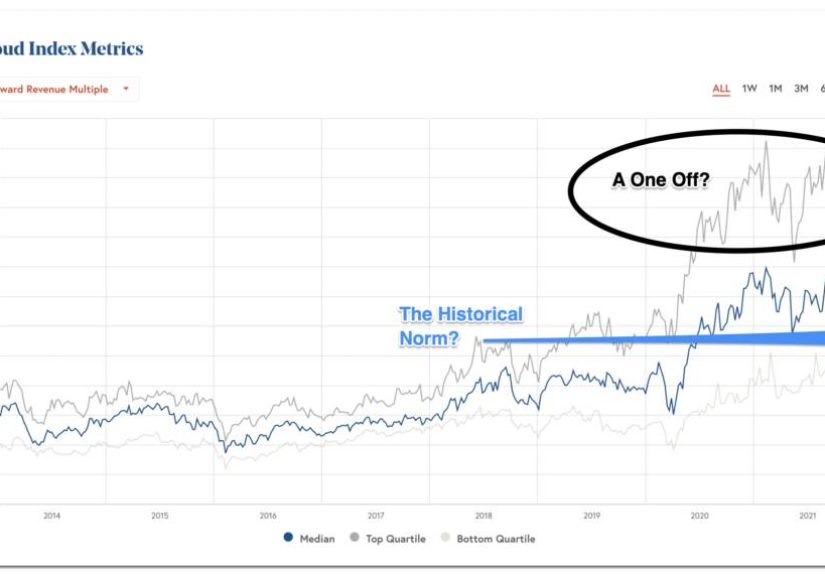

In SaaS, a “multiple” usually means a valuation compared with revenue, annual recurring revenue, or forward revenue. If a company generates $100 million in ARR and trades at 20x ARR, the market is valuing it at roughly $2 billion before other adjustments. During 2020 and 2021, many public and private SaaS companies saw their valuation multiples expand dramatically. Some high-growth names traded at forward revenue multiples that looked less like finance and more like someone accidentally leaned on the calculator.

Before the pandemic, a strong public SaaS company might command a healthy premium because subscription software had attractive qualities: recurring revenue, high gross margins, expansion potential, sticky customers, and scalable distribution. During the pandemic, those qualities were turbocharged. Suddenly, every organization needed remote collaboration, digital payments, cloud infrastructure, cybersecurity, workflow automation, online customer support, and analytics. SaaS was no longer the future; it was the emergency exit.

That surge created a powerful story: cloud software was eating the world faster than expected. Investors paid up for growth, often far into the future. The trouble was that future revenue is worth much more when interest rates are near zero. When rates rose, those dreamy long-term cash flows had to come back down to Earth. They did not land gently. They arrived like a dropped laptop.

Why SaaS Valuations Exploded During Covid

1. Digital Transformation Went From “Someday” to “By Friday”

Before 2020, many companies talked about digital transformation the way people talk about cleaning the garage: important, inevitable, and conveniently postponed. Covid changed that. Offices closed, employees went remote, sales teams moved online, customer support became distributed, and IT teams had to secure everything from kitchen tables to spare bedrooms. SaaS vendors were suddenly solving urgent operational problems.

Video conferencing, collaboration software, digital signatures, cloud security, HR platforms, project management tools, developer platforms, and data infrastructure all benefited from this shift. Investors extrapolated those adoption curves as if the emergency growth rate might become the permanent growth rate. For a while, it seemed reasonable. When a company doubles revenue in a year, even sober analysts start using exciting adjectives.

2. Near-Zero Interest Rates Made Growth Look Magical

The Federal Reserve cut rates aggressively in March 2020, bringing the federal funds target range down to 0% to 0.25%. That mattered enormously for SaaS valuations. High-growth software companies are often valued based on expected cash flows many years in the future. When discount rates are low, those future cash flows are worth more today. When discount rates rise, the same cash flows are worth less.

This is why SaaS valuations are sometimes called “long-duration equities.” Much of the value sits in the future. During the zero-rate period, investors were willing to pay premium prices for companies that could grow quickly, even if profits were years away. Growth was the hero. Profitability was the supporting character who appeared briefly in season three.

3. Venture Capital and Public Markets Fed Each Other

The public market boom raised the ceiling for private SaaS valuations. If public cloud companies traded at huge revenue multiples, venture investors could justify paying similarly rich prices for private companies with faster growth. Private founders saw public benchmarks and asked for higher valuations. Investors agreed because capital was plentiful and the fear of missing the next category winner was intense.

This feedback loop produced a familiar pattern: public SaaS stocks rose, private rounds got bigger, more startups hired aggressively, revenue growth became the headline metric, and burn rates were treated like a minor weather condition. In the hottest categories, “efficient growth” sounded almost old-fashioned, like fax machines or remembering your voicemail password.

The Correction: When the Market Remembered Gravity

The SaaS multiple correction began as interest rates rose and inflation concerns took over the market narrative. By 2022, investors had shifted from “How fast can this company grow?” to “Can this company generate cash before the sun burns out?” The answer mattered. Companies with high growth and strong margins held up better. Companies with slowing growth, weak retention, or heavy cash burn saw multiples compress sharply.

Public SaaS benchmarks show the scale of the reset. Market commentary from firms tracking public software companies has shown median revenue multiples falling dramatically from 2021 peaks. Meritech’s public SaaS data, for example, showed the median enterprise value to next-twelve-month revenue multiple down from the 2021 high, while the highest-multiple companies suffered some of the steepest compression. SaaS Capital later described the 2025 environment as a return to a “low normal” level, but with a wider spread between winners and weaker performers.

That last part is important. The market did not stop liking SaaS. It stopped giving every SaaS company a participation trophy with a 20x revenue multiple attached. Premium multiples became reserved for businesses with strong growth, high retention, efficient acquisition, meaningful free cash flow, durable product moats, and credible AI strategies. In other words, the market did not become anti-software. It became allergic to sloppy software economics.

Were Covid Multiples an Anomaly or a Preview?

The best answer is that Covid multiples were an anomaly in price, but not in direction. The pandemic did not invent cloud adoption. It accelerated it. SaaS was already winning because businesses preferred flexible subscriptions, remote access, rapid deployment, and lower infrastructure burden. Covid simply slammed the accelerator.

However, the valuation multiples attached to that acceleration were not sustainable. They assumed several unusual conditions would persist: ultra-low rates, unusually fast software adoption, abundant capital, low concern about profitability, and a willingness to value companies based on distant potential rather than near-term cash generation. That combination was rare. It may happen again in some form, but founders should not build operating plans around it. Hope is not a pricing model.

A healthier view is this: Covid multiples revealed what investors are willing to pay when growth feels scarce, software feels essential, and money is cheap. The post-Covid correction revealed what investors demand when money has a real cost. Both periods taught useful lessons, but only one is safe to use as a base case. Spoiler: it is not the one where every pitch deck looked like it had been sprinkled with valuation confetti.

The New SaaS Valuation Playbook

Growth Still Matters, But Efficient Growth Matters More

Growth has not gone out of style. A SaaS company growing 40% or 60% annually with strong retention will still attract attention. But growth without discipline is no longer automatically rewarded. Investors now ask how much cash is being consumed to produce each dollar of ARR. They look at burn multiple, sales efficiency, payback period, gross margin, and free cash flow margin. If the company is growing fast but spending like a pirate who just discovered corporate cards, the market notices.

The Rule of 40 has become a popular shorthand for this new balance. It combines revenue growth and profitability margin. A company growing 30% with a 10% free cash flow margin hits 40. A company growing 70% while losing 60% does not. In the Covid period, the second company might have received a standing ovation. Today, it gets a spreadsheet and several uncomfortable questions.

Retention Is Now a Valuation Superpower

Net revenue retention has become one of the most important SaaS metrics because it shows whether existing customers expand, renew, or quietly wander off to competitors. Strong NRR means the company can grow without relying entirely on new logo acquisition. That matters when sales cycles lengthen, budgets tighten, and buyers demand proof of return on investment.

During the boom, investors often tolerated weak retention if top-line growth was impressive. In the current market, weak retention is a warning flare. If customers are not expanding or staying, revenue quality suffers. A SaaS company with 120% NRR and efficient growth can deserve a premium. A company with 85% gross retention and heavy discounting may discover that “recurring revenue” is less recurring than the board hoped.

AI Has Reopened the Multiple Debate

Artificial intelligence has complicated the SaaS valuation conversation. AI-native companies can command premium valuations because they may unlock new markets, automate labor-heavy workflows, and grow faster than traditional SaaS vendors. Bessemer and Battery have both framed AI as a major platform shift for cloud software. The Cloud 100 data also shows AI companies taking a larger share of private cloud valuation.

But AI is not a magic sticker that turns a 4x revenue company into a 25x revenue company overnight. Investors are becoming more selective. They want to know whether AI improves the product, expands the market, reduces churn, increases pricing power, or creates defensible data advantages. “We added a chatbot” is not a moat. It is often just a support ticket wearing sunglasses.

Public SaaS vs. Private SaaS: Why the Gap Matters

Public SaaS markets repriced quickly because public stocks trade daily. Private markets move more slowly. Founders and investors often need several quarters to accept that the old valuation environment is gone. This creates a lag: public comps fall first, private rounds slow, down rounds appear, M&A conversations reset, and eventually everyone updates their mental model.

During 2020 and 2021, private valuations often followed public cloud enthusiasm upward. After 2022, the reverse happened. Public multiples compressed, and private investors became more cautious. Companies that raised at high Covid-era valuations faced a difficult choice: grow into the old price, raise a flat or down round, cut expenses, sell, or wait. None of those options are especially fun, though “wait and improve the business” is usually more dignified than pretending 2021 is coming back next Tuesday.

For private SaaS companies today, valuation depends heavily on quality. Vertical SaaS with strong retention, mission-critical workflows, low churn, and clear profitability can still attract strong multiples. Horizontal SaaS companies facing AI disruption, weak differentiation, or seat-based pricing pressure may see more skepticism. The market is no longer buying “SaaS” as a category. It is buying specific businesses with specific economics.

Examples: What the Boom and Reset Taught Us

Zoom became the symbol of pandemic software adoption because its growth exploded as remote work became unavoidable. That growth was real, but the pandemic-level adoption curve was not infinitely repeatable. Once the world reopened and growth normalized, the market had to value the business on a more mature trajectory.

Snowflake, Datadog, and other high-quality cloud software companies showed another lesson: great businesses can still experience multiple compression. A company can execute well and still see its valuation fall if the market changes the price it is willing to pay for each dollar of revenue. That distinction is crucial. Multiple compression is not always a business failure. Sometimes it is a market-wide repricing.

On the other hand, companies with weaker unit economics suffered more because investors no longer wanted growth at any cost. In 2021, a company could raise money by showing fast ARR growth and a giant market opportunity. By 2023 and 2024, the follow-up questions became sharper: What is churn? How long is payback? What is gross margin after cloud infrastructure costs? Is the sales team productive? Can the company reach breakeven without another heroic financing round?

So, What Is the “Normal” SaaS Multiple Now?

There is no single normal SaaS multiple because SaaS is no longer treated as one uniform category. A slow-growing, low-margin SaaS company may trade at a modest revenue multiple. A high-growth, profitable, mission-critical platform may command a much higher one. AI-native companies with extraordinary traction may trade above traditional software benchmarks, at least while the market believes their growth and defensibility are real.

Broadly, the post-Covid environment looks more like a selective market than a collapsed one. Public SaaS multiples have generally settled far below the 2021 peaks, while private valuations vary widely based on growth, retention, size, profitability, and category. The premium has shifted from “software company” to “excellent software company.” That may feel harsh, but it is healthier. The best businesses can still be valuable. The weaker ones no longer get to hide behind the acronym “ARR” like it is a financial invisibility cloak.

What Founders Should Learn From Covid Multiples

Founders should not treat 2021 valuation multiples as the benchmark for success. That period was distorted by emergency macro conditions and unusual demand patterns. Building a company around the assumption that those multiples will return is risky. It can lead to over-hiring, inflated burn, unrealistic fundraising expectations, and painful strategic delays.

Instead, founders should build for durability. That means focusing on customers who truly need the product, pricing that reflects value, retention that proves stickiness, and a cost structure that can survive market cycles. A company that can grow efficiently in a normal market will be in excellent shape if multiples expand again. A company that only works when capital is free is not a company; it is a mood board with invoices.

The smartest SaaS operators now think in scenarios. What happens if the next round takes twice as long? What if sales cycles stretch? What if a competitor uses AI to undercut pricing? What if customers reduce seat counts? What if public comps fall another 20%? These questions are not pessimistic. They are adult supervision.

What Investors Should Learn From the SaaS Boom

Investors should remember that category tailwinds do not eliminate valuation discipline. SaaS is still one of the most attractive business models in technology when executed well. Recurring revenue, high gross margins, expansion revenue, and workflow lock-in are powerful. But even great models can be overvalued.

The Covid boom encouraged investors to underwrite perfection. The correction reminded everyone that growth decelerates, competition increases, retention can weaken, and capital markets change. The next great SaaS investments will likely come from companies that combine product depth, AI leverage, customer urgency, efficient acquisition, and strong financial controls. In other words, the next winners may look less like “growth at any cost” and more like “growth with receipts.”

Final Verdict: An Anomaly, But Not a Mirage

The Covid multiples in SaaS were an anomaly because they depended on a rare mix of near-zero rates, forced digital adoption, abundant capital, and investor willingness to pay extreme prices for future growth. Those conditions were temporary. The valuation peaks of 2020 and 2021 should not be treated as the default setting for SaaS.

But they were not meaningless. The pandemic confirmed that software is deeply embedded in modern business operations. It accelerated cloud adoption, proved the value of remote-first workflows, and created durable demand for many categories. The anomaly was not that SaaS mattered. The anomaly was how much the market paid for that truth at the peak.

In today’s market, the SaaS companies that deserve premium multiples must earn them the old-fashioned way: by growing, retaining customers, expanding accounts, controlling burn, producing cash, and building products that remain essential even when budgets tighten. Less fireworks, more fundamentals. It may not be as glamorous as the Covid boom, but it is a much better way to build a company that survives longer than a market cycle.

Experience Notes: What the SaaS Multiple Roller Coaster Felt Like in Practice

For operators, investors, and advisors who lived through the Covid SaaS cycle, the experience was less like reading a finance textbook and more like riding a roller coaster designed by someone who had just discovered espresso. In 2020 and 2021, many SaaS teams felt the market pulling them forward. Prospects were more willing to buy digital tools, boards encouraged aggressive hiring, and competitors were raising giant rounds. If a company was growing quickly, the pressure was not simply to keep growing. The pressure was to grow faster before someone else captured the category narrative.

That environment changed behavior. Sales teams expanded. Marketing budgets grew. Product roadmaps stretched. Companies entered new segments earlier than planned. Some of those moves were smart. Others were reactions to a market that rewarded speed more than focus. When capital was cheap, the cost of being inefficient seemed low. In hindsight, it was just hidden. The bill arrived later, wearing a 2022 calendar invite.

One common experience during the boom was that valuation became part of identity. Founders who raised at high multiples were treated as if the valuation itself proved product-market fit. But a valuation is not a customer renewal. It is not a product moat. It is not a support ticket resolved in five minutes. It is a price agreed upon at a moment in time. When the market turned, many teams had to separate ego from execution. That was painful but useful.

The correction also improved conversations. Instead of asking only about ARR growth, serious boards began asking better questions: Which customers are expanding? Which segments churn? What is the true cost of onboarding? Are we selling to buyers with budget authority? Can gross margins improve? What happens if we slow hiring? These questions may sound less exciting than “How fast can we triple?” but they create stronger companies.

Another lesson from the field is that customers became more disciplined too. During the pandemic, some companies bought software quickly because they had no choice. Later, finance teams reviewed SaaS spend more aggressively. Shelfware became a target. Vendors had to prove usage, impact, and ROI. The best SaaS companies adapted by strengthening customer success, refining packaging, and tying pricing to measurable value. The weaker ones discovered that “annual contract” does not mean “automatic love.”

The most practical takeaway is simple: build as if the market will not rescue you. If multiples expand, wonderful. Enjoy the tailwind. But the business should make sense without it. Durable SaaS companies are built on customer pain, retention, product depth, efficient go-to-market, and financial discipline. Covid multiples made many companies look brilliant. The reset showed which ones actually were.

Conclusion

The Covid-era SaaS valuation boom was not pure fantasy, but it was not normal either. It was a temporary overpricing of a genuinely powerful trend. Cloud software did become more important. Digital workflows did accelerate. Remote work did change buying behavior. But the multiples attached to those shifts were inflated by cheap money and extraordinary market psychology.

Today’s SaaS market is more selective, more analytical, and frankly more grown-up. Investors still reward great software businesses, but they expect evidence: efficient growth, high retention, pricing power, and a credible path to cash generation. For founders, that is not bad news. It is a clearer scoreboard. The age of “just add SaaS and stir” is over. The age of durable, measurable, mission-critical software is very much alive.