Table of Contents >> Show >> Hide

- What Is a Wire Transfer (and When Should You Use One)?

- Step 1: Confirm a Wire Transfer Is the Right Tool

- Step 2: Gather the Exact Recipient Details (This Is the Make-or-Break Step)

- Step 3: Verify Everything (Because Wires Don’t Do Second Chances)

- Step 4: Initiate the Wire Transfer Through Your Bank (Online, App, or In Person)

- Step 5: Review, Approve, and Send Before the Cutoff Time

- Step 6: Confirm Delivery, Track the Wire, and Keep Records

- Wire Transfer Fees, Exchange Rates, and “Where Did My Money Go?”

- Wire Transfer Safety Tips (Because Scammers Love Wires)

- Common Wire Transfer Mistakes (and How to Avoid Them)

- FAQ: Quick Answers to Wire Transfer Questions

- Conclusion: Wire Transfers Are PowerfulSo Treat Them Like Power Tools

- Real-World Wire Transfer Experiences (What People Learn the Hard Way)

Wiring money sounds like something only spies and real estate agents dountil you need to move a big chunk of cash fast, safely, and with a paper trail.

A wire transfer is one of the quickest ways to send funds from one bank account to another, especially for large-dollar or time-sensitive payments.

But it’s also one of the least forgiving: the details must be correct, fees can be annoying, and once the money is gone, it can be very hard to get it back.

This guide breaks the process into six clear steps (with practical examples), explains domestic vs. international wires, shows how fees really work,

and includes safety tips to keep your money out of a scammer’s hands and in the right account.

What Is a Wire Transfer (and When Should You Use One)?

A wire transfer is an electronic payment sent through bank-to-bank networks. In the U.S., many bank wires move through systems such as Fedwire

(operated by the Federal Reserve) and CHIPS (used by participating financial institutions), while international wires often use SWIFT messaging

along the route. Translation: it’s a fast, bank-grade way to move moneyusually same-day for domestic wires if you meet the cutoff time.

Wires are commonly used for real estate closings, large contractor payments, earnest money, sending money to family abroad, or business invoices.

For smaller everyday payments, options like ACH transfers, Zelle, or debit cards can be cheaper and easier.

Quick reality check

- Speed: Domestic wires often arrive the same business day; international wires can take a couple of business days (sometimes more).

- Cost: Fees vary by bank and method (online vs. branch). Expect wires to cost more than ACH.

- Finality: Once a wire is sent, it may be impossible to canceland recovery after a mistake or scam is often unlikely.

Step 1: Confirm a Wire Transfer Is the Right Tool

Before you send anything, decide whether a wire is actually the best way. Wires are great when timing is critical or the amount is large.

They’re not great when you’re unsure about the recipient, trying to “test” a new vendor, or paying someone who popped into your DMs

with an urgent story and a new bank account.

Use a wire transfer when:

- You’re paying for a real estate closing or escrow (common requirement).

- You need same-day delivery (and you can meet your bank’s cutoff time).

- You’re sending a large payment where card limits, holds, or delays are a problem.

- You need a formal bank record/receipt for compliance or documentation.

Consider alternatives when:

- You’re sending a small amount and fees would eat your lunch.

- You don’t fully trust the recipient or the request feels “off.”

- You can wait 1–3 business days (ACH is usually cheaper).

Example: If you’re paying a contractor $800 for a minor repair, a wire may be overkill.

If you’re sending $35,000 for a down payment and closing is tomorrow, a wire may be the right move.

Step 2: Gather the Exact Recipient Details (This Is the Make-or-Break Step)

Wiring money is like typing in the world’s most expensive “shipping address.” One wrong digit can delay the transfer, cause it to be returned,

orworst casesend your funds to the wrong place. Your bank will require specific “wiring instructions,” and the list differs for domestic vs. international wires.

For a domestic U.S. wire, you typically need:

- Recipient (beneficiary) name exactly as it appears on the account

- Recipient address (often required)

- Recipient bank name and address

- ABA routing number (wire routing/ABA number, not always the same as ACH routing)

- Recipient account number

- Account type (checking/savings, if asked)

- Purpose or memo (especially for business/real estate)

For an international wire, you may also need:

- SWIFT/BIC code of the recipient bank

- IBAN (common in Europe and many other regions) or local equivalent (varies by country)

- Intermediary/correspondent bank details (sometimes required)

- Currency choice (send in USD or local currency)

- Recipient bank branch information (some countries/banks require it)

Tip: Ask the recipient for official wiring instructions in writing (invoice, contract, bank form, or secure portal),

and compare them with a second source you already trust (like a verified phone call to a known number).

Step 3: Verify Everything (Because Wires Don’t Do Second Chances)

This is the step people skip right before they say, “So… funny story…” to their bank.

Verification is about two things: accuracy and fraud prevention.

Accuracy checks (do these even if you’re in a hurry):

- Confirm the routing number format and bank name match.

- Double-check every digit of the account number.

- Make sure the beneficiary name matches the account (especially for business payments).

- Confirm the currency and any special instructions (international wires love “special instructions”).

Fraud checks (do these especially if anyone “changed the wiring instructions”):

- Call the recipient using a known number (not the one in a suspicious email) to confirm instructions.

- Be skeptical of last-minute changes, urgency, or secrecy requests.

- Watch for look-alike emails/domains (one tiny letter can be a whole scam operation).

- If the request involves real estate, verify through your escrow/title company using verified contact info.

Why so intense? Because wire transfers are often treated like cash: once sent, recovery after a mistake or scam is very unlikely.

If someone is pressuring you to wire money, that’s not a “fun quirk”it’s a giant neon warning sign.

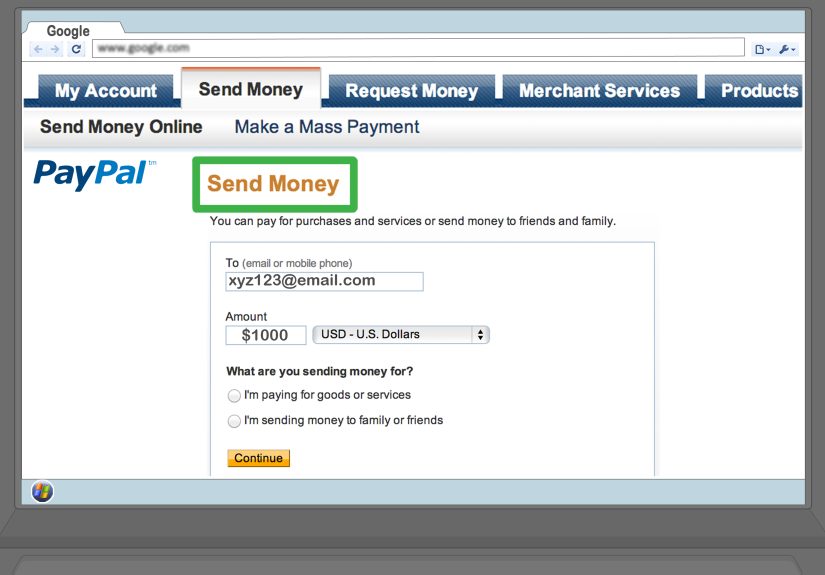

Step 4: Initiate the Wire Transfer Through Your Bank (Online, App, or In Person)

Most major banks and credit unions let you send wires through online banking, a mobile app, or a branch.

Some institutions require an initial setup step, identity verification, or first-time wires to be done in person.

Business accounts may have different workflows and approval controls.

Typical process inside your bank’s wire transfer screen:

- Select Send money / Wire transfer (wording varies).

- Choose Domestic or International.

- Add a recipient/beneficiary (name, address, bank details).

- Enter amount and currency (for international).

- Review fees, delivery estimate, and any exchange rate details.

- Authenticate (one-time passcode, token, call-back, or in-branch ID check).

Example: You’re sending $8,500 to a new apartment landlord for a deposit.

Your bank may require you to add the landlord as a wire recipient, then confirm via a text code or a call.

If it’s a first-time recipient, your bank may add extra security steps (annoying, yesbut also protective).

Step 5: Review, Approve, and Send Before the Cutoff Time

Banks process wires on business days and often have a daily cutoff time. If you submit after the cutoff, your wire may go out the next business day.

Domestic wire cutoffs can differ from international wire cutoffs, and the cutoff may vary by whether you’re sending online vs. in a branch.

Before you hit “Send,” review these three lines like your wallet depends on it (because it does):

- Beneficiary name

- Routing/SWIFT and account number

- Amount and currency

Once you authorize the wire, save the confirmation details. Your bank may provide a reference number (sometimes called an IMAD/OMAD for Fedwire

or an internal confirmation number). That receipt is your proof of payment and the key to tracking if anything goes sideways.

Step 6: Confirm Delivery, Track the Wire, and Keep Records

After sending, confirm with the recipient that funds arrived. For domestic wires, confirmation can happen the same day.

For international wires, timing can vary due to time zones, intermediary banks, compliance checks, and local banking hours.

If the recipient says “Nothing arrived,” do this:

- Confirm the wire was sent (not scheduled, pending, or rejected).

- Check for a return (wrong details can cause a wire to bounce back).

- Ask your bank to trace the wire using your confirmation/reference number.

- If it’s international, ask whether an intermediary bank may have deducted fees or caused delays.

Important consumer note for certain international transfers

Some international “remittance transfers” sent by U.S. consumers fall under Regulation E’s remittance transfer rules, which include specific disclosure,

cancellation, and error-resolution procedures. For example, in many cases there is a short window (often 30 minutes after payment) to cancel and receive a refund,

and there are formal timelines for investigating reported errors. Ask your provider what rules apply to your transfer.

Wire Transfer Fees, Exchange Rates, and “Where Did My Money Go?”

Wire costs can be more complicated than “a flat fee.” Here’s what can show up:

Common wire cost components

- Outgoing wire fee: What your bank charges to send the wire (often higher for international).

- Incoming wire fee: What the recipient’s bank charges to receive the wire (yes, this exists).

- Intermediary bank fees: Some international wires pass through one or more correspondent banks, which may deduct fees.

- Exchange rate markup: If currency conversion is involved, the rate may include a spread.

Example: Domestic vs. international cost feel

A domestic wire might cost a straightforward sending fee, and the recipient gets the full amount.

An international wire might cost a sending fee and involve exchange-rate spread and arrive slightly short if intermediary fees were deducted.

If you need the recipient to receive an exact amount, ask your bank what options exist for fee handling and currency choice.

Wire Transfer Safety Tips (Because Scammers Love Wires)

Wire transfers are a favorite in fraud schemes because they can move quickly and are hard to reverse.

If someone is insisting on a wireespecially with urgencyslow down and verify.

Simple rules that prevent expensive regrets

- Never wire money to “fix fraud.” If someone claims to be your bank and tells you to wire money, it’s almost certainly a scam.

- Treat wiring instructions like sensitive data. Use secure channels and avoid random email threads.

- Verify changes. If wiring details change, confirm via a trusted number or in person.

- Don’t let urgency override verification. Legit businesses can wait 10 minutes while you confirm.

- Keep documentation. Save invoices, contracts, confirmations, and communications.

If you suspect you’ve been scammed, contact your bank immediately. Speed mattersyour bank may attempt a recall or outreach to the receiving institution,

even though success is not guaranteed.

Common Wire Transfer Mistakes (and How to Avoid Them)

Mistake 1: Using the wrong routing number type

Some banks use different routing numbers for wires vs. ACH. If you’re copying details from an old direct-deposit form,

it may not match what’s needed for a wire. Always use the wiring instructions provided for wire transfers.

Mistake 2: Name mismatch

If the beneficiary name doesn’t match what the receiving bank expects, the wire may be delayed or returned.

For business payments, confirm whether the account is under the company name, a legal entity name, or an individual.

Mistake 3: Waiting until the last minute

Cutoff times and business-day processing can turn “I’ll do it at 4:59” into “See you tomorrow.”

If the wire is time-sensitive, send earlier and build in a buffer.

Mistake 4: Trusting emailed wiring instructions without verification

Business email compromise scams specifically target wiring instructions. Always verify independently

especially for real estate, invoices, and new vendors.

FAQ: Quick Answers to Wire Transfer Questions

How long does a wire transfer take?

Domestic wires are often same business day if submitted before the cutoff. International wires commonly take 1–3 business days,

but delays can happen due to intermediary banks, compliance checks, time zones, and local banking schedules.

Can I cancel a wire transfer?

It depends. Many bank wires can’t be canceled once sent, and recovery is often difficult if you made a mistake or were scammed.

For certain remittance transfers governed by specific consumer rules, there may be a short cancellation window (ask your provider).

If you need to stop a wire, contact your bank immediatelyminutes matter.

What’s the difference between a wire transfer and an ACH transfer?

ACH transfers typically cost less but can take longer (often 1–3 business days) and are used for payroll, bill pay, and bank-to-bank transfers.

Wires are generally faster and are commonly used for large, time-sensitive payments, but they usually cost more.

Do wire transfers have limits?

Many banks set wire limits based on account type, relationship history, security checks, and whether you send online or in person.

If you’re wiring a large sum, ask your bank about limits and timing in advance.

Conclusion: Wire Transfers Are PowerfulSo Treat Them Like Power Tools

Wire transfers are one of the fastest ways to move significant money, and they’re a standard solution for real estate, business payments,

and urgent transfers. The tradeoff is precision and caution: the details must be perfect, fees can stack up, and wires can be hard to reverse.

Follow the six steps: confirm a wire is appropriate, gather exact recipient details, verify everything, initiate through your bank, send before cutoff,

and confirm delivery with records. Do that consistently and a wire transfer becomes a reliable toolnot a stressful story you tell at brunch.

Real-World Wire Transfer Experiences (What People Learn the Hard Way)

If you ask people about wire transfers, you’ll notice a pattern: nobody tells “fun” wire stories. They tell “educational” wire stories.

The kind where the lesson is clear, the stakes were high, and the moral is basically “double-check everything.”

One common experience is the real estate wire scramble. Someone is closing on a home, the title company sends wiring instructions,

and the buyer waits until the morning of closing to send the funds. Then the bank says, “Great! Just note the cutoff time was earlier,”

or “We need additional verification for a first-time wire.” Suddenly, everyone is calling everyone, the buyer is sweating, and the phrase

“business day” becomes the villain of the story. The takeaway: if a deadline matters, wire early, and ask your bank what authentication steps

might be required before you’re staring down a clock.

Another frequent lesson: the “tiny typo, big delay” situation. A single wrong digit in an account number, an incorrect routing number type

(wire vs. ACH), or a missing SWIFT/IBAN character can cause a wire to bounce back or get stuck in limbo. People often assume the bank will

“figure it out,” but banks generally process what you submit. If the information doesn’t match what the receiving bank expects, the wire may

be rejected or delayed while institutions investigate. The takeaway: treat each digit like it’s the code to a safe, because it kind of is.

International wires introduce their own character development arc. People learn that the recipient might receive slightly less than expected

due to intermediary or receiving bank fees, or that currency conversion can change the outcome depending on the exchange rate and timing.

A sender thinks, “I sent $2,000,” while the recipient says, “I got the equivalent of $1,960,” and everyone feels mildly betrayed by math.

The takeaway: if the recipient needs an exact amount, ask about fees, currency choice, and whether deductions can occur along the route.

Then there’s the scam storyoften involving “updated wiring instructions.” A vendor invoice arrives, then a follow-up email says,

“Important: our bank info has changeduse this account instead.” The email looks legit, the urgency feels plausible, and the new account is,

unfortunately, a scammer’s. People who avoid this usually did one simple thing: they verified the change by calling a trusted number already on file,

not the one in the email. The takeaway: wiring instructions should never be trusted on email alone, especially when something changes.

Finally, many people learn that banks take security seriously for a reason. First-time wires, large amounts, or unusual patterns can trigger extra

verification steps. It can feel inconvenient, but it’s often the difference between a safe transfer and a disaster. The takeaway: plan ahead,

keep your contact info updated for authentication, and don’t interpret security friction as “the bank being dramatic.” Sometimes the bank is saving you

from a very expensive plot twist.