Table of Contents >> Show >> Hide

- Introduction: When the White House Moves Into Your Brokerage Account

- What Are Presidential Partisan Portfolios?

- The Historical Puzzle: Markets Have Often Done Well Under Democratic Presidents

- Why Sentiment Changes Faster Than Portfolios

- The Sector Temptation: Betting on the President’s Favorites

- Investor Psychology: The Real Swing State

- What Actually Drives Long-Term Returns?

- How to Think About Presidential Partisan Portfolios Without Losing Your Mind

- Specific Examples of Partisan Portfolio Mistakes

- The Rise of Political Identity in Investing

- Practical Rules for Investors During Presidential Cycles

- Experiences Related to Presidential Partisan Portfolios

- Conclusion: Vote at the Ballot Box, Not With Your Entire Portfolio

Note: This article is for educational and editorial purposes only. It discusses market history, investor psychology, and portfolio behavior, but it is not personal financial advice.

Introduction: When the White House Moves Into Your Brokerage Account

Every four years, Americans vote for a president. Then, almost immediately, many investors start voting againthis time with their portfolios. Some buy stocks because their preferred party won. Others flee to cash because the “wrong” president took office. A few begin talking about gold, canned beans, and “the end of the economy as we know it,” usually before breakfast.

This is the world of Presidential Partisan Portfolios: investment decisions shaped not only by earnings, interest rates, valuation, inflation, or business cycles, but also by political identity. The idea is simple and surprisingly emotional. If investors feel confident when “their side” controls the White House, they may take more risk. If they feel worried when the opposing party wins, they may sell stocks, move into bonds, or sit in cash while waiting for the financial sky to fall.

The trouble is that markets are not registered voters. The S&P 500 does not carry a party card. Corporate profits, Federal Reserve policy, productivity, global trade, consumer spending, and technological change often matter far more than campaign slogans. Still, presidential politics can influence taxes, regulation, energy policy, defense spending, tariffs, health care, immigration, and investor sentiment. So the question is not whether politics matters. It does. The better question is: Should politics run your portfolio?

What Are Presidential Partisan Portfolios?

A presidential partisan portfolio is an investment approach that tilts based on which political party controls the presidency. In its simplest form, it might mean owning more stocks under one party and more cash or bonds under another. In a more sophisticated version, it could mean favoring sectors expected to benefit from a president’s policy agendaenergy, defense, health care, financials, technology, industrials, or clean infrastructure.

For example, an investor might assume that a Republican administration will favor lower taxes, deregulation, fossil fuels, defense contractors, and banks. Another investor might assume that a Democratic administration will favor renewable energy, health care expansion, infrastructure, consumer protections, and social spending. These assumptions are not pulled out of thin air; parties do tend to emphasize different policies. But investing based only on party labels is like trying to cook dinner using only the color of the pan. It may tell you something, but not nearly enough.

The Historical Puzzle: Markets Have Often Done Well Under Democratic Presidents

One of the most discussed findings in financial research is sometimes called the “presidential puzzle.” Academic studies have found that U.S. stock market returns, especially excess returns over Treasury bills, have historically been higher under Democratic presidents than under Republican presidents. This result surprises many investors because Republicans are often viewed as more business-friendly, while Democrats are often viewed as more regulation-friendly.

But historical averages can be tricky little creatures. They look confident in a spreadsheet and then become shy when you ask them to predict the future. The market’s performance under any president depends heavily on the economic starting point. A president who takes office near the bottom of a recession may enjoy a strong recovery. Another who enters during an expensive bull market may inherit trouble. Timing matters. Valuations matter. Inflation matters. Wars, pandemics, banking crises, oil shocks, and Federal Reserve decisions matter. The president matters toobut rarely alone.

Examples From Recent History

Consider the Clinton years. The 1990s saw strong economic growth, falling deficits, globalization, and a technology boom. Stocks surged. Was that because of presidential party, productivity, the internet, lower interest rates, or all of the above? The honest answer is: probably all of the above, with a generous scoop of investor enthusiasm.

During George W. Bush’s presidency, investors faced the dot-com crash, the September 11 attacks, wars in Afghanistan and Iraq, and the global financial crisis. Those events were massive market forces. Reducing the entire period to “Republican president equals weak returns” misses the hurricane for the umbrella.

Under Barack Obama, stocks recovered strongly from the financial crisis, helped by low interest rates, improving corporate profits, bank stabilization, and aggressive monetary policy. Under Donald Trump’s first term, markets benefited from corporate tax cuts and deregulation expectations, but also faced trade-war volatility and the COVID-19 crash. Under Joe Biden, investors dealt with reopening, inflation, higher rates, fiscal stimulus, energy shocks, and an artificial intelligence boom. In each case, politics was part of the story, not the whole novel.

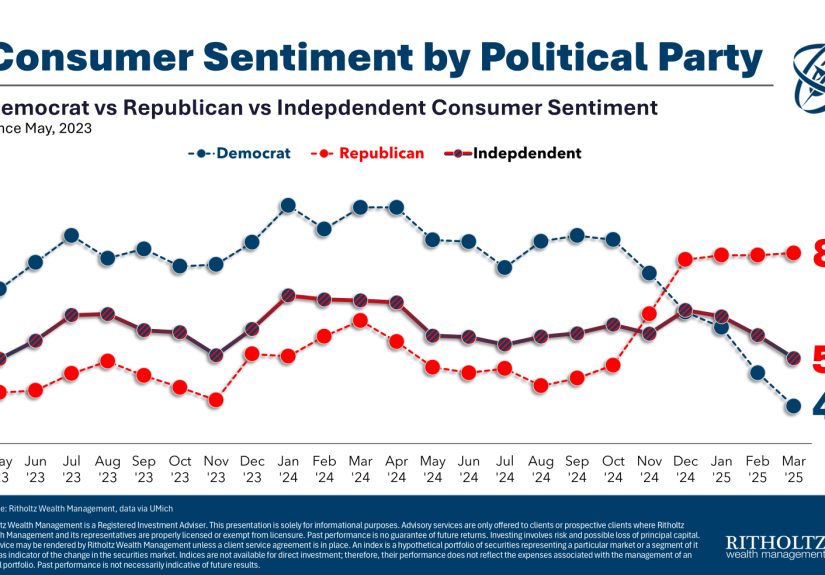

Why Sentiment Changes Faster Than Portfolios

Political identity can change how people feel about the economy almost overnight. When a president from one party wins, supporters often become more optimistic, while opponents suddenly see storm clouds forming over every grocery receipt, gas pump, and stock chart. Consumer sentiment surveys have repeatedly shown large partisan gaps depending on who occupies the White House.

But there is an important distinction between what people say and what they do. Investors may tell pollsters they are terrified, furious, or ready to move everything into cash. Yet many keep contributing to retirement accounts, holding index funds, and buying homes. In other words, political mood can swing like a screen door in a thunderstorm, while actual portfolio behavior often moves more slowly.

That said, some investors really do make dramatic changes. They sell after an election. They stop contributing to stocks. They buy assets that match their political worldview. They follow commentators who confirm their fears. Over time, this can become expensive. Missing a few of the market’s strongest days can damage long-term returns, and those big days often arrive when headlines look terrible.

The Sector Temptation: Betting on the President’s Favorites

Sector investing is where presidential partisan portfolios become especially tempting. If a candidate campaigns on more defense spending, investors may look at aerospace and defense companies. If a president promotes clean energy subsidies, renewable energy stocks may attract attention. If deregulation is expected, banks and financial companies may rally. If tariffs rise, domestic manufacturers may look attractive while import-heavy retailers may come under pressure.

These connections sound logical. Sometimes they work. The problem is that markets price in expectations quickly. By the time an average investor says, “This sector should benefit,” Wall Street may have already ordered the cake, eaten it, and started arguing about dessert. A policy can also help an industry but hurt a company. Subsidies may increase competition. Tariffs may protect one manufacturer while raising costs for another. Lower taxes may boost profits, but if valuations are already high, stocks can still disappoint.

Policy Is Not the Same as Profit

A president may support an industry, but shareholders still need earnings, margins, cash flow, and reasonable prices. A solar company can operate in a friendly policy environment and still struggle with debt. A bank can benefit from deregulation but suffer if credit losses rise. An oil company can enjoy pro-drilling policies but lose money if crude prices fall. Politics opens doors; business fundamentals decide who walks through without tripping over the rug.

Investor Psychology: The Real Swing State

The most dangerous part of partisan investing is not politics. It is overconfidence. When investors believe their political team understands the economy and the other side is guaranteed to destroy it, they can become blind to evidence. Good news under the opposing party gets dismissed as fake, temporary, or suspiciously convenient. Bad news under their preferred party becomes “short-term noise.” That is not analysis. That is sports fandom wearing a finance hat.

Behavioral finance research has long shown that investors are vulnerable to confirmation bias, loss aversion, recency bias, and narrative addiction. Presidential elections pour gasoline on all four. A scary headline becomes a trading signal. A campaign promise becomes an earnings forecast. A social media rant becomes a macroeconomic thesis. Suddenly, the portfolio is not diversified across assets; it is concentrated in feelings.

Good investing requires the humility to say, “My political opinion may be sincere, but it may not be profitable.” That sentence will not go viral, but it may save your retirement account from doing something dramatic and unnecessary.

What Actually Drives Long-Term Returns?

Over long periods, stock returns are driven by corporate earnings, dividends, valuation changes, innovation, productivity, inflation, interest rates, and risk appetite. Bonds are shaped by yields, inflation expectations, credit quality, and duration. Cash depends on short-term interest rates. Real estate responds to income, financing costs, supply, demand, and local conditions. Politics can influence all of these, but it rarely controls them completely.

The Federal Reserve, for example, is often more important to markets than the president in the short run. Interest-rate policy affects borrowing costs, discount rates, mortgage rates, business investment, and investor appetite for risk. A president may pressure, praise, or criticize the Fed, but monetary policy has its own institutional rhythm. Likewise, global events can overpower domestic politics. Oil shocks, wars, supply-chain disruptions, pandemics, and foreign recessions do not politely wait for election calendars.

How to Think About Presidential Partisan Portfolios Without Losing Your Mind

The best approach is not to pretend politics is irrelevant. That would be naive. Instead, investors should separate policy awareness from partisan market timing. Policy awareness means understanding how taxes, regulation, spending, trade, and deficits may affect sectors and asset classes. Partisan market timing means making big all-or-nothing moves because you love or hate the president. The first can be useful. The second can be hazardous.

Build a Portfolio That Can Survive Both Parties

A durable portfolio should not need your favorite candidate to win. It should be designed around your goals, time horizon, income needs, risk tolerance, tax situation, and liquidity needs. For many investors, that means broad diversification across U.S. stocks, international stocks, high-quality bonds, cash reserves, and possibly real assets. The exact mix depends on the person, but the principle is universal: do not build a portfolio that collapses emotionally every election night.

Rebalancing can also help. If stocks surge after an election, rebalancing trims risk. If markets fall because investors panic over policy uncertainty, rebalancing may push you to buy at lower prices. This is boring. Boring is underrated. Boring is how many portfolios quietly survive while exciting portfolios are busy lighting themselves on fire for attention.

Specific Examples of Partisan Portfolio Mistakes

Imagine an investor who sold all stocks in 2008 because they disliked the incoming administration. That investor may have missed one of the strongest bull markets in U.S. history. Now imagine another investor who became wildly optimistic after the 2016 election, bought only policy-sensitive trades, and ignored valuation and risk. Some positions may have worked, but others would have been vulnerable to trade tensions, rate changes, and pandemic shocks.

Or consider someone who avoided traditional energy stocks for political reasons during periods when oil and gas companies produced strong cash flow. Another investor may have ignored clean energy because they disliked subsidies, even though policy incentives created real business opportunities in certain periods. In both cases, ideology narrowed the opportunity set. Investing is hard enough without voluntarily wearing partisan blinders.

The Rise of Political Identity in Investing

Recent research on household finance and institutional investing suggests that political identity can influence portfolio choices. Some investors prefer companies, funds, managers, or themes that feel aligned with their values. Public pension plans, mutual fund investors, and individual households may all show some degree of political or ideological tilt.

This is not always irrational. Values-based investing can be legitimate when investors knowingly accept trade-offs. Someone may prefer not to own certain industries. Another may want exposure to companies they believe support national security, environmental goals, labor standards, or domestic manufacturing. The danger appears when investors confuse identity satisfaction with expected return. A portfolio can express values, but it still needs risk management.

Practical Rules for Investors During Presidential Cycles

First, write down your investment plan before election season gets loud. A plan created during calm conditions is usually better than one created while cable news is yelling at you from across the room.

Second, limit tactical bets. If you want to express a policy view through sectors, keep it modest. A small satellite position can satisfy curiosity without hijacking your future.

Third, watch valuations. A great political story can still be a bad investment if the price already assumes perfection.

Fourth, focus on after-tax, after-inflation returns. The party in power matters less than whether your money is actually growing in real purchasing power.

Fifth, avoid emotional all-cash decisions. Cash feels safe, especially when politics feels chaotic, but inflation and missed market gains can make it costly over time.

Experiences Related to Presidential Partisan Portfolios

One of the most common investor experiences during election years is the sudden transformation of normal people into part-time political economists. A neighbor who rarely discusses bond yields may begin explaining currency debasement while standing beside the mailbox. A cousin who once bought a stock because he liked the company’s sneakers may now have a detailed theory about tariff policy. Election season does that. It makes the market feel personal.

Many investors remember moments when they felt certain a president would either rescue or ruin the economy. Then the market did something else. After one election, futures might fall overnight and recover quickly. After another, analysts may predict a boom, only for volatility to arrive instead. These experiences teach a humbling lesson: the first market reaction is not always the final verdict. Wall Street is very good at sounding confident while changing its mind before lunch.

Financial advisors often see this pattern up close. A client may call after an election wanting to sell everything. Another may want to double stock exposure because their preferred candidate won. In both cases, the advisor’s real job is not to debate politics. It is to bring the conversation back to goals. Are you retiring in three years or thirty? Do you need income? Do you have emergency savings? Has your risk tolerance changed, or did your television simply get louder?

Individual investors also learn that their political expectations can be right while their trades are wrong. A president may pass a policy that helps an industry, but the related stocks may already be expensive. A regulation may hurt sentiment, but strong companies may adapt. A tax cut may boost profits, but rising interest rates may pressure valuations. Markets are not simple applause meters for Washington.

The healthiest experience is often the boring one: keep contributing, rebalance occasionally, maintain diversification, and review the plan after emotions cool. Investors who lived through multiple administrations have seen enough plot twists to know that panic is not a strategy. The White House changes hands. Congress flips. The Fed tightens and cuts. Headlines scream. Companies still compete, innovate, fail, merge, and grow. The investor’s task is not to ignore politics, but to prevent politics from becoming the portfolio manager.

Conclusion: Vote at the Ballot Box, Not With Your Entire Portfolio

Presidential partisan portfolios are understandable because politics affects confidence, policy, and expectations. But understandable does not always mean wise. History shows that markets can perform well under both parties and poorly under both parties. The economy is too complex to reduce to a bumper sticker, and your portfolio is too important to be driven by election-night emotions.

The smarter path is to understand policy without becoming captive to partisanship. Use politics as one input, not the steering wheel. Build a portfolio that can survive presidents you admire and presidents you dislike. In the long run, discipline, diversification, valuation, earnings, savings behavior, and emotional control are likely to matter more than which party controls the Oval Office.

In other words, vote passionately. Invest patiently. And never let a campaign slogan do the job of a financial plan.